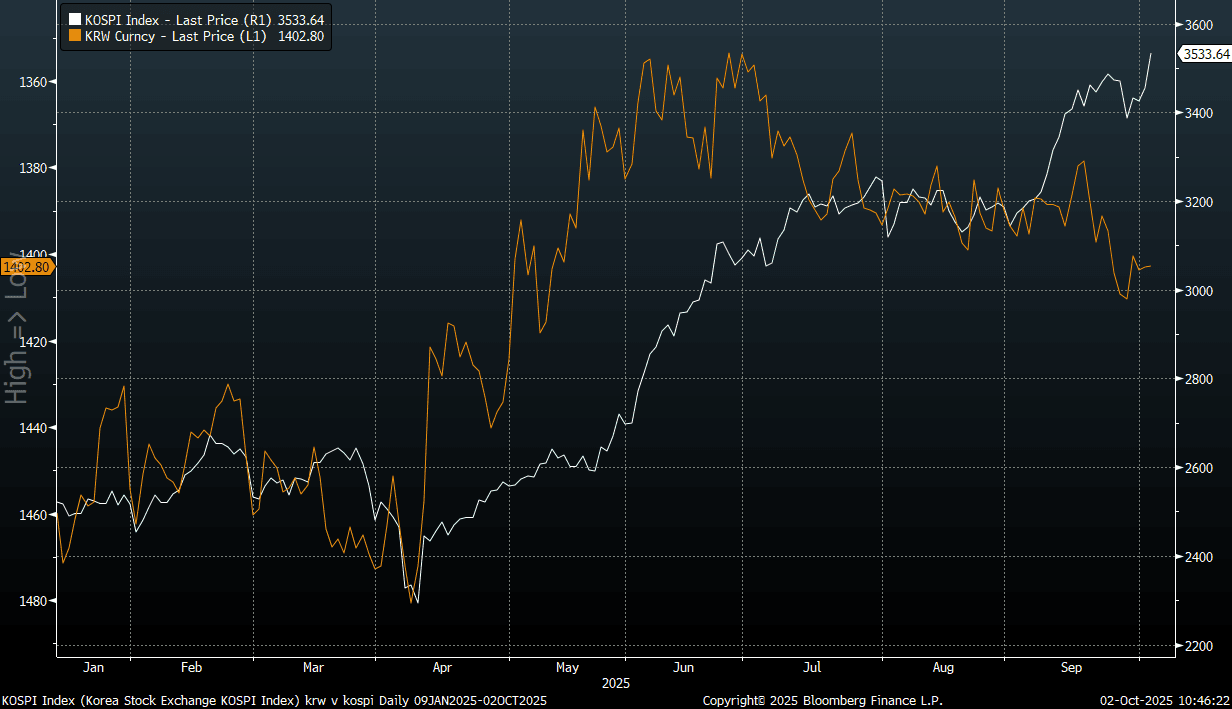

KRW: USD/KRW Holding Above 1400 Despite Equity Rally/Lower US Yields

Spot USD/KRW sits near 1403/04 in latest dealings, slightly down on end Wednesday levels. We are sub late Sep highs (near 1414) but the better equity tone for local stocks so far today isn't providing much positive spill over for the won. On the downside, all the key EMAs are under 1400, the 50-day around 1392.25.

- The Kospi has surged in early Thursday trade, up over 2% before gains were slightly pared. This puts the index to fresh record highs above 3500, via BBG: "Samsung Electronics Co. and SK Hynix Inc.’s shares rose sharply after Korea’s largest companies forged initial agreements to supply chips to OpenAI’s Stargate project, reinforcing their lead in advanced AI memory."

- Offshore investors have bought $356mn of local stocks so far today. This adds to net inflows already seen this week.

- The chart below shows the divergence between USD/KRW spot and local equities. USD/KRW spot also looks too high relative to US-SK 1y1y rate differentials (this spread last at +51bps).

- Trade deal uncertainty may be continuing to keep USD/KRW spot supported. Earlier headlines crossed via Rtrs: "SOUTH KOREAN FOREIGN MINISTER CHO SAYS U.S. IS REVIEWING CURRENCY SWAP WITH SOUTH KOREA BUT TELLS SEOUL IT ISN'T OPTIMISTIC -YONHAP"

- On the data front, Sep CPI was close to market expected but a step up from the Aug pace, with headline CPI at 2.1%y/y (prior 1.7%). The Aug current account and goods balance both narrowed, but remained healthy above $9bn.

