NEW ZEALAND: VIEW: Weak Growth Drives Westpac To Expect 50bp October Cut

Q2 NZ GDP printed well below both consensus and the RBNZ’s expectations at -0.9% q/q compared to -0.3%. The weakness was also broad based with 10 out of 16 sectors contracting. The MPC had signalled 50bp of easing over two meetings but there is a risk of a 50bp move after two of the four members voted for a 50bp cut in August. Given the weak GDP data, Westpac is now forecasting 50bp, up from 25bp, at the 8 October decision with another 25bp on 26 November bringing the OCR to 2.25%.

- Westpac expects rates to become stimulatory and that they won’t increase again until after the late 2026 election but the risk is that it will be before this.

- In August, RBNZ Governor Hawkesby said that estimates of spare capacity had increased and thus its OCR profile was revised lower. Westpac notes that the significantly weaker Q2 GDP outcome “implies greater than expected economic slack”.

- Hawkesby said the economy looked better in July and there are signs that growth will pick up in H2, as was expected. The RBNZ expects growth to recover in H2 with Q3 forecast at +0.3% q/q and Q4 +0.8% q/q. Westpac is forecasting Q3 GDP to rise 0.6% q/q.

- Westpac notes that the key data point before the October decision is the QSBO survey on October 7 but that it would need to be very strong for the RBNZ to cut by 25bp rather than 50bp. Q3 CPI and labour market data will print after the October meeting but before November’s.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: AUD Crosses - Tread Water

US equities traded sideways overnight, consolidating as the market awaits Powell's Jackson Hole speech. This morning US futures have turned a little lower, ESU5 -0.10%, NQU5 -0.10%. The AUD traded sideways in the crosses overnight, after trading a little heavy recently.

- EUR/AUD - Overnight range 1.7920 - 1.7993, Asia is currently trading around 1.7960. The direction US stocks ultimately decide on following will have a direct impact on the direction of this pair. It is currently probing the top end of its 1.7650/1.8100 range, which has seen decent supply cap it the last few months.

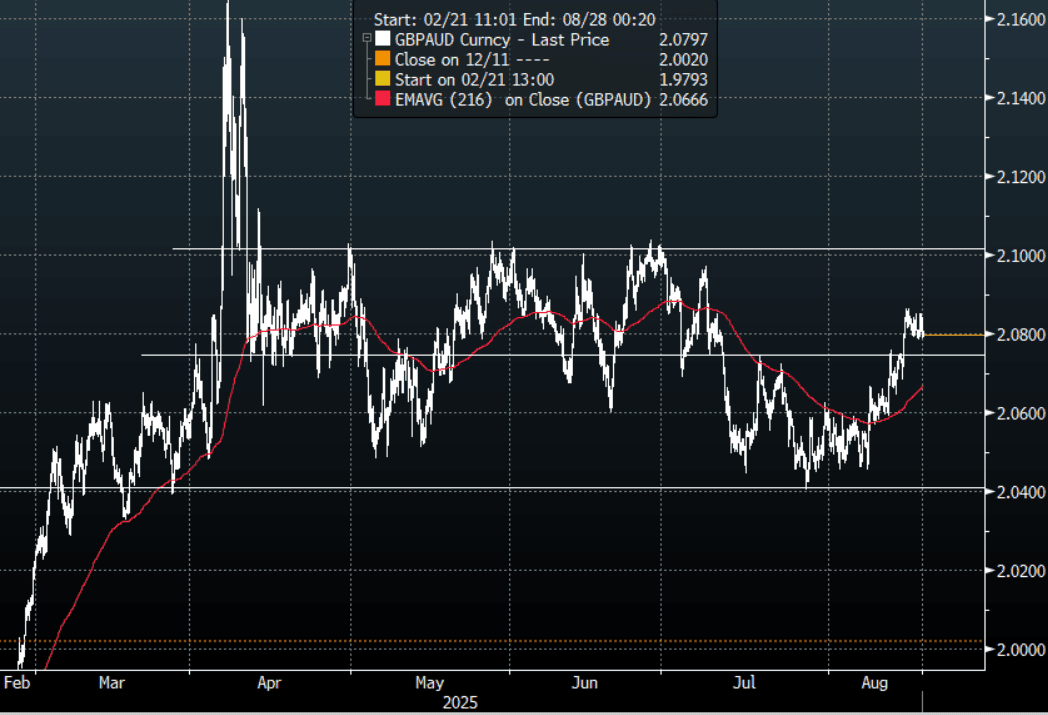

- GBP/AUD - Overnight range 2.0783 - 2.0850, Asia is trading around 2.0800. The pair's momentum higher has stalled in recent days. Having broken above the pivot within its 2.0400 - 2.1050 range, dips should be supported enroute to testing 2.10/11.

