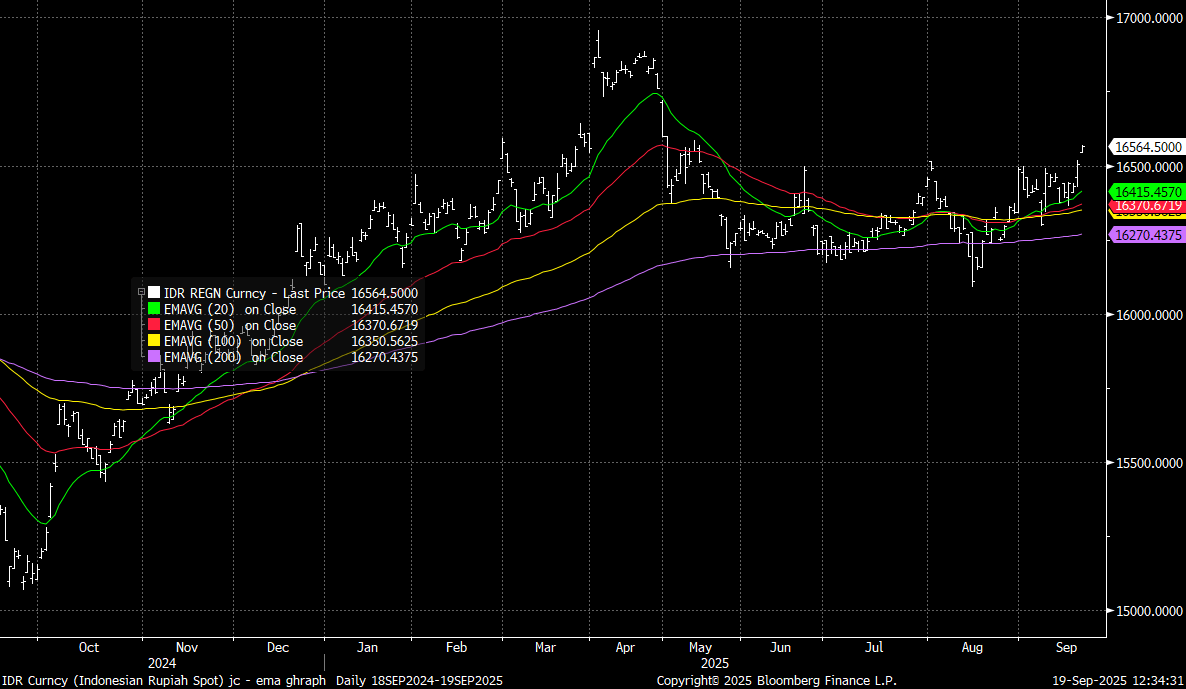

IDR: USD/IDR Consolidates Break Above 16500

USD/IDR spot is higher in the first part of Friday dealings, last at 16565 (+0.35% up on end Thursday levels). This is largely catch up to USD gains from Thursday trade, as better US data outcomes aided higher US yields. The teal US 10yr yield moved back up to +1.73%. So far today, the 1 month NDF is little changed and close to 16600.

- Still, this is fresh highs for spot in back to mid May (which were at 16585). The 16600 level beckons next, while April highs in the pair were close to 17000, see the chart below. At this stage, official jawboning/and or intervention around FX doesn't appear to have materialized from BI.

- Focus will remain on the fiscal backdrop, yesterday's news of widening the budget deficit to 2.68% for next year was beyond the initial 2.48% estimate, but short of the 3% deficit ceiling. Via BBG: “The higher deficit does not bode well for sentiment but impact is likely to be limited given that its remains below 3% limit and overall lower than the 2.78% projected deficit for 2025,” said Wee Khoon Chong, APAC market strategist at BNY Mellon in Hong Kong."

- 5yr CDS for Indonesia is up slightly, but at +70bps, remains within recent ranges.

Fig 1: Spot USD/IDR Versus Key EMAs.

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBs: Gap Richer After RBNZ Gives Dovish Guidance

NZGBs gap 9-12bps richer after the RBNZ cut the OCR by 25bps to 3.0%, as expected (4–2 vote; some favoured a 50bp cut).

