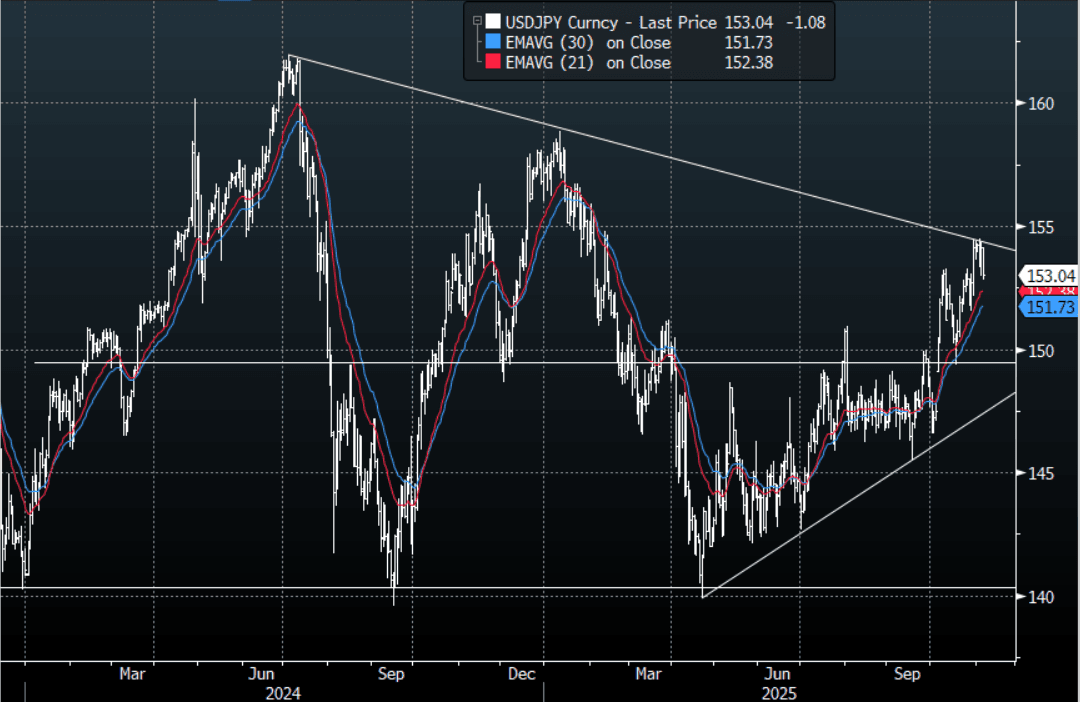

JPY: USD/JPY - Fails Above 154.00 Again, JPY Being Bought In The Crosses

The overnight range was 152.83 - 153.98, Asia is currently trading around 153.05. The pair failed again above the 154.00 area as cross-Yen came back under pressure as risk turned lower again. A lot depends on what your view is for risk from here, should the price action of the last few days signal we could be putting in a potential top and a correction in risk plays out then I suspect the resistance around the 154/155 area should continue to offer solid resistance. With the crosses under pressure we could see some further pullbacks and rallies on the day toward 153.50 should find sellers, but I do think any correction lower will still find buyers happy to fade. The first buy zone is toward 151.50-152.00 and then the more important 149.00-150.00 area.

- MNI INTERVIEW: Ex-BOJ's Kameda Sees Dec Hike, Ueda Not Dovish. The Bank of Japan is likely to raise its 0.5% policy rate 25 basis points in December at the earliest, following Governor Kazuo Ueda’s signal that a hike could come in December or January, former BOJ chief economist Seisaku Kameda told MNI, emphasising that the bank will need clearer data on wage growth before acting.

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none - BBG.

