EM LATAM CREDIT: Vale: Q325 Earnings – Neutral

(VALEBZ; Baa2/BBB/BBB+)

• Revenues rose 9% and adjusted EBITDA climbed 21% while net debt increased 31% YoY, leading to an uptick in leverage to a still very comfortable .8x up from .5x a year ago and down from .9x QoQ.

• VALEBZ 54s were last quoted T+140bp, 37bp tighter since June 30th and 35bp tighter YTD. S&P upgraded the rating to BBB from BBB- last month while Fitch raised the rating to BBB+ from BBB last week.

• In Vale’s main iron ore fines division volume grew 8% and EBITDA rose 20% YoY while the much smaller pellets area was a drag on results with a volume decline of 14% and an EBITDA drop of 35%.

• In other areas, copper EBITDA rose 71% and Nickel improved from a negative EBITDA of USD66mn a year ago to USD114mn in Q3, which was lower sequentially from USD201mn in Q2.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Remains Above Support

- RES 4: 0.6763 1.382 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 2: 0.6660/6707 High Sep 18 / 17 and key resistance

- RES 1: 0.6628/29 High Sep 24/30 & Oct 01

- PRICE: 0.6602 @ 16:31 BST Oct 1

- SUP 1: 0.6527/21 61.8% of the Aug 21 - Sep 17 bull leg / Low Sep 26

- SUP 2: 0.6484 76.4% retracement of the Aug 21 - Sep 17 bull leg

- SUP 3: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

The AUDUSD uptrend remains intact and recent weakness appears to have been a correction. Attention is on support at the 50-day EMA, at 0.6554. A clear break of this average would signal scope for a deeper retracement and expose 0.6527 once again (pierced), a Fibonacci retracement. For bulls, a stronger reversal higher would refocus attention on 0.6707, the Sep 17 high. Initial firm resistance to watch is 0.6628, the Sep 24 high.

US TSYS: Taking Delayed/Suspended Data In Stride As Shutdown Gets Underway

- Treasuries look to finish higher - off first half highs after September's ISM Manufacturing Report showed a slight if uneven improvement in sectoral activity. Rates initially gapped higher after much lower than estimated private ADP employment numbers.

- The ADP release for September was weak, showing the biggest private payrolls drop (-32k) since March 2023 and before that, Jun 2020. And the prior 54k was revised down to -3k, so the first back-to-back drops since the pandemic. This was a significant miss for private payrolls versus +51k expected.

- ADP was re-benchmarked, however, resulting in a reduction of 43,000 jobs in September compared to pre-benchmarked data. The trend was unchanged; job creation continued to lose momentum across most sectors."

- Underlying futures climbing again after paring back from late morning highs. Projected rate cut pricing gaining vs. late Tuesday levels (*): Oct'25 at -25.3bp (-24.2bp), Dec'25 at -46.9bp (-44.2bp), Jan'26 at -58.8bp (-53.7bp), Mar'26 at -70.0bp (-64.7bp).

- Thursday's scheduled economic data largely delayed/suspended due to the shutdown - weekly jobless/continuing claims as well as Factory New Orders will not be released

- In other news: Supreme Court rejects Pres Trump's firing of Fed Gov Cook - until at least an oral argument on the case is heard in January 2026. VP Vance expects federal layoffs to start in the next one to two days.

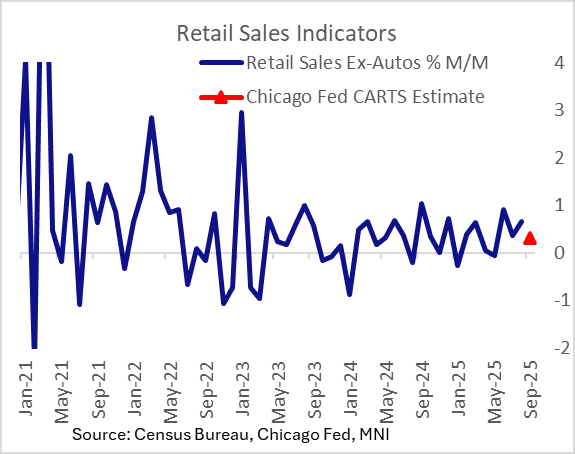

US DATA: Chicago Fed Eyes Solid Ex-Auto September Retail Sales

The Chicago Fed's Advance Retail Trade Summary (CARTS)'s preliminary estimate for September Retail sales ex-auto is 0.3% M/M.

- Coming after 0.7% M/M gains in this retail sales aggregate in August, this would be a 3-month low, but still suggest that underlying strength remains after a strong few months: it would translate into 6.1% 3M/3M annualized growth for this category, the fastest since November 2023.

- There is not yet consensus for the September retail sales report and not even certainty we will get one on Oct 16 as scheduled from the Census Bureau given the federal government shutdown, but so far the indicators for September (including Redbook same-store sales) have pointed to relatively solid dynamics in the month.

- The final CARTS estimate is published on Oct 15.

- One last major piece of the puzzle is auto sales, for which we should get data from Wards Automotive later on Wednesday.