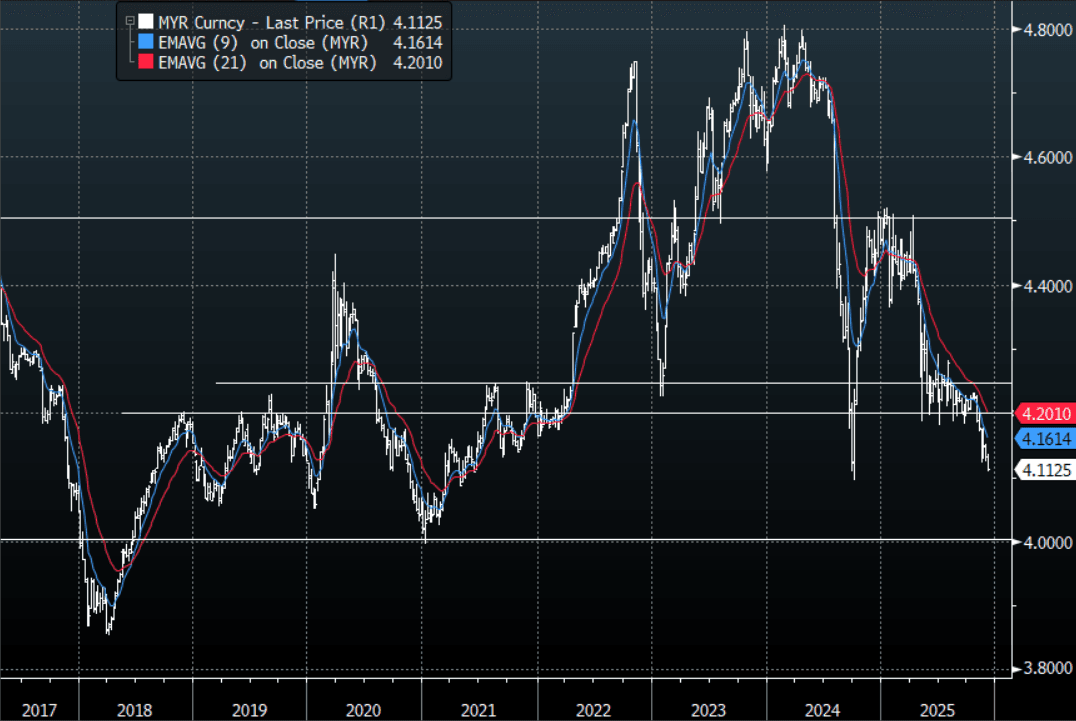

MYR: USD/MYR - Trades Heavy, If PBOC Continues To Push Back Can It Bounce ?

The overnight range was 4.1085 - 4.1163, closing around 1411.25. The pair continued to trade heavily all of yesterday even in the face of pushback from the PBOC. Today EM/Asia will be watching the CNY fix again to see how serious China is about fighting the weak USD. USDMYR has opened marginally weaker at 4.1178. The current downtrend remains in place though so I would be looking for bounces to be faded unless we have something more structural to change the current sentiment. On the day I suspect bounces toward 4.1300-1400 should find resistance initially should we see a bounce.

- The USD/MYR Average True Range for the last 10 Trading days: 110 Points

- Data/Event : Foreign Reserves

Fig 1 : USD/MYR Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

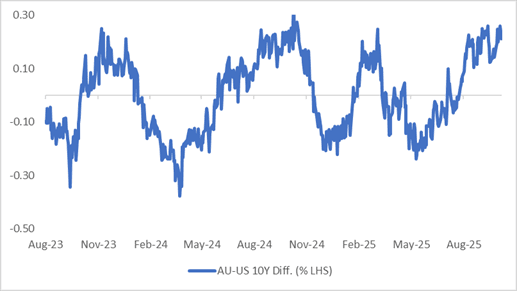

AUSSIE BONDS: A Strong Day For ACGBs But AU-US10Y Diff Sits Near Top Of Range

Cash ACGBs are 5–7bps richer on the day, while the AU–US 10-year yield differential is little changed at +24bps.

- At this level, the spread remains near the upper end of the ±30bps range that has persisted since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is close to fair value.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has increased around 75bps since June to be around the same level as October 2024.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

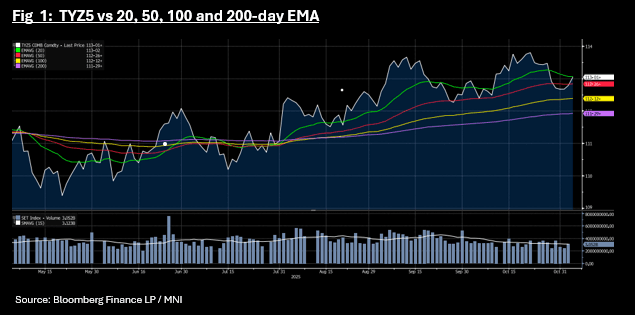

US TSYS: Rally Continues, TYZ5 Approaches Key Technical

Overnight moves in Treasuries spilled over into Asia today with bond futures stronger and yields lower. The 10-Yr bond future is up +08 at 113-01+ taking it near to the 20-day EMA of 113-02+. It has traded below since just prior to the last FED where for some observers, the December rate cut became uncertain. The boost for bonds overnight came from the weakening in equities on profit taking.

Cash has opened up very strong with yields across the curve -3 - 3.5bps lower. The 2s10s curve has flattened modestly.

- The 2-Yr is at 3.549 (-2.9bps)

- The 5-Yr is at 3.663% (-3.5bps)

- The 10-yr is at 4.054% (-3.1bps)

- The 30-Yr is at 4.642% (-2.4bps)

Equity weakness is a key theme for markets today with major markets down and recent star performers like the KOSPI and NIKKEI down over 4% as the tech sector is hit hard. The warning from the Korea Exchange yesterday on SK Hynix was an indicator as to how far these tech stocks have run and were long overdue a correction.

CNH: USD/CNY Fixing Back Above 7.0900, But CNH Outperforming Higher Beta Plays

The USD/CNY fix edged higher earlier, printing at 7.0901, against a 7.1328 market consensus forecast. The fixing is back near late Oct levels, while the error term widened further to -427pips from -363pips yesterday. USD/CNH sits near 7.1345 in latest dealings, little changed for the session. CNH should outperform higher beta plays during this bout of risk off in markets. AUD/CNH continues to to tracks towards 4.6000 (last 4.6150). A short while ago the RatingDog Services PMI printed, which was 52.6, against a 52.5 consensus forecast and 52.9