- Data/Event : Household Spending, Weekly Investment Flows

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

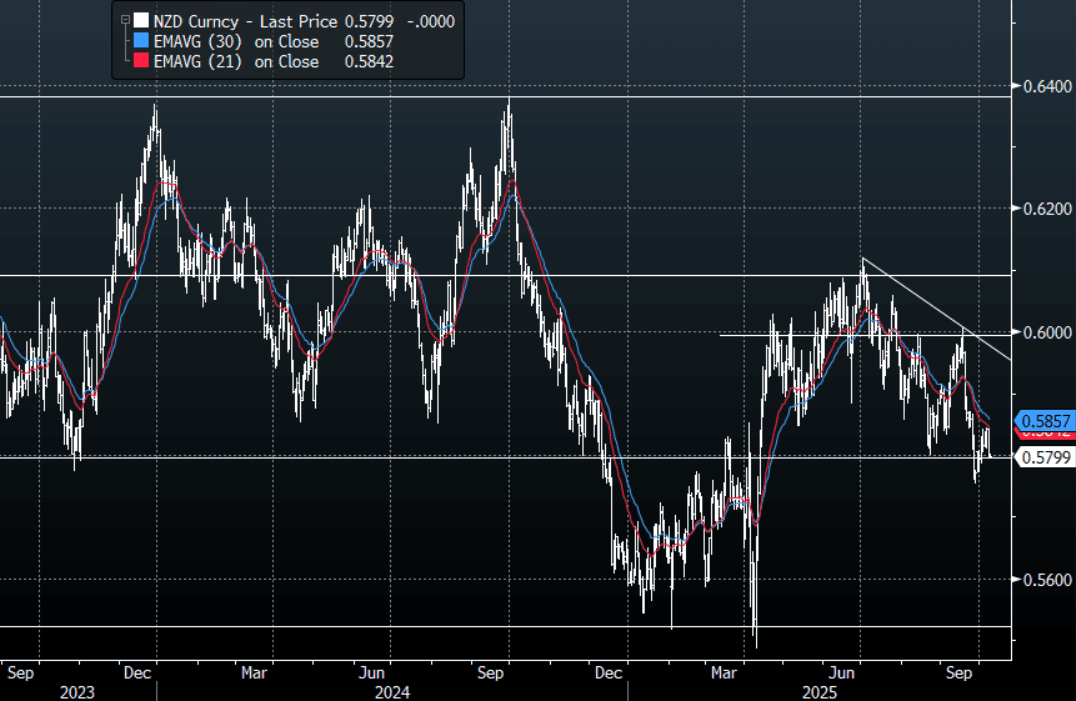

NZD: NZD/USD - Looking To Regain Momentum Below 0.5800, RBNZ Looms

The NZD/USD had a range overnight of 0.5794 - 0.5821, Asia is trading around 0.5800. US equities upward momentum looks to be stalling for now and the USD is building on its recent reprieve. The NZD topped out towards the 0.5850 area and has moved lower as the USD looks to correct. NZD/USD bears will be looking for the move below 0.5800 to regain momentum lower, the RBNZ today will have a say in whether they get their wish.

- MNI - RBNZ Preview: How Much To Ease? After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October. The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. 36bps of easing is priced for Wednesday’s meeting, with a cumulative 63bps by November 2025.

- Bloomberg - “Whole Milk Powder Average Price Falls to $3,696 a Ton. Average price for whole milk powder fell to $3,696 from $3,790 at the previous auction, according to the GlobalDairyTrade website. GDT's weighted average price for all milk products was $3,921 a ton. The GDT price index change, which is a weighted average of the percentage changes in individual milk products between trading events, was a decrease of 1.6%.”

- Data/Event: RBNZ

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

OIL: Modest Gains, Expected Surplus & Geopolitics The Focus

Crude made further modest gains on Tuesday as the post-OPEC relief rally continued but lost momentum. It will likely look for direction from the supply/demand outlook or geopolitical developments, especially related to Ukraine-Russia. The market is expected to shift into surplus towards the end of 2025 and this trend may begin to worry markets again now the OPEC November decision is behind it.

- WTI rose 0.6% to $62.03/bbl after falling to $60.72 but then recovering to $62.11. The benchmark is down 0.6% so far in October with the downtrend intact. Initial support is at $60.40 while resistance is $66.42.

- Brent is 0.5% higher at $65.79/bbl following a low of $64.53. It has traded in a relatively narrow $2.50 range this month. The bearish theme persists and this week’s gains are seen as corrective. Initial support is at $64 with resistance at $69.87.

- A soft outlook was reflected in the EIA’s October report as it is forecasting global oil inventories to build through next year pushing Brent down to $52/bbl from $62 in Q4 2025. Global output rises across its forecast horizon driven by non-OPEC. It doesn’t believe OPEC will be able to achieve its higher production targets helping to support prices.

