THB: USD/THB Slightly Lagging Weaker USD/Higher Gold Prices

USD/THB continues to consolidate close to recent lows. The pair was last in the 31.70/75 region, up a little over 0.15% versus end Tuesday levels. Recent lows at 31.61 remain intact, despite fresh USD weakness and a further record high in gold in Tuesday trade.

- Any divergence between USD/THB and broader USD index levels, or gold, remain quite modest though from an historical stand point.

- Outside of broader USD risks (which will likely be dictated by the upcoming Fed meeting out come and outlook), focus will be on the new government's efforts to curb baht gains/outperformance, with an emphasis on reducing the correlation with gold prices.

- Outgoing BoT Governor, Sethaput Suthiwartnarueput (his terms end at the end of this month), stated late yesterday that a tax on gold transactions is one policy under consideration, but Sethaput stressed that any decision may take time to reach, given the various stake holders involved.

- Elsewhere the SET equity index is holding above 1300, close to fresh multi month highs. We are down slightly today, but this is following gains in the previous 8 sessions. On the data front, the industrial sentiment index eased down to 86.4 in Aug, from 86.6.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

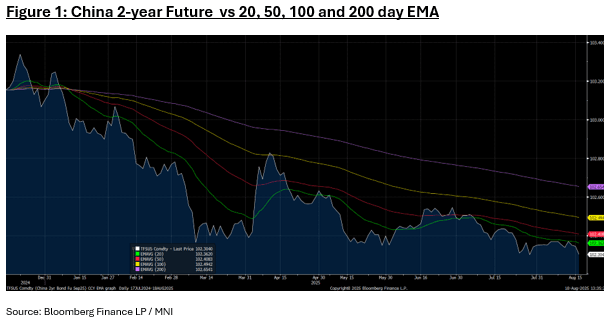

CHINA: Bond Futures Fall in Weak Start to the Week

- China's bond futures are down in the morning session, with their biggest one day fall since May.

- The 10-year is down -0.32 at 108.00, taking it further below all major moving averages. The nearest, the 20-day EMA, is at 108.45.

- The 2-year bond future is down -0.04 at 102.30. Having approached the 20-day EMA of 102.36, today's falls see it move further below.

- The CGB10 year continues to drift higher, following on from moves on Friday. Having finished Friday at 1.74%, it is up +3bp today at 1.77%, the highest level of the month.

ASIA STOCKS: Most Markets Higher, China Outperforms, South Korea Weaker

Asian equity markets are mostly on the front foot in the first part of Monday dealings, although there are some pockets of weakness. The lead from US markets on Friday was softer, particularly in the tech space. US futures are up a touch in the first part of Monday dealings, while EU futures are also higher. Market attention remains on US-Ukraine talks later, with focus on whether a peace deal to end the Russia-Ukraine conflict can be reached. The knee-jerk reaction from any peace deal reached is likely to be positive for risk appetite.

- China markets are outperforming, particularly given a flat HSI backdrop in Hong Kong. The CSI 300 was last up a little over 0.90%, putting the index near 4240, which is fresh intra-session highs back to early Oct last year. Hopes of fresh stimulus after disappointing July data is aiding sentiment, while there is also talk of outflows from bonds into equities. US President Trump also stated late last week that he will hold off raising China tariffs over their Russian oil purchases.

- Japan markets are higher, the Topix +0.55%, the NKY 225 up close to 0.90%. The Topix transport sub index is up close to 1.50%, continuing a recent solid run.

- South Korean markets have returned after Friday's break and are off over 1%, putting the Kospi back under 3200. Taiwan stocks are holding up better, despite a Friday slump in the US SOX index.

- Australia's markets is around flat, as we sit near record highs.

- In South East Asia, trends are mixed. Singapore is softer, but Malaysia and the Philippines have ticked higher. Indonesian markets are out today.

US: Viewpoint On The AI Cycle

Adam Butler the CIO of ReSolve Asset Management wrote a thread on X giving his view that the AI cycle could very well be over. It received quite a lot of attention over the course of last week below are some key excerpts: https://x.com/GestaltU/status/1954561703967867019

- “I’ve got bad news. The AI cycle is over—for now. I’m still convinced it will take the wider economy years—maybe decades—to fully digest the productivity shock we’ve already uncorked. But the curve we’ve been riding just flattened into a long plateau.’

- “The problem isn’t that the models stopped improving. It’s that the improvements we need are measured in orders of magnitude, not percentage points. Every step up the scaling laws now demands a city’s worth of electricity and a sovereign wealth fund’s worth of GPUs.”

- “What comes next is not the next spectacular demo but the quiet absorption of today’s tools into the 80 percent of the economy that still runs on Excel and email. The productivity gains are real; they’re just not cinematic.”

- “For investors, treat “AI” the way we treated “mobile” circa 2011: infrastructure bets can still clear the hurdle rate if you triple the time discount, but the application layer is a graveyard of demos wearing revenue costumes.”

- “To my fellow zealots: we are not going back to the pre-2022 world. The ceiling just got higher, but the ladder is longer than we thought. That isn’t failure; it’s physics. The next breakthrough will arrive; maybe from a grad student with a sparse attention kernel, maybe from a national lab running a ten-gigawatt reactor. Until then the boring work of integration is the only game in town.”

- “So breathe. Ship the eval harness. Close the ticket. And remember: exponential curves always look flat when you zoom in too close.”