EM ASIA CREDIT: Vedanta Resources: Expands copper operations in Zambia

(VEDLN, B2/B/B+)

"*COPPERTECH WILL OWN KONKOLA COPPER MINES IN ZAMBIA" - BBG

"*COPPERTECH PLANS TO RAISE COPPER OUTPUT TO 300,000 TONS BY 2031" - BBG

"*COPPERTECH INTENDS TO INVEST AN ADDITIONAL $1.5B IN OPERATIONS" - BBG

Vedanta has launched a new company, US based CopperTech Metals Inc., which will expand production at the Konkola Copper Mines in Zambia's Copperbelt Province. Positive strategic development.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Weak Earnings Data But market Slightly Cheaper

In Tokyo morning trade, JGB futures are weaker, -16 compared to settlement levels, and at session lows.

- August labour earnings data in Japan was comfortably below market expectations. Headline earnings rose 1.5%y/y (against a 2.7 forecast and 3.4% July outcome), while real earnings dipped back to -1.4%y/y (-0.5%) was forecast. Real earnings have not been in positive territory (in y/y terms) so far in 2025. This will reinforce expectations of the BoJ likely remaining on hold at the Oct policy meeting.

- Japan's new political regime had already noted that Oct is too soon for a rate hike. BoJ Governor Ueda also noted recently that the risk was low for the central bank to fall behind the inflation/policy curve (with today's data supporting this theme).

- Cash US tsys are flat to 1bp cheaper, with a steepening bias, in today’s Asia-Pac session after yesterday’s modest rally.

- Cash JGBs are flat to 1bp cheaper across benchmarks, with a steepening bias. The benchmark 10-year yield is 0.9bp higher at 1.694% versus the cycle high of 1.699%.

- Swap rates are 1-2bps higher. Swap spreads are wider.

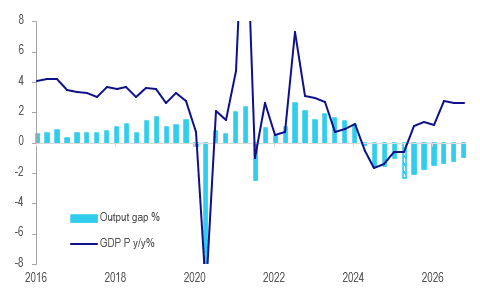

RBNZ: Spare Capacity To Require Further Easing

There are valid arguments for both 25bp and 50bp rate cuts at today’s RBNZ decision. One reason for an outsized reduction is that Q2 GDP contracted by significantly more than the RBNZ projected in August meaning that the degree of excess capacity was larger than it thought at that time. However, arguing for 25bp is that GDP is prone to large revisions and that the output gap may not actually be as large as it currently looks. Whatever the size, there is material spare capacity which is likely to require further easing.

- We have estimated a simple output gap using a Hodrick-Prescott. The current -0.9% q/q for Q2 production-based GDP results in the output gap widening around 1.3pp in the quarter.

- However, the output gap had been negative for the previous four quarters and while the size is difficult to estimate, especially as GDP will be revised in the future, it is clear that there is substantial spare capacity in NZ that requires further monetary easing.

- Using the RBNZ’s quarterly GDP forecasts, our estimate doesn’t have excess economic capacity being worked off until Q3 2027, in two years’ time. This implies that rate cuts could continue into 2026 shifting policy into stimulatory territory.

- The RBNZ estimates the “neutral” rate to be between 2.5% and 3.5%. Consensus has the OCR declining to 2.75% this month but analysts are split with many forecasting 2.5%.