- Bloomberg reported a US crude inventory build of 2.78mn barrels last week, according to people familiar with the API data. However, product stocks were lower with gasoline down 1.2mn and distillate 1.8mn. The official EIA data will still be released Wednesday as the agency is continuing to publish for now despite the US government shutdown.

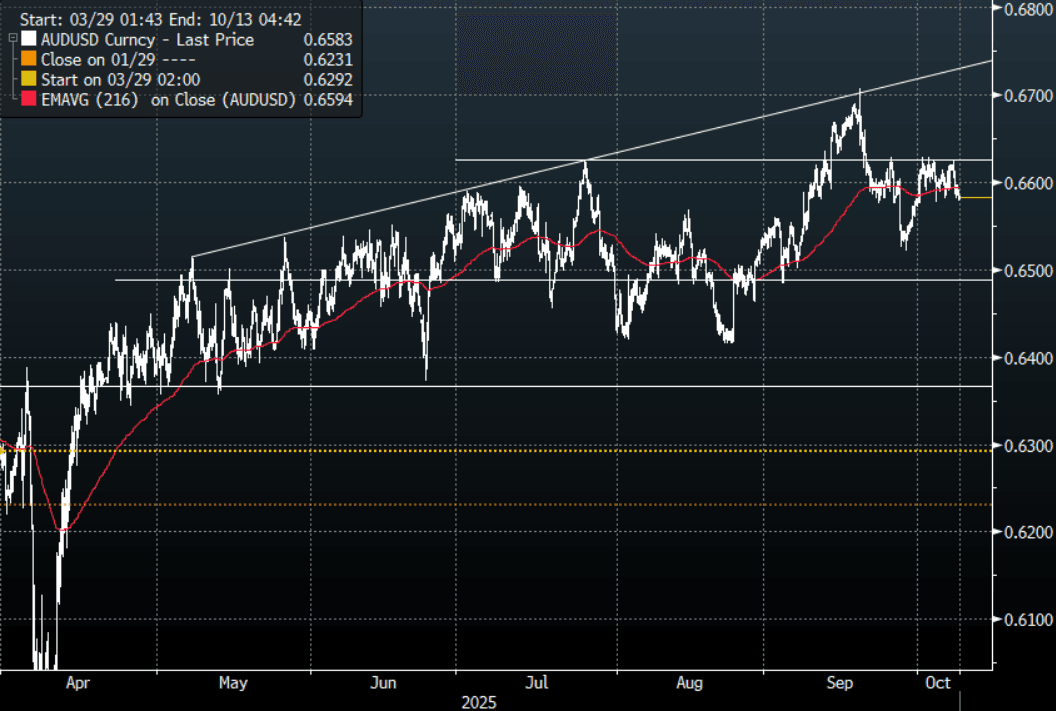

AUD: AUD/USD - Fails To Extend Above 0.6600, Drifts Lower As The USD Corrects

The AUD/USD had a range overnight of 0.6579-0.6602, Asia is trading around 0.6580. US equities upward momentum looks to be stalling for now and the USD is building on its recent reprieve. The AUD could not push above the 0.6625/50 resistance and has drifted lower from there in sympathy with the broader USD move and the risk backdrop looking a little toppy. This puts the AUD back in its recent range, and if the USD pullback continues to build the risk is skewed towards further losses, first support lies toward the 0.6475 area.

- Bloomberg - “Australia Home Rents Surge as Vacancy Sinks to Record Low. Australia’s home rental market tightened further in the third quarter, with the national vacancy rate sinking to a record low, in a setback for inflation prospects and hopes of near-term rate cuts. The Cotality Rental Value Index, which measures national dwelling rents, climbed 1.4% in the three months to the end of September, its largest quarterly gain since mid-2024. On an annual basis, rents jumped 4.3%.”

- “A Pentagon review of the AUKUS pact between the US, Australia and the UK is a “brass-tack” evaluation of its affordability and whether the agreement fits with President Donald Trump’s foreign-policy priorities, a Defense Department nominee said.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6300(AUD899m), 0.6725(AUD 398m). Upcoming Close Strikes : 0.6545(AUD607m Oct 10)- BBG

- Data/Event: Foreign Reserves

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P