JPY: USD/JPY Continues To Unwind Pre-Election Rally, Yield Differentials Lower

USD/JPY sit near 155.25/30 in latest dealings, around 0.40% stronger in yen terms for the session so far. Earlier lows were at 155.15. The market continues to fade upticks post the weekend election, with earlier highs today at 156.29. A case of the LDP victory priced into some degree, along with positive soundbites so far from Japan officials, has likely aided the move. The FinMin stating today there is no plans to extend the tax cut beyond two years and that a variety of options are being looked at to fund it (with focus on avoiding fresh JGB issuance).

- USD/JPY is back under the 20 and 50-day EMAs, but still above recent lows. 154.55/152.10 the low from Feb 2 and low from Jan 27 (and the bear trigger) are likely to be key downside focus points.

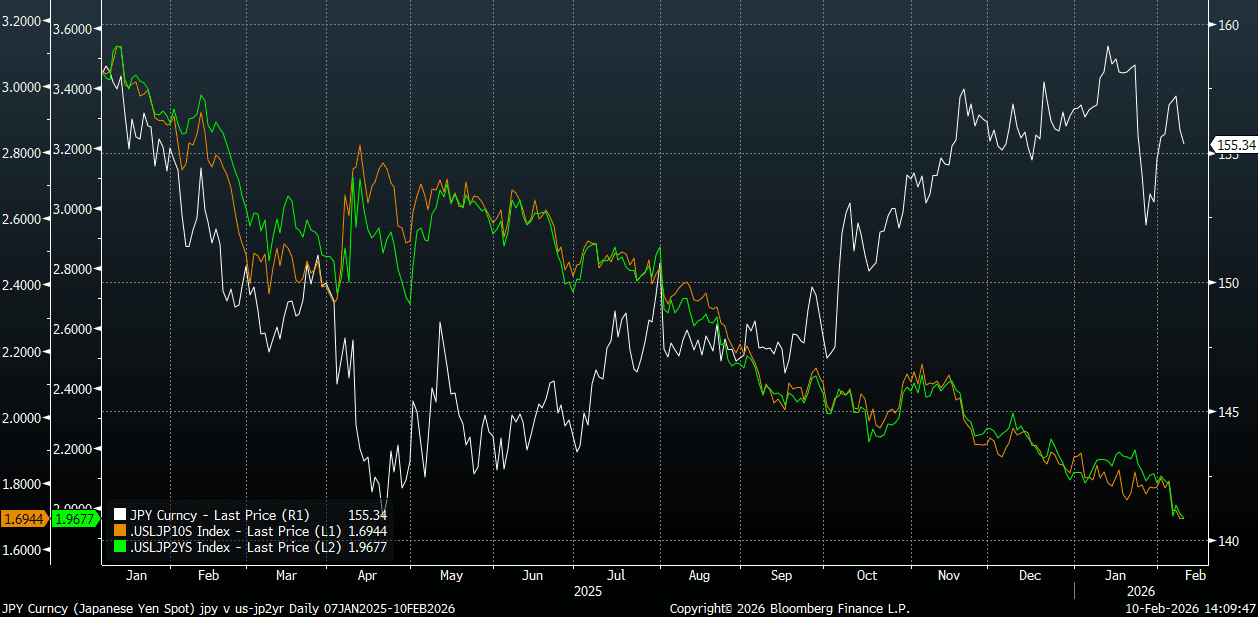

- If we can see concerns around the domestic policy outlook in Japan subside further, USD/JPY may realign itself more with yield differentials, which remain in a steep downtrend. The chart below plots USD/JPY versus the US-JP 2yr and 10-yr swap rate differentials.

- Helping sentiment for yen at the margins today has also been a softer precious metals backdrop, with gold and silver giving back some of the respective recent gains. AUD and NZD are both off around 0.20-0.25% at this stage. AUD/JPY is back under 110.00, but still above all key EMAs (the 20-day is near 108.11).

- Looking ahead, the local data calendar is empty tomorrow. We do have payrolls in the US tomorrow evening, a likely key driver of the near term rates outlook in the US.

Fig 1: USD/JPY Spot Versus US-JP Swap Rate Differentials

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Test Test TEST

MNI: MNI Test, Please Ignore

Test, ignore