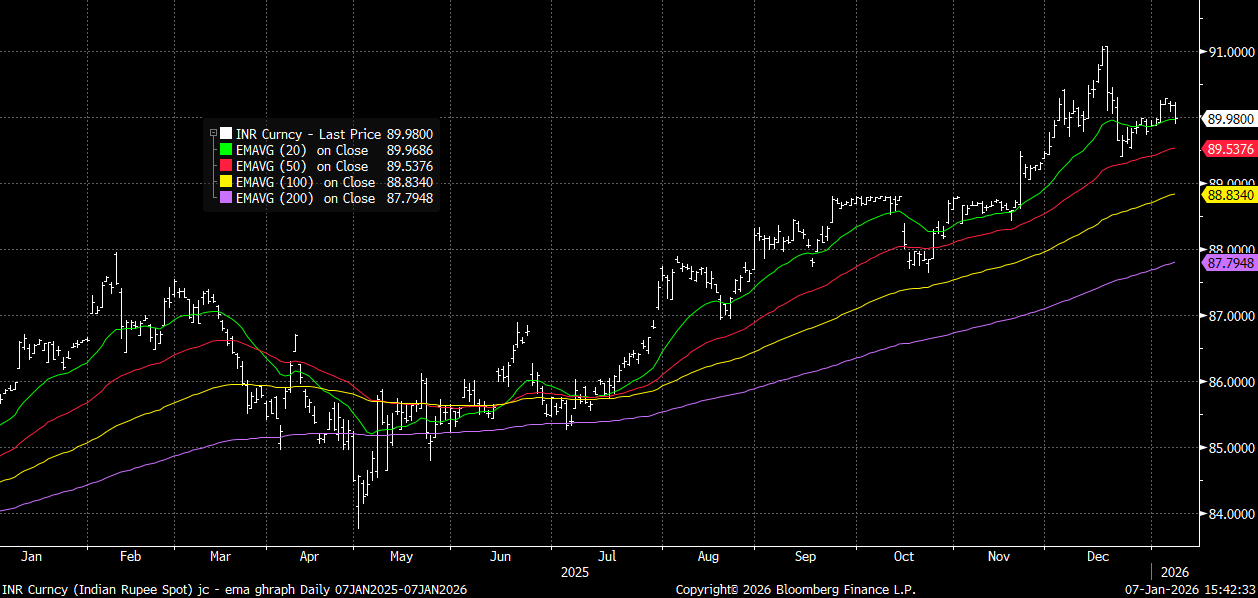

INR: USD/INR Under 90.00 On Fresh Intervention, Wedged Near Key EMA

Spot USD/INR is holding just under 90.00, weighed earlier by reported RBI intervention. Session lows were at 89.90. We are currently close to 20-day EMA support point. Recent highs rest at 90.29 from earlier in Jan. From mid Dec were saw the 91.00 level breached before falling sharply on more aggressive RBI intervention. Going back to August of last year, dips under the 20-day EMA support point have mostly proven to be buying opportunities. The one exception was in Oct when we fell under the 50-day EMA support, see the chart below.

- Broader risks are still skewed a buy on dips mentality from the market, particularly as we await for a trade deal to be confirmed by the US side. US President Trump noted overnight in terms of his relationship with Indian leader Modi, "“I have a very good relationship with him, but he is not that happy with me because they are paying a lot of tariffs,” Trump told a gathering of Republicans in Washington on Tuesday, adding that India’s buying of Russian oil “has reduced substantially.” (via BBG).

Fig 1: USD/INR Spot Versus Key EMAs

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBA: MNI RBA Preview-Dec 2025: On Hold, Could Be A Hawkish Shift?

- Download Full Report Here

- With October trimmed mean inflation printing at 3.3%, the RBA is unanimously expected to be on hold at its December meeting.

- The strength of the data since the November meeting plus inflation rising further above the top of the band increases the chance that the RBA now sees risks skewed to the upside and as a result it may sound more hawkish and at a minimum will remain “cautious”.

- RBA-dated OIS pricing is showing the probability of a 25bp hike rising from 2% tomorrow to 105% by August and 141% by December 2026.

- With core inflation rising over H2 2025 and stronger demand increasing upside risks, future rate decisions will be even more data dependent to give clarity to the outlook. November CPI is released 7 January & Q4/December 28 January ahead of the next RBA meeting on 4 February. At this stage policy is likely to be unchanged then too.

JGBS: Mostly Cheaper With 10YY A Fresh Cycle High ut A Subdued Session

JGB futures are slightly weaker, -3 compared to settlement levels, after a relatively subdued session.

- MNI Techs Team - Futures prices traded to new pullback and cycle lows again Friday, weighed by building expectations of a December BoJ rate hike and a breach of support in futures prices. This affirms the firm downtrend that's dominated prices since mid-September, and prices will need to challenge resistance before signalling any broader reversal. Key short-term resistance has been defined at 137.30, the Sep 8 high.

- MNI - Japan's Q3 GDP fell 0.6% q/q, or an annualised -2.3%, compared with the initial estimate of -0.4% q/q, or -1.8% annualised, as capital investment and public spending were revised down, although private consumption was revised slightly higher. Private consumption, which accounts for about 60% of Japan's GDP, was revised up to 0.2% from 0.1%, though its contribution remained unchanged at 0.1 pp.

- Cash US tsys are little changed in today's Asia-Pac session after Friday's modest sell-off.

- Cash JGBs are 2.5bps cheaper (20-year) to 0.5bp richer (40-year) across benchmarks, with the 10-year yield 1.0bp higher at 1.958%, a fresh cycle high.

- Swap rates are 1-3bps higher, with a steeper curve.

- Tomorrow, the local calendar will see Money Stock and Machine Tool Orders data alongside 5-year supply.

Source: Bloomberg Finance LP

US TSYS: Bonds Give Back Early Gains

US bond futures gave back earlier gains to be near where they started in the afternoon session. The US 10-Yr is flat at 112-17+ near to the 100-day EMA of 112-15. Topside resistance is the 50-day EMA of 112-26.

Cash has trended back to relatively unchanged across the curve having been lower in yields earlier.

- The 2-Yr is at 3.563%

- The 5-Yr is at 3.713%

- The 10-Yr is at 4.137%

- The 30-Yr is at 4.793%

There are no Tier 1 data releases tonight with markets looking ahead to the JOLTs Job Openings for October

Ahead tonight is a 13 and 26 week bill auction, with the focus being the U$58bn 3-Year auction.