Fig 1: Spot USD/KRW & The Kospi Index

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

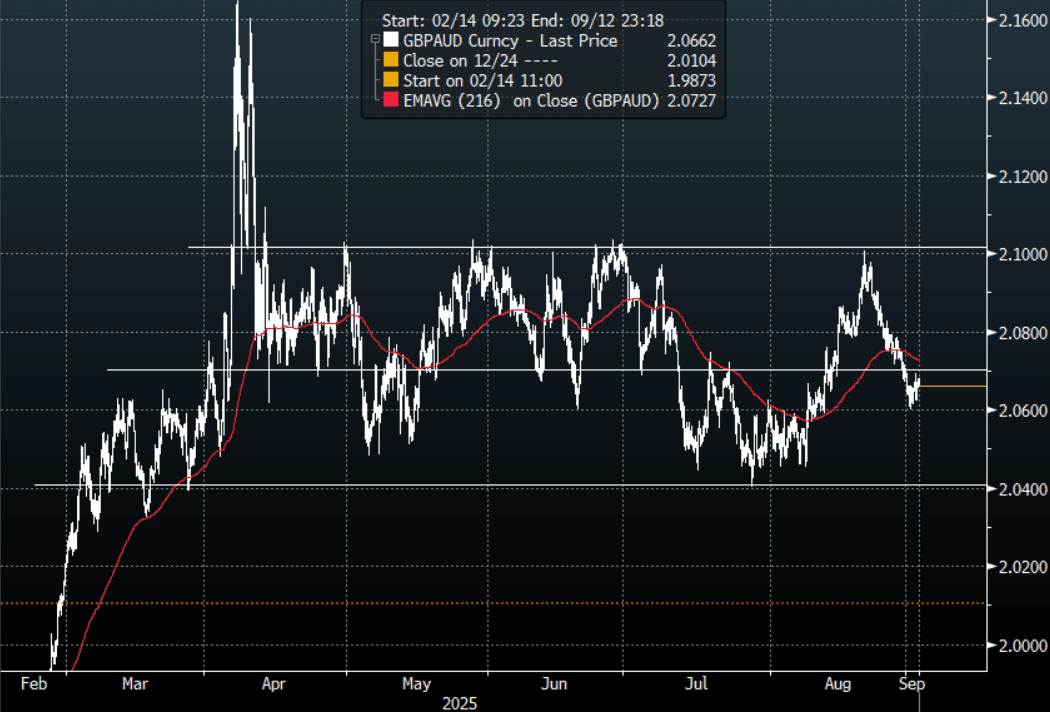

FOREX: AUD Crosses - Consolidate Recent Gains, Within Ranges

US Equities had a quiet night with the US being off on holiday. The S&P remains in a bullish uptrend, and for the moment is ignoring all headwinds. US Futures have opened slightly lower this morning, E-minis -0.10%, NQU5 -0.10%. The AUD was helped by the return in risk appetite at the end of last week and is consolidating those recent gains, albeit within some clearly defined ranges.

- EUR/AUD - Overnight range 1.7854 - 1.7933, Asia is currently trading around 1.7870. The area just above 1.8100 has seen decent supply cap it the last few months, a sustained move above 1.8100 is needed to see the move regain momentum higher. The pair has drifted back towards its first support around the 1.7800 area, expect some demand here first up, below there next support is around 1.7600.

- GBP/AUD - Overnight range 2.0624 - 2.0694, Asia is trading around 2.0665. The pair is probing just below the 2.0700 pivot within its wider 2.0450-2.1050 range where you could expect some demand first up. If this level can’t hold the focus will turn back to the range lows towards 2.0450.

- AUD/JPY - Overnight range 96.06 - 96.59, Asia is trading around 96.50. The pair is probing above the 96.50 area this morning. A sustained move back above 96.50 would turn the trend higher again but until then sellers should be around looking for this move to top out.

- AUD/NZD - Overnight range 1.1086 - 1.1112, the cross is dealing in Asia around 1.1100. Momentum higher looks to have stalled above 1.1100 for now, look for demand to return on a dip back towards the 1.1000 area.