- AUD/JPY - Overnight range 95.87 - 96.20, Asia is trading around 96.00. The pair found good demand last week towards 95.50, price is now firmly back into the 94.50-97.50 range looking for clearer direction.

- AUD/NZD - Overnight range 1.0955 - 1.0974, the cross is dealing in Asia around 1.0955. The Cross is trying to push higher but continues to stall back towards 1.1000 and will need a sustained break here to potentially extend. Until then the range looks to be 1.0850-1.1000.

Fig 1: GBP/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

POLITICAL RISK: Ukraine/Russia To Decide On Territory Issues

Ukrainian President Zelenskyy and key EU leaders have hailed the meetings with US President Trump as a success and positive progress towards ending the Russia-Ukraine conflict. Still, a degree caution remains and seemingly many details still need to fall into place.

- The first is a meeting between Zelenskyy and Putin has to take place. No exact timeframe was given, but a number of officials suggested the aim was to have a meeting in the next 2-3 weeks between the two leaders. It is expected that a trilateral meeting including US President Trump would then take place after this.

- A focus point for the Zelenskyy/Putin meeting would be on territory claims falling out from any peace deal. A headline crossed via Rtrs: "UKRAINE'S PRESIDENT SAYS TERRITORIAL ISSUES WILL BE DECIDED BETWEEN RUSSIA AND UKRAINE - [RTRS]".

- This comes after earlier reports of Russia reportedly offering to hold its frontlines in Kherson and Zaporizhzhia in exchange for the Donbas, not all of which it currently occupies.

- The other focus point will be on security guarantees for Ukraine. This headline crossed earlier: "*RUTTE: WE'RE DISCUSSING ARTICLE 5 TYPE OF SECURITY GUARANTEES" (via BBG).

- Still, but Rutte (the NATO Secretary General) and French President Macron stated details on security guarantees need to be worked on/out with the US. Trump said that they will principally be provided by Europe but the US will also be “involved” and that “we’ll give them good protection”.

- Macron added that if Putin doesn't attend a meeting then more pressure will be needed on Russia. He also expressed pessimism on whether Putin actually wants a peace deal.

- Zelenskyy also agreed with Trump to buy $100bn of US weaponry and to a $50bn US-Ukraine drone manufacturing venture. The funding is likely to come from Europe.

US STOCKS: Tread Water Ahead Of Jackson Hole

The ESU5 overnight range was 6456.00 - 6479.75, Asia is currently trading around 6470. The ESU5 contract traded sideways consolidating just above 6450, as the market awaits Powell's Jackson Hole speech. This morning US futures opened a fraction higher, ESU5 +0.05%, NQU5 +0.05%. Only a break below 6200 would potentially signal a deeper correction. For now the price action in stocks continues to be bullish ignoring all headwinds as the Trump Administration runs the economy hot which for the moment has superseded the seasonal volatility that normally characterises the August/September period.

- Wei Li(CIS BlackRock) on LinkedIn - "Quiet.. so quiet. With equity rate and currency vols at lows this year, and heading into seasonally choppy September and October, derivatives overlay strategy should be looked at. Especially if already long risk and not ready to call end."

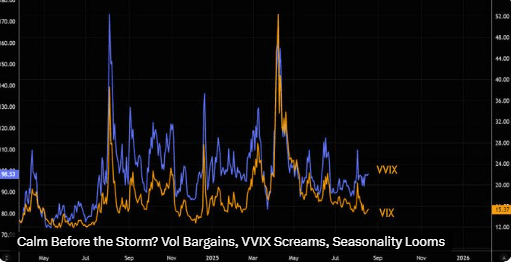

- The Market Ear on X: “QQQ 1-month implied vol just hit a YTD low and is nearing multi-year lows. We see immense value in owning hedges through the rest of summer. Do not underestimate the VVIX.” See Fig.1 Below.

