THAILAND: VIEW: JP Morgan Brings Forward Remaining Rate Cuts

The Bank of Thailand cut rates 25bp to 1.5% as JP Morgan and Bloomberg consensus expected. JP Morgan noted that the MPC is more concerned about “structural competitiveness” and the stronger baht and that if they become part of BoT’s reaction function, then policy may “stay below neutral” for some time, which it estimates at around 1.5%. It continues to expect rates to trough at 1% but has brought forward its two remaining cuts to October and December from Q4 2025 & Q1 2026.

- JP Morgan believes that “should gold-related error & omission inflows persist and keep the NEER strong, the central bank may need to resort to more rate cuts as a macro adjustment tool”.

- “The BoT mentioned that the Thai baht’s outperformance against regional currencies may have “implications for economic activity”. As far as we know, this is the first time that the central bank has openly brought up FX as a macro headwind. This was not the case even in previous MPC meetings that resulted in rate cuts.”

- “The MPC did not alter its key macroeconomic projections. However, the characterization of growth headwinds, both externally and domestically, has turned decidedly more negative.”

- “Although the reciprocal tariff outcome (19%) came in line with its baseline scenario (18%), the BoT mentioned that U.S. trade policies will “exacerbate structural problems” and “weaken competitiveness”, suggesting that they are concerned about the “substitution effect” caused by tariffs, not just the “income effect” from weaker end-demand.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Bear-Steepener Extends

In Tokyo morning trade, JGB futures are slightly weaker, -3 compared to settlement levels.

- Today, the local calendar will be empty apart from 5-year Climate Transition supply.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session after yesterday’s modest sell-off. Focus is on Tuesday's June CPI inflation data and several Fed speakers ahead of Friday evening's policy blackout. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June on a rounded basis, but with sizeable risk of undershooting at 0.2% (MNI median unrounded estimate at 0.24% M/M /average 0.25%).

- Cash JGBs are flat to 9bps cheaper across benchmarks, with a steeper curve. The benchmark 10-year yield is 0.3bp higher at 1.585% after revisiting the cycle high of 1.596% earlier in the session.

- (Bloomberg) “Fixed income investors are paying extra attention to rising Japanese yields for their global impact, yet it is Treasuries which are still the driving force behind G-10 debt markets. The next major catalyst for global yields to spread anxiety across asset classes will be 30-year Treasury yields surpassing the peak seen in May, which looks likely given the US passed the huge tax and spending bill that almost guarantees an even wider fiscal deficit.”

- Swap rates are ~1bp higher. Swap spreads are mostly tighter.

US STOCKS: Shrug Off Tariffs, Focus On Trump Still Being Open To Negotiate

The ESU5 overnight range was 6259.75 - 6315.00, Asia is currently trading around 6305. The September contract lifted off the 6250 area and has closed back above 6300. This morning has seen US futures open a little lower, ESU5 -0.10%, NQU5 -0.10%. US Stocks have shrugged off the latest tariff threats and instead focused on the fact Trump said he is still open to more trade negotiations.

- Wei Li(BlackRock) on LinkedIn: “ONE MYSTERY that the team has been debating all week – who will bear the cost of higher tariffs? Is it: Consumers? Yet to show up meaningfully, all eyes on CPI tonight; Corporates? But it is not consistent with profit margin making new highs, all eyes on earnings kicking off this week; Foreign suppliers? I’ve only seen some inconclusive evidence at best.”

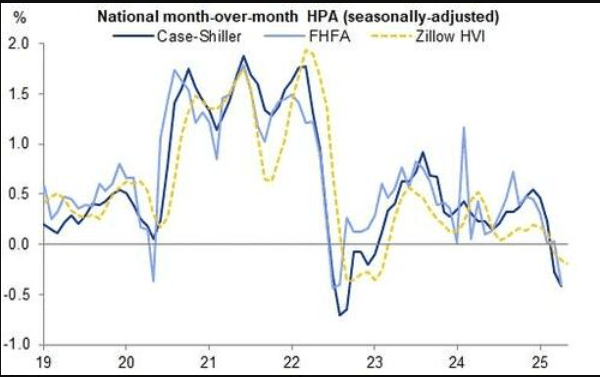

- Lance Roberts on X: “Housing, which makes up over 40% of the CPI index, continues to weaken. Both the number of home sales and prices continue to decline." See Graph Below.

- Mark Zandi on X: ”I sent off a yellow flare on the housing market in a post a couple of weeks ago, but I now think a red flare is more appropriate. Home sales, homebuilding, and even house prices are set to slump unless mortgage rates decline materially from their current near 7% soon. That, however, seems unlikely.”

- (Bloomberg) - “Wall Street banks are poised to post gains largely from record trading in the aftermath of Trump’s “Liberation Day” shock. Analysts expect Goldman to lead in equities and JPMorgan in FICC, with investors watching for guidance on how lenders plan to ride regulatory tailwinds”

- Short-term this is starting to look a little overdone but the market clearly disagrees for now and sees the potential for a melt-up. First support is back towards the 6100 area.

Fig 1: National Month-Over-Month HPA

Source: MNI/@lanceRoberts

ASIA STOCKS: Recent Positive Inflow Momentum Stalls (Ex South Korea)

The start of the week saw positive inflow momentum into South Korea and Thailand, but mostly softer trends elsewhere. South Korea's Kospi continues to rally, testing through 3200, amid bullish sell-side optimism (on reform hopes and earnings). This is likely aiding a return of offshore inflows, although year to date flows remain firmly in negative territory, so there is still scope for catch up.

- Taiwan saw net outflows yesterday, trimming net inflows seen in the past 5 trading sessions. At the end of last week, India saw sharp outflows, the largest since the end of May.

- Offshore investors returned to net selling Indonesian stocks yesterday, a consistent theme since the start of July.

- The rebound in the SET Thailand index (which gained a further +2% yesterday) is drawing in flows, with month to date offshore buying now back into positive territory.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 160 | 843 | -8340 |

| Taiwan (USDmn) | -163 | 1121 | -2104 |

| India (USDmn)* | -524 | 9 | -8328 |

| Indonesia (USDmn) | -70 | -148 | -3571 |

| Thailand (USDmn) | 42 | 115 | -2323 |

| Malaysia (USDmn) | 0 | -57 | -2793 |

| Philippines (USDmn) | 11 | -5 | -551 |

| Total (USDmn) | -542 | 1877 | -28011 |

| * Data Up To July 11 |

Source: Bloomberg Finance L.P./MNI