- Forward guidance sees the OCR averaging 2.71% in 4Q 2025, 2.56% in 2Q 2026, and 2.59% in 3Q 2026 (down from May’s trough forecast of 2.9%). Indicates scope for further rate cuts if inflation pressures ease; forecasts imply a good chance of two more 25bp cuts.

- GDP seen contracting 0.3% q/q in 2Q 2025 but growing 0.3% q/q in 3Q 2025. Risks to the outlook remain both to the upside and downside.

- Bottom line: RBNZ delivered a widely expected rate cut to 3%, signalled a lower future OCR path, and left the door open for further easing if inflation moderates. Markets responded with a weaker NZD and higher local equities.

- Swap rates are 9-12bps lower after the decision.

- RBNZ dated OIS pricing has shunted softer for meetings beyond August. Pricing is 14-18bps softer out to July 2026. 31bps of cumulative easing is priced by November 2025.

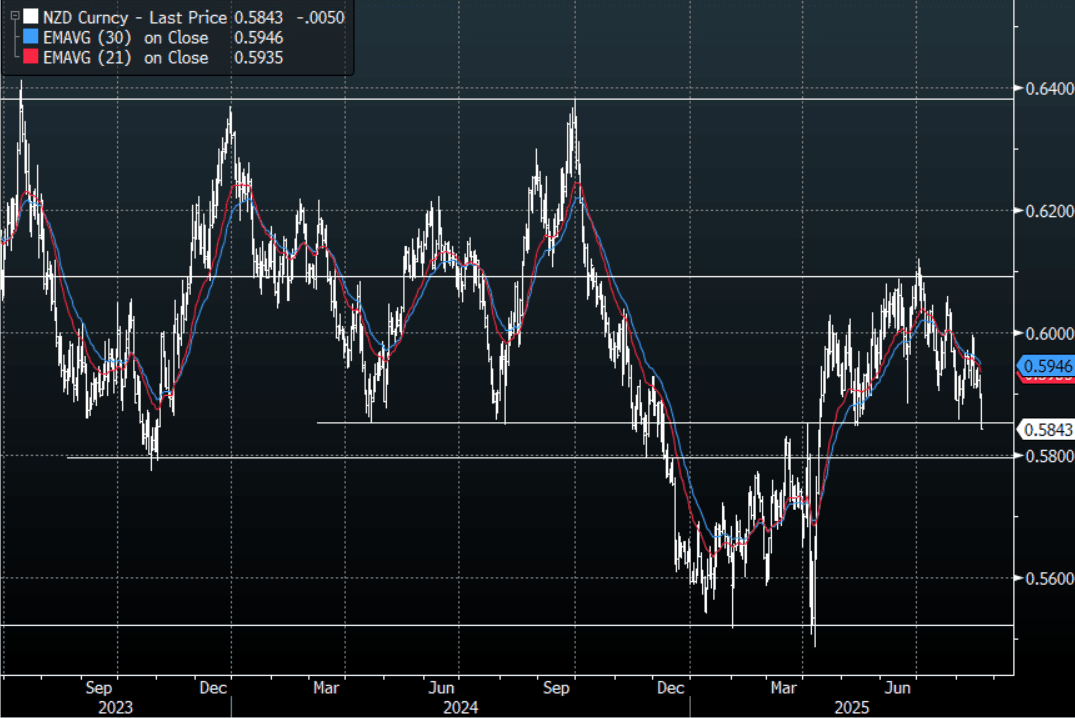

NZD: NZD/USD - Probing Pivotal Support After The RBNZ

With policy makers signaling there is scope to lower borrowing costs further if inflation pressure ease the NZD/USD has quickly moved lower and is now testing some pivotal support. Is this enough for the NZD to break lower and reignite the momentum lower ? Together with a market that is paring back USD shorts into Jackson Hole it does leave the NZD vulnerable.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

RBNZ SEES LOWER OCR SHOULD INFLATION EASE FURTHER

- RBNZ SEES LOWER OCR SHOULD INFLATION EASE FURTHER

- RBNZ DISCUSSED 50BP CUT, ALONGSIDE HOLD AND 25BP REDUCTION