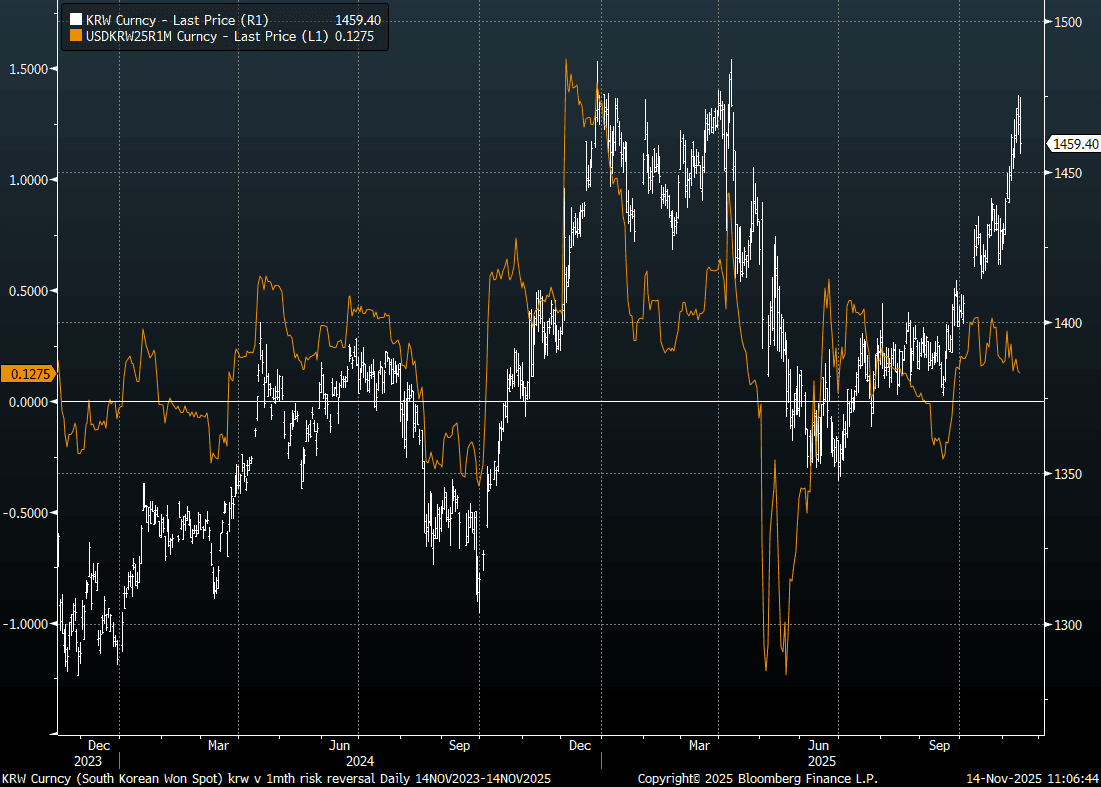

KRW: USD/KRW Finds Demand Under 1460, Watching Risk Reversal Trends

Spot USD/KRW has stabilized near 1460 in latest dealings (session lows at 1456). We are up around 0.40% in terms of gains for the session so far. NDF volumes are once again higher for this time of day per DTCC, last near $1.8bn, around 94% of total NDF volumes recorded by DTCC. Implied vols are firmer, but only back close to earlier Nov highs. The 1 month was last around 8.38%. Risk reversals are lower, the 1 month at just under 0.1300. If history is a guide if we dip sub 0, and trend more towards puts favoured over calls in the pair, spot USD/KRW losses could accelerate.

- The chart below plots spot USD/KRW versus the 1 month risk reversal. The horizontal line representing 0 from a risk reversal standpoint. Moves under flat for the 1 month risk reversal, particularly towards -0.25, have coincided with sharper moves lower in USD/KRW spot in recent years.

- In the cross asset space, local equities are down close to 2.5% amid negative tech spill over from Thursday US trade. Offshore investors have sold over $500mn of local stocks, reversing a good proportion of yesterday's inflows.

- Such trends are likely providing some offset to the step up in policy rhetoric from earlier around addressing FX supply/demand imbalances.

