US CONSUMER CYCLICALS: VF Corp: Bracken interview (edited)

(VFC: Ba2 neg/BB)

You can watch the new CEO in a podcast, he is a charismatic talker. There is not much new there but some points that weren't mentioned elsewhere include:

- Bracken buying over $3m of VF stock thus far

- Management compensation policy heavily skewed to performance

On last point Bracken's salary last year was $12.6m; $1.3m in base, $2.3m based on the years performance targets (= revenue and adjusted EBIT) and other $9m on longer term 3yr rolling targets that are based on revenue & gross Margin (balanced by 75th or 25th out/under performance in the stocks total return vs. S&P600 consumer disc. index).

Equities are struggling to price aggressive growth - likely not helped by mgmt continuing to guide low for next quarter, and the still HSD sales falls in Vans. Credit metrics, net of tariffs, are guided to improve based on FY guidance.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR FUTURES: Large Jun'27/Sep'27/Dec'27 Fly

- 37,000 SFRM7/SFRU7/SFRZ7 flys, trading desks suggest package was sold at -0.5

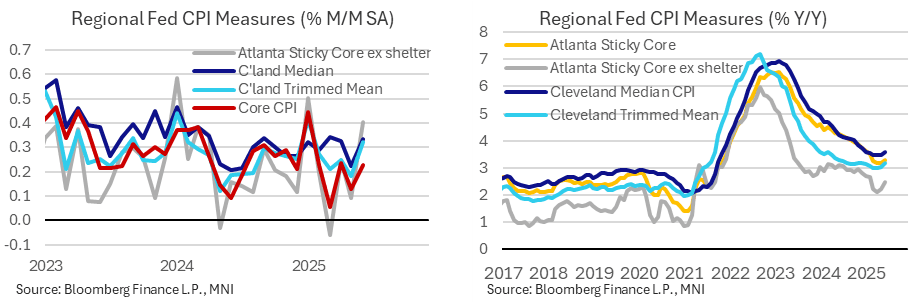

US DATA: Regional Fed CPI Metrics Stabilizing Above Target

- Regional Fed CPI metrics support the earlier notion that core CPI was weighed down by some large items, such as used cars -0.7% on the core goods side and lodging away from home -2.9% on the core services side. See our bullet on the acceleration in median core goods inflation at 0915ET for an example of underlying pressures building.

- Core CPI inflation stood at 0.23% M/M in June after 0.13% in May. In comparison, across the entire CPI basket the Cleveland Fed median lifted from 0.22% to 0.33% M/M (back to Mar/Apr rates) and the 16% trimmed mean accelerated from 0.18% to 0.32% M/M (fastest since Jan 2025).

- There’s a similar story in the Atlanta Fed’s sticky CPI series, with ex-shelter measures on both a headline and core basis accelerating to 0.40% M/M for their fastest since January.

- Taking a step back, Y/Y rates appear to have bottomed in the spring, at least for now, at levels above pre-pandemic averages.

- The Cleveland Fed median increased to 3.6% Y/Y in June after three months averaging 3.47% in a tight range and the trimmed mean increased to 3.17% having touched 2.97% in April. The Atlanta Fed’s sticky core CPI ex shelter series meanwhile increased to 2.46% Y/Y to continue an acceleration from 2.09% in April – see charts.

BONDS: Early EGB Outperformance Sticks, But Futures Follow USTs Lower Post CPI

Major EGB futures continue to follow TYs lower post-US CPI, with Bunds now just +14 ticks on the session at 129.32, off earlier highs of 129.83. However, EGBs continue to outperform Gilts and USTs intraday.

- Resistance at the 20-day EMA (130.06) was untested during this morning’s Bund rally, which kept a bearish technical theme intact. A reminder that there wasn’t much in the way of headline flow to explain the early strength.

- Initial support to monitor in Bunds remains the July 14 low at 129.08 Clearance of this level would expose the bear trigger at 128.97, the May 14 low.

- OAT futures are +21 ticks at 122.53, with PM Bayrou’s 2026 budget outline not promoting any meaningful divergence from Bunds. Notably, far-right RN leader Bardella suggested a censure motion was likely if Bayrou was to follow through with the removal of two public holidays.

- Gilt futures are off session lows, but remain -27 ticks at 91.56. UK June inflation headlines tomorrow’s calendar, with labour market data also due on Thursday. A reminder that Chancellor Reeves and Governor Bailey speak at Mansion House later this evening. See our preview here for more.