PHP: USD/PHP Breaks Higher, Implied Vols Stay Contained

USD/PHP has broken to fresh record highs in the first part of Wednesday trade, we were last in 59.30-35 region. Session highs rest at 59.36. Outside of broader USD gains from Tuesday's session, there seems little in the way of fresh PHP negatives. Recent themes of the BSP not targeting USD/PHP levels (but rather the pace of PHP depreciation and its impact on local inflation) has potentially given a green light to PHP bears. Earlier in the week the government also raised its USD/PHP projection to 58-60 for 2026-28 from 56-58 prior.

- Upside focus may now at 59.50 then ultimately 60.00, albeit with one eye on the pace of PHP depreciation pressures given BSP rhetoric. Even with this break higher in spot, 1 mth implied vols are only modestly higher at +6%.

- It would likely take a move under the 50-day EMA (58.73) to re-assess the bullish outlook in the pair. We aren't yet overbought per RSI (14).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

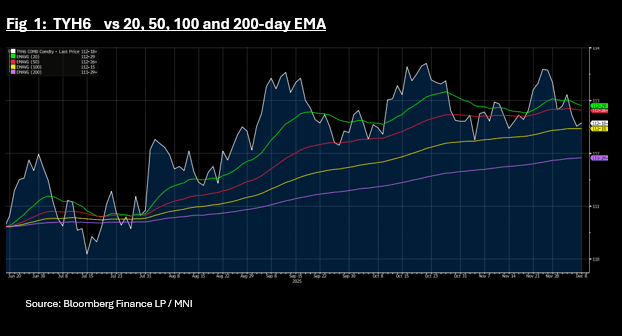

US TSYS: Yields Lower as TYH6 Fails Key Tech Resistance

US bond futures have edged higher in the Asia morning session, with the 10-Yr failing to break below a key technical. Opening at 112-18+ TYH6 was near to the 100-day EMA of 1132-15+ but has bounced higher in early trade to be up by +02 to 112-18+

Cash is stronger across the curve with yields -0.2 - -0.6 lower with short and intermediate maturities outperforming.

- The 2-Yr is at 3.556% -0.6bps

- The 5-Yr is at 3.708% -0.5bps

- The 10-Yr is at 4.133% -0.4bps

- The 30-Yr is at 4.791% -0.2bps.

Ahead tonight is a 13 and 26 week bill auction, with the focus being the U$58bn 3-Year auction.

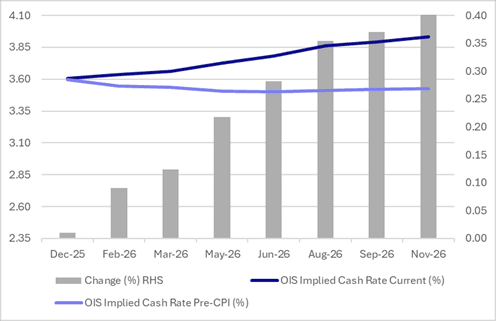

STIR: RBA-Dated OIS Pricing Fully Prices Hike By August 2026

RBA-dated OIS pricing is slightly firmer today, showing tightening across all meetings, with the probability of a 25bp hike rising from 2% tomorrow to 105% by August and 141% by December 2026.

- After today’s move, pricing is 9-40bps firmer across the curve beyond December 2025, than pre-Monthly CPI levels (26 November), led by December 2026.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

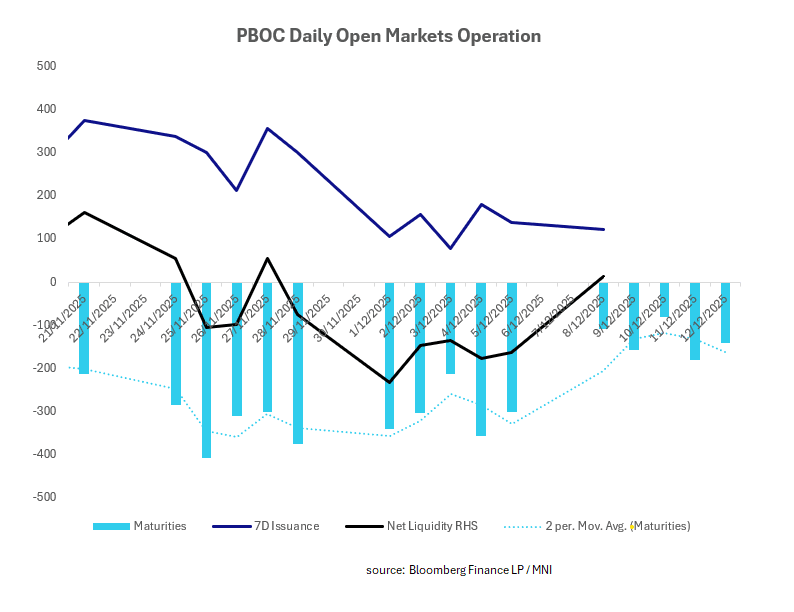

CHINA: Central Bank Injects CNY14.7bn via OMO

Last week the PBOC withdrew 7-day liquidity, adding 3-month liquidity. The week ahead has (relative to last) a more moderate redemption schedule and likely to see the resumption of some moderate injections.

- The PBOC issued CNY122.3bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY107.6bn.

- Net liquidity injects CNY14.7bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.43%.

- The China overnight interbank repo rate is at 1.31%, from the prior close of 1.31%.

- The China 7-day interbank repo rate is at 1.40%, from the prior close of 1.40%.