NZ GDP (production) y/y% vs output gap %

Source: MNI - Market News/LSEG

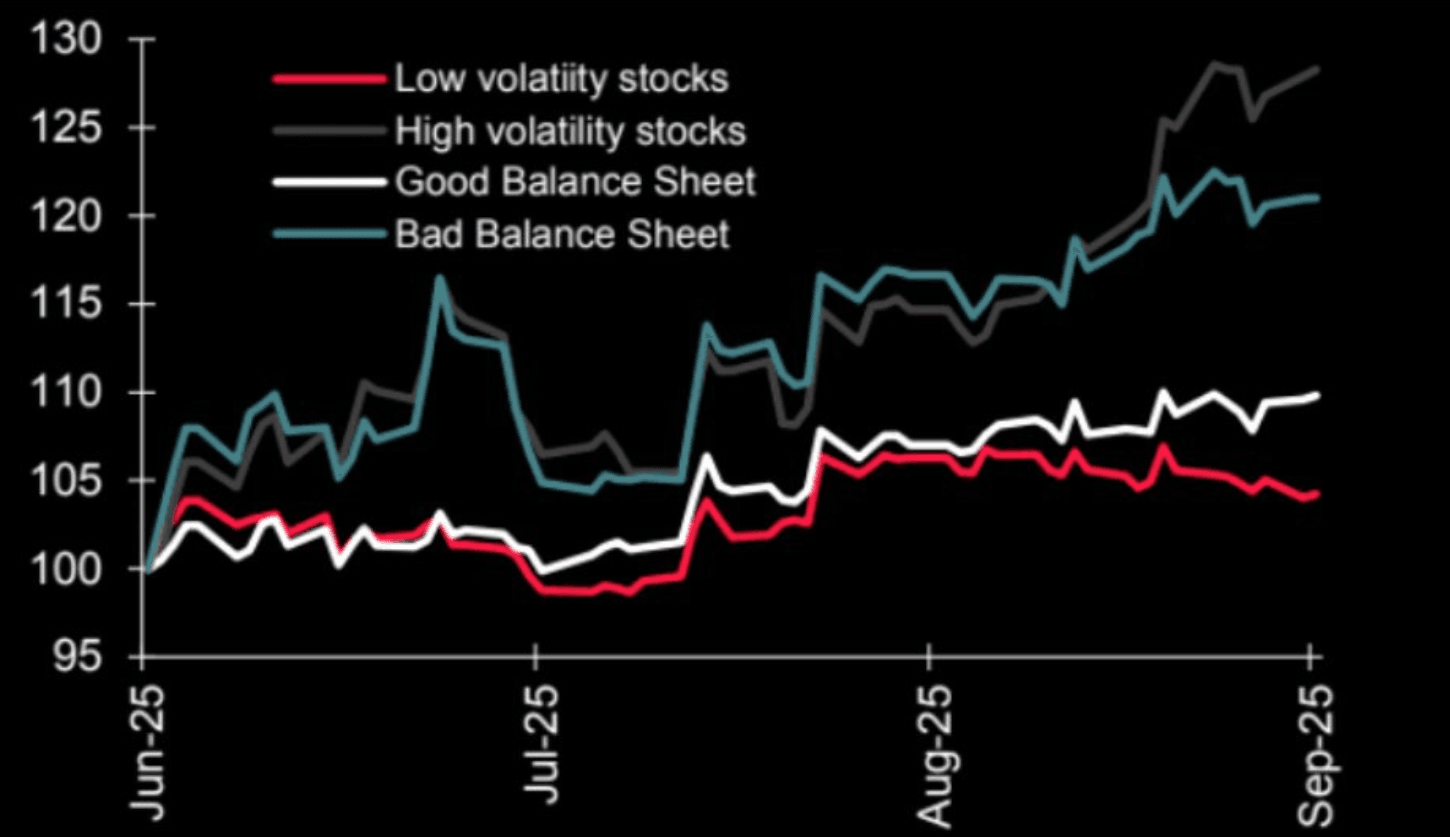

US STOCKS: Russell Index - Rejects 2500, Look For Support Back Toward 2400

The Russell 2000 overnight range was 2451.31 - 2493.10, closing -1.12%. The Russell 2000 took a sharp turn lower after briefly probing above 2500. The move in small caps has been more about positioning as the underperforming and least loved sectors have surged in the past month on short covering and momentum funds buying as new highs are being made. Are we seeing the first signs of this huge move finally running out of steam ? If we do at some point get some sort of a correction then small caps are likely to be hardest hit, the newly built longs will be looking for the price to sustain its break above 2400 and build a base from which to move higher, back through 2350/2400 and these longs will begin to be challenged.

- Lance Roberts on X: “Be careful of that small cap chase. 1) Small caps are the most economically sensitive stocks so much of the speculation hinges on a strong economic rebound. 2) After taxes and interest payments, net income is negative. 3) The majority of the current small cap chase is in high volatility and bad balance sheet stocks. Know what you own.”

- Zerohedge on X: "Incredible Demand": Retail Investors Buy Record-Shattering $100BN Stocks In Past Month.”

Fig 1: High Vol, Bad Balance Sheets Outperforming

Source: MNI - Market News/@LanceRoberts/@themarketear