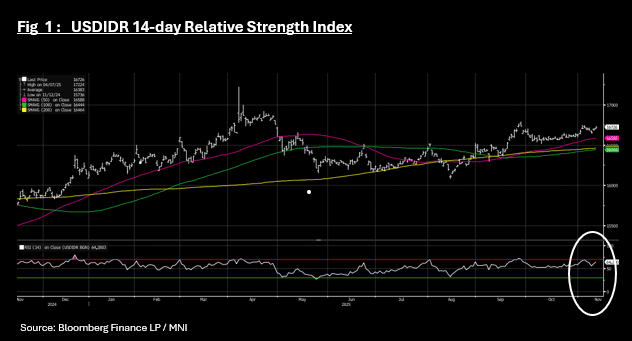

IDR: USDIDR Nears Over-Sold, Conditions for a Correction (amended)

Nov-12 04:13

- The plight of the Rupiah continues, losing ground again today by -0.20% to 16,728 .

- It is drawing near to the near term high of September at 16,749 and the 2025 high 16,891.

- USDIDR now approach oversold conditions according to the 14-day relative strength index with it seemingly a strong resistance point throughout the year.

- Despite a strong day for risk assets with the Jakarta Composite gaining +0.55% and bonds rallying, the currency continues to struggle.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Yields Up From Lows, But Bearish Bias Intact Given Data

Oct-13 04:10

NZGB yields have pared losses as Monday's session has unfolded, consistent with improved risk appetite amid higher US equity futures and lower US Tsy futures. We were last 2-4.5bps weaker, led by the backend. Near term focus will remain on US-China tensions, as markets look for an off ramp to higher US tariff level and export controls. Comments from US officials up to President Trump hint at an openness to negotiate. Still, for NZGBs the risks remain for lower levels in yield terms, so long as domestic growth remains soft, something reinforced by today's data.

- The 2yr was last at 2.60% (today's low near 2.55%), the 10yr at 4.08% (today's low was under 4.04%). The 2/10s curve is around +148, flatter versus recent highs of +154bps.

- The 2yr swap rate got to lows of 2.355%, but we sit back at 2.38% in latest dealings, off close to 2bps for the session. In yield terms the 2yr swap rate is oversold, but upticks, particularly back towards 2.50% may be used as fresh entry points to express lower yield risks. Longer term trends still look for move into the 2.00-2.25% region, without a broader shift in the macro backdrop.

- On the data front, the BNZ services and manufacturing PMIs for September were consistent with the RBNZ’s assessment in its October statement that “economic activity recovered modestly in the September quarter”. The manufacturing sector stagnated in August/September, while services continued to contract but at a slower rate with September. Continued weak activity, including employment, at the end of the quarter is consistent with further RBNZ easing with policy likely to become stimulatory.

ASIA STOCKS: As Trade War Intensifies, Equities Suffer (amended)

Oct-13 04:08

- With Japan out today, it was left to China's major bourses to guide sentiment as the trade war rhetoric ramps up. Having declined over -1.9% Friday, the CSI 300 started the week on the back foot, dragging the other key bourses with it. Down -1.7% today, it was the biggest two days of consecutive falls since April when the trade war began first ratcheted up. The Hang Seng fell sharply, down -3.3% as it traded through the key 20-day and 50-day EMA's and now is approaching the 100-day EMA which it last traded below in April. There was little positives to find as Shanghai Comp fell -1.30% and Shenzhen down -2.2%. The retail expansion of equity accounts over recent months has been a key contributor to the performance of stocks and comes on the back of a multi year decline in housing. The authorities will be loathe to see significant stock losses for investors and news agencies over the weekend were keen to spell out that the outlook for the CSI 300 should be little impact by the threats coming from Washington.

- Unsurprisingly the KOSPI followed China's lead and is down -1.6%. As always with market, context is key and the KPSPI hit new all time highs recently and any move lower is as much driven by the locking in of profits by investors, rather than a sea change in sentiment at this stage.

- With the JCI doing very little, South East Asia's other major bourse the FTSE Malay KLCI is down just over -0.50%. It has consistently underperformed the run up in equities in the recent period of strength and naturally its downside seems less pronounced.

- The focus on China arguably gives India a short respite having been in the sights of the US recently. The NIFTY 50 delivered a positive though modest week of gains last week, yet is giving some of those gains back in Monday morning trade.

ASIA STOCKS: As Trade War Intesifies, Equities Suffer

Oct-13 04:07

- With Japan out today, it was left to China's major bourses to guide sentiment as the trade war rhetoric ramps up. Having declined over -1.9% Friday, the CSI 300 started the week on the back foot, dragging the other key bourses with it. Down -1.7% today, it was the biggest two days of consecutive falls since April when the trade war began first ratcheted up. The Hang Seng fell sharply, down -3.3% as it traded through the key 20-day and 50-day EMA's and now is approaching the 100-day EMA which it last traded below in April. There was little positives to find as Shanghai Comp fell -1.30% and Shenzhen down -2.2%. The retail expansion of equity accounts over recent months has been a key contributor to the performance of stocks and comes on the back of a multi year decline in housing. The authorities will be loathe to see significant stock losses for investors and news agencies over the weekend were keen to spell out that the outlook for the CSI 300 should be little impact by the threats coming from Washington.

- Unsurprisingly the KOSPI followed China's lead and is down -1.6%. As always with market, context is key and the KPSPI hit new all time highs recently and any move lower is as much driven by the locking in of profits by investors, rather than a sea change in sentiment at this stage.

- With the JCI doing very little, South East Asia's other major bourse the FTSE Malay KLCI is down just over -0.50%. It has consistently underperformed the run up in equities in the recent period of strength and naturally its downside seems less pronounced.

- The focus on China arguably gives India a short respite having been in the sights of the US recently. The NIFTY 50 delivered a positive though modest week of gains last week, yet is giving some of those gains back in Monday morning trade.