PHP: USD/PHP Dips After Record High, Outperforms EM Asia FX

USD/PHP is holding lower, last near 59.10/15. This is down around 0.45% and the best performer in EM...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBA: Discussion Around Prolonged Pause Or Hike Given Upside Inflation Risks

Governor Bullock clarified that a rate cut was not considered or even suggested as an option at the December meeting and that the 2026 discussions are likely to be around whether to leave rates at 3.6% or increase them. The Board is uncomfortable with where inflation is and private demand is now taking over from the public sector and so further easing is not “on the horizon for the foreseeable future”. Rates will continue to be decided on a meeting-by-meeting basis and be driven by the data.

- A rate hike wasn’t explicitly considered in December but the Board discussed what needs to happen for it to occur, which includes quarterly CPIs showing more inflation persistency signalling that there are greater capacity pressures and less restrictive financial conditions. She noted that with growth likely around potential, there isn’t much room to grow without price pressures.

- The Board is now more focussed on inflation. If it stays high, then it will have to do “something”. It is particularly looking at market services, new dwelling and durable goods prices.

- Bullock observed that the market is trying to predict the RBA’s reaction function and is reacting to the data. She said that the market is right that the Board is thinking about upside risks and that it is alert but wants more evidence. She wouldn’t comment on the timing of market priced hikes.

- 6 months ago risks were to the downside, which have abated, but upside ones have been “generated” and therefore there was no consideration to cut. Bullock noted that the Board needs to be flexible as conditions change.

US TSYS: Yields Trend Higher in Afternoon Trade (amended)

Bond futures turned down in the afternoon with the US-10-Yr falling to 112-06. Having traded up at 112-11 it lost ground in the afternoon session. TYH6 is at the mid-point between the 100-day EMA of 112-14+ and the 200-day EMA of 111-29+.

Cash was weak with yields up to +1.3bps higher in the mid-part of the curve.

- The 2-Yr is up +0.9bps at 3.586%

- The 5-Yr is up 1.2bps at 3.76%

- The 10-Yr is up 1.2bps at 4.178%

- The 30-Yr is up +1.0bps at 4.813%

The 10-Yr remains in the 4.00% -4.20% range that has held in recent weeks. A more hawkish outlook from the FED could see new ranges established, particularly for the 10-yr.

Tuesday Data Calendar in the US: ADP Weekly, Redbook and JOLTS for Sep/Oct; Treasury auctions include $39B 10Y note reopen.

Tonight sees a US$75bn 6-week bill auction and a US$39bn 10-Yr auction.

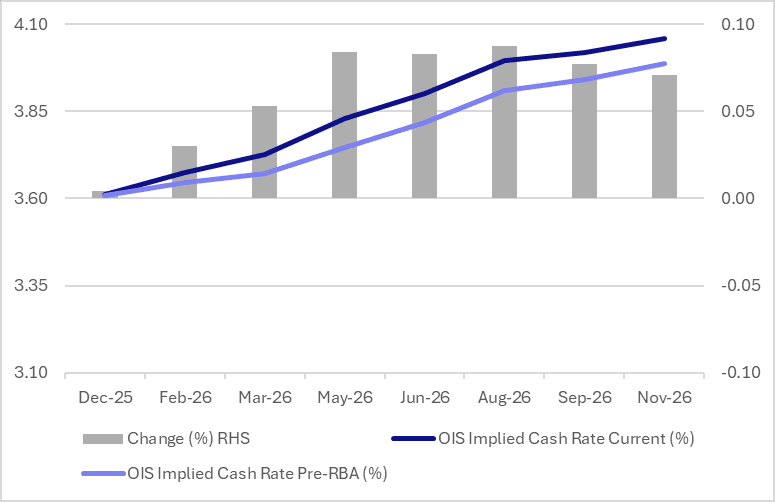

AUSSIE BONDS: Market Cheapens During RBA Governor Presser

ACGBs (YM -11.0, XM -6.5) cheapened sharply during Governor Bullock’s post-meeting press conference. While markets initially took the decision and accompanying statement in stride, her comments were interpreted as distinctly more hawkish, prompting a swift repricing

- Bullock signalled that inflation risks have shifted to the upside, with recent data suggesting more economic tightness than previously thought. The RBA is cautious about over-interpreting the new monthly CPI but is alert to any broad-based pickup in inflation.

- The Board did not consider rate cuts and does not expect them in the foreseeable future.

- Overall, downside risks have faded and upside risks have grown. The policy debate is now between an extended pause or potential hikes, with the Board uncomfortable about current inflation and guided strictly by incoming data.

- Cash ACGBs are 6-11bps cheaper, with the AU-US 10-year yield differential at +58bps.

- The bills strip has bear-steepened, with pricing -2 to -13.

- RBA-dated OIS pricing is 1-8bps firmer versus pre-decision levels. Tightening expectations are seen across all meetings, with the probability of a 25bp hike rising from 28% for February to 119% by June and 190% by December 2026.

- Tomorrow, the local calendar will be empty.

Bloomberg Finance LP