Fig 1: USD/KRW Spot & 1 month Risk Reversal

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBA: RBA’s Hunter Notes It Is Monitoring Housing & US-China Trade Developments

RBA Assistant Governor (Economic) Hunter said today that the RBA is looking to keep inflation close to the current rate which is around 2.6/2.7% for the trimmed mean. She noted that inflation expectations remain anchored and that the central bank is monitoring housing & resumption of US-China trade tensions. Her commentary on recent economic developments was consistent with the 30 September meeting minutes. There was nothing to suggest thinking for the 4 November decision. The Board remains flexible and highly data dependent.

- Hunter commented that dwelling prices had reacted to 2025’s easing as expected but with stronger housing and market services CPI components, it will be monitoring growth in the housing market.

- She wouldn’t give an estimate of the “neutral” rate but said that it is a range and only a guide.

- She also spoke on the impact of the RBA’s August downward revision to medium-term productivity growth to 0.7% from 1.0%, which was driven by an assessment that the slowdown was at least partially structural and therefore not temporary.

- The change reduces long-term nominal wage growth that is consistent with the 2.5% inflation target mid-point by 0.3pp to 3.2%. The RBA believes that consumers have already adjusted their spending to lower productivity and wage growth. Consumption per person is positively correlated with productivity.

- With potential growth revised down to 2% from 2.25%, 0.5% q/q GDP prints are now consistent with supply and demand in balance and inflation steady, whereas previously that was considered soft growth. As a result, the GDP profile was revised down but still showing a recovery.

ASIA STOCKS: Taiwan Sees Outflows, While India More Positive On Rate Cut Hopes

Asia Pac net equity flows have been mixed to start the week. South Korea has seen mixed trends since onshore markets returned from the early Oct break. We are positive for the past 5 trading days, but aggregate sums remain below recent highs. The Kospi is just below record highs, while focus remains on local chip makers linked into the global tech/AI boom. Sentiment in this space remains positive, but we have had a very strong run higherin recent months. In contrast, inflows into Taiwan have clearly lost momentum, with $2.3bn in net outflows for the past 5 trading days. Price action in the Taiex has been choppy in the past week, with offshore investors potentially taking some profit after most of Sep saw quite strong inflows (+$7.3bn for the month)

- Elsewhere, inflow momentum has been stronger into Indian markets, over $1.2bn in the past 5 trading days. Inflation outcomes have given hope to easier RBI policy settings, although local equities are struggling to build on earlier Oct gains.

- In South East Asia, outflow pressures have mostly been evident, although Indonesia's 5-day sum remains positive.

- Outflows from Malaysia have been most prominent from a trend standpoint, with local equities down sharply from earlier Oct highs abvoe 1650.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 311 | 582 | 2671 |

| Taiwan (USDmn) | -411 | -2313 | 7563 |

| India (USDmn)* | 400 | 1251 | -16526 |

| Indonesia (USDmn) | -82 | 133 | -6175 |

| Thailand (USDmn) | -88 | -163 | -3028 |

| Malaysia (USDmn) | -76 | -376 | -4116 |

| Philippines (USDmn) | -6 | -10 | -703 |

| Total (USDmn) | 49 | -894 | -20314 |

| * Data Up To Oct 13 |

Source: Bloomberg Finance L.P./MNI

US TSYS: Treasury Yields Grind Lower at Open of Asia Trading Day

As cash bonds set up for another trading day, futures had guided prices marginally lower after the overnight rally in the US. As TYZ5 trades down -01+ at 113-11 bond yields are opening up marginally lower.

- The US 2-Yr is at 3.381%, close to 0.5bp lower in early trade.

- The US 5-Yr is at 3.607% having closed prior to Columbus day at 3.626%.

- The US 10-Yr is down -0.5bps to 4.028% having failed to test 4.00% prior. It had looked likely to remain in the 4.00% - 4.20% range for now, seeking a fresh catalyst to break out.

- The US 30-Yr is down -0.5bps at 4.628%

- The catalyst for the overnight rally was comments from Fed Chairman Powell indicating that the outlook for inflation and employment appears to have changed little since September, keeping intact expectations for two more rate cuts this year.

- Key data in the calendar for later is Empire Manufacturing which is forecast to decline -1.8 following -8.7 in September and Real Average Hourly Earnings.