OIL: Vietnam Buys First US Crude Since December

Vietnam has bought the first US crude since Dec. 2024, according to Reuters sources.

- The country typically buys crude from Kuwait, Brunei and Libya.

- Vietnam's Binh Son Refining and Petrochemical typically processes domestic crude but has bought 1mbbl of US WTI for November delivery.

- Vietnam, and other countries such as Indonesia and Thailand, have committed to buy more US crude as part of deals to avoid high US tariffs and reduce trade surpluses with the US.

- WTI has become more competitive in Asia for November delivery amid stronger Middle East prices.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FRANCE: 2026 Budget Outline At 1500BST/1600CET The Next Source Of Risk For OATs

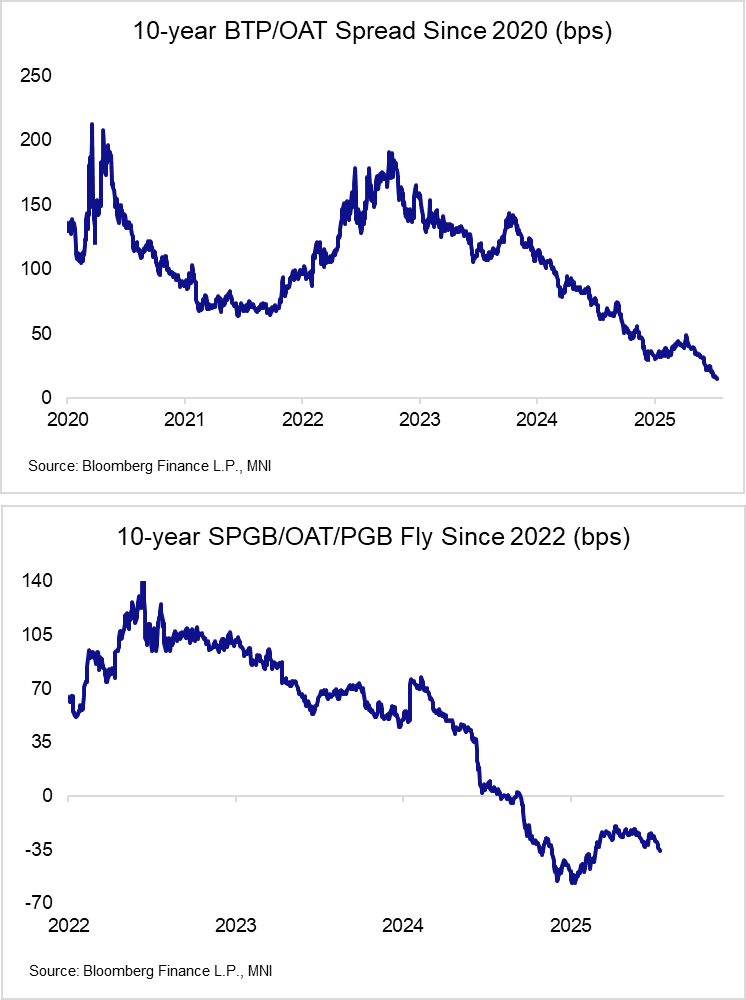

At 1500BST/1600CET today, French PM Bayrou is set to unveil the main proposals of the 2026 state budget, including spending cuts and tax hikes that risk collapsing his minority government. French political risks gradually been priced back into OATs in recent weeks, particularly when assessing French debt against semi-core/periphery peers. Last week, we highlighted a persistent tightening trend in the 10-year BTP/OAT spread, with markets eyeing full convergence if PM Bayrou is forced out of office.

- 10-year GGB yields have also moved below OATs this month, with the GGB/OAT spread currently below -2bps. Meanwhile, OATs have displayed renewed cheapening on the SPGB/OAT/PGB fly since the end of June.

- Bayrou has previously noted that E40bln in fiscal savings are required for the Government to meet its 4.6% 2026 deficit target.

- Without a majority, Bayrou is likely to be forced to use Art. 49.3 of the French constitution to push the budget through without a vote in parliament. The far-right RN party has threatened to vote in favour of a censure motion in the autumn should the PM utilise Art. 49.3, and with the parties of the left also on board, such a vote would be enough to remove Bayrou from office.

- This morning, RN MP Sébastien Chenu doubled down on his party’s threats, stating to BFMTV/RMC that “If you ask the French to make additional efforts, regardless of the category—workers, retirees, young people, civil servants—we will say no”.

- A backdrop of political risks and ongoing fiscal pressures did not stop French President Macron from announcing an additional E6.7bln in defence spending by 2027 on Sunday. Macron noted that this spending would not be financed by debt, but economic reforms and a "strength of soul" from the French people. No details were provided, but this is suggestive of the need for yet more fiscal consolidation.

EGB OPTIONS: RXU5 123.50 Puts Lifted

RXU5 123.50 puts paper paid 3 on +4.5K.

STIR: A Little Over 55bp Of Cuts Priced Through Dec Ahead Of UK Risk Events

A relatively flat start for GBP STIRs.

- SONIA futures -1.0 to +1.0.

- Meanwhile, BoE-dated OIS is flat to 1bp less dovish on the day, showing 22bp of cuts for August, 29bp through September, 47bp through November and 56bp through year-end.

- A reminder that a particularly soft REC labour market report and dovish comments from BoE Governor Bailey resulted in dovish repricing on Monday.

- Following those developments J.P.Morgan noted that they “continue to expect a 25bp cut in August, but there are increasing odds of a follow up cut in September which is currently far from fully priced in. Bailey’s comments raise the likelihood of a shift in tone from the BoE in August”.

- They went on to note that “for now the Bank remains cautious due to high inflation, and Bailey’s interview suggests this is partly due to the optics of a headline rate that is expected to continue running close to 3.5% in 2H25. While that is unlikely to change, the BoE will have a limit on its tolerance for weakening data in other areas. Downside surprises in week’s data, for example, would be significant, particularly if they came from the BoE’s core services metric, payroll jobs or private sector average earnings”.

- Bailey & Reeves will speak at Mansion House this evening, while CPI (Wednesday) and labour market (Thursday) data headline this week’s domestic calendar.

- Spillover from today's U.S. CPI data is also eyed.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.001 | -21.6 |

Sep-25 | 3.927 | -29.0 |

Nov-25 | 3.748 | -47.0 |

Dec-25 | 3.656 | -56.1 |

Feb-26 | 3.524 | -69.4 |

Mar-26 | 3.489 | -72.8 |