Fig 1: GBP/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

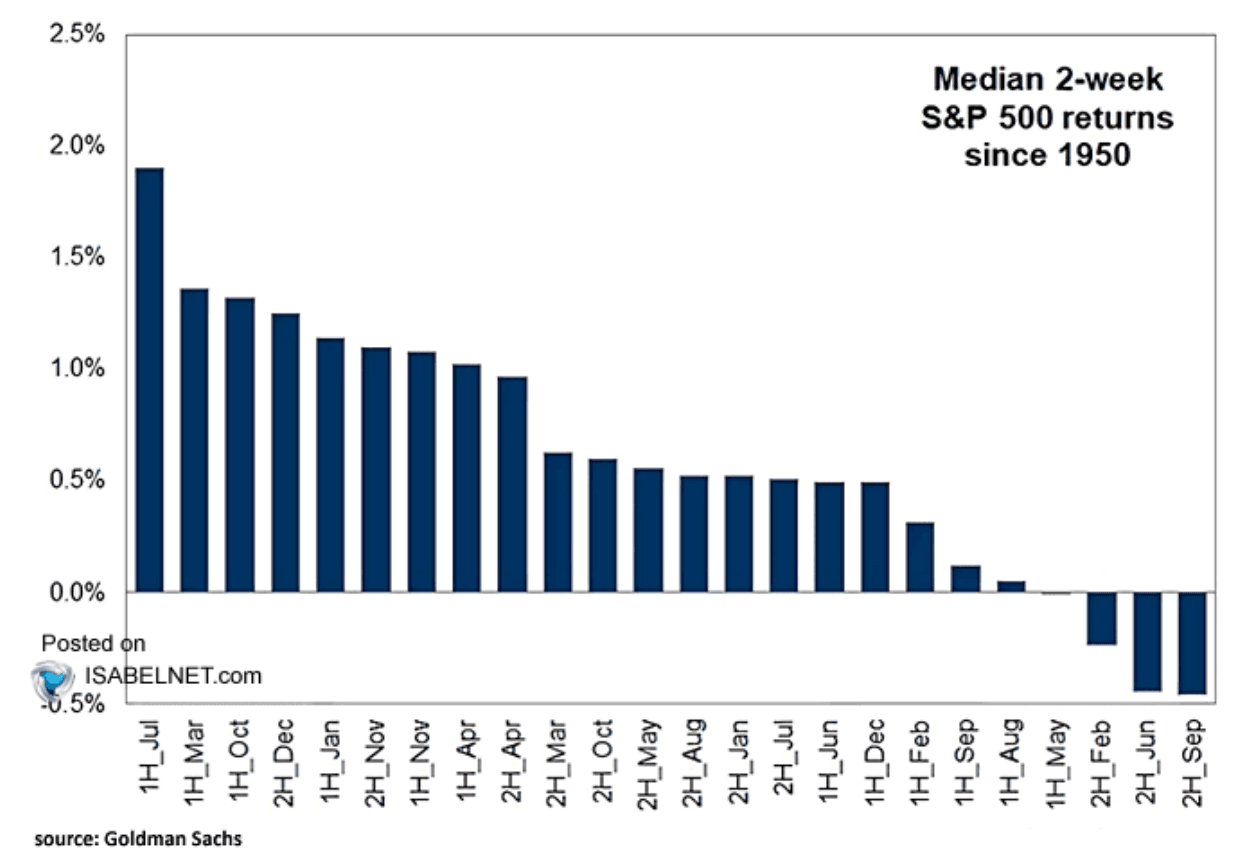

US STOCKS: S&P Momentum Stalling Towards 6500, Focus Turns To NFP

The S&P(ESU5) overnight range was 6459.50 - 6485.00, Asia is currently trading around 6468, -0.10%. A quiet night with the US being off on holiday. The S&P remains in a bullish uptrend, and for the moment is ignoring all headwinds. We head into September which traditionally is the worst month for US Equity performance, will stocks continue to ignore seasonality like it did in August? This morning futures have opened a little lower, E-minis -0.10%, NQU5 -0.10%. The market will be eyeing NFP on Friday, hoping for a catalyst to reignite momentum which has been stalling.

- (Bloomberg) - “AI Theme Turns 2-Way Street as China Accelerates. Chinese equities are getting an extra lift from signs that the AI boom there is gathering pace. Coming as that does after the DeepSeek revelations earlier this year, the positives for the theme in China are also threatening to feed some of the burgeoning unease about the possibility that valuations are overstretched for US-centered tech stocks.”

- “The S&P 500 can soar another 20% by the end of next year on the back of an AI-driven tech revolution, according to Evercore ISI strategists, whose 7,750 target for 2026 is the Street’s highest so far.” - BBG

- ISABELNET on X: "S&P 500 - Since 1950, the first half of September has been a seasonally weak period for the S&P 500, ranking as the sixth weakest half-month in the annual cycle." See Chart Below.

- zerohedge on X: “Systematic Demand Has Dried Up': Goldman's Flows Gurus Expect September To Be "Challenging."

- Daily Chartbook on X: "Analysts expect [Mag 7] earnings growth to stabilize over the next six quarters, but still deliver double-digit growth. The baton is being passed to the S&P 493, whose earnings are expected to accelerate into the mid double-digits by Q3 2026." - @mattcerminaro @callieabost.

Fig 1: Median 2-Week S&P Returns

Source: MNI - Market News/@ISABELNET_SA/Goldman Sachs

US TSYS: Cash Open

TYZ5 is trading 112-10, down 0-06 from its close.

- The US 2-year yield opens around 3.633%, up 0.02 from its close.

- The US 10-year yield opens around 4.2575%, up 0.3 from its close.

- MNI: Congress returns to Washington, D.C. on Tuesday, after the Labor Day holiday. Lawmakers face a race to reach a deal on a continuing resolution to avoid a federal government shutdown ahead of the 30 September deadline, when funding is set to expire.

- Bloomberg - “Trump’s tariffs will stay in place until at least mid-October amid a legal fight, Capital Economics said. Should the president ultimately lose, Bloomberg Economics estimates the average US effective rate of 16.3% would be cut by at least half.”

- 10-Year Yields continue to find supply toward the 4.20% area, which signals the range might continue to dominate. A break of the recent lows around 4.18% would bring the bottom of the range towards 4.10% back into focus.

- Data/Events: S&P Manf. PMI, ISM Manf., Construction Spending