- Lance Roberts on X: “Two things can be true at the same time - bullish fundamentals and stretched markets.”

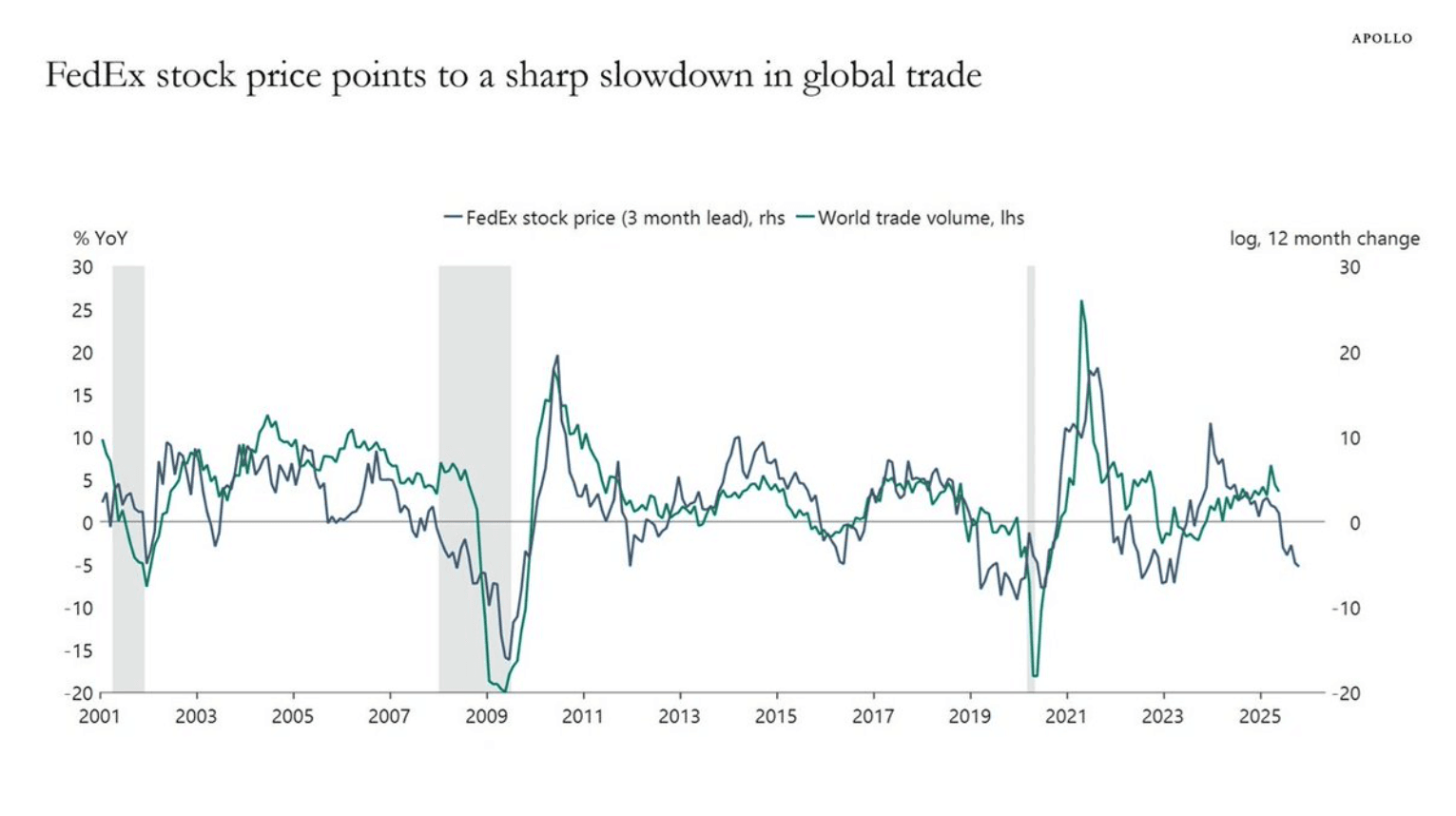

- Daily Chartbook on X: "FedEx’s stock price is a leading indicator of global trade." - Apollo Sløk. See Fig.2 Below.

Fig.1: VIX Vs VVIX

Source: MNI - Market News/@themarketear

Fig.2: FedEx Vs World Trade Volume

Source: MNI - Market News/@dailychartbook/Apollo