IDR: USD/IDR Back Under 16400, Cross Asset Trends Help, BI Seen On Hold

Spot USD/IDR is tracking near 16390 in latest dealings, down a little over 0.40% for the session so far. This brings us back close to the 20-day EMA support point, but greater focus is likely to rest around the 200-day EMA support zone (16261 (which we haven't been able to sustain moves under so far in 2025). On the topside, as we noted yesterday, firm official resistance is still likely on any move towards 16500 or just above this level.

- Cross asset moves are likely helping IDR sentiment. The continued move lower in US real yields is a positive, although USD/IDR remains quite elevated relative to such trends.

- Local equities continue to recover as well, the JCI last up +1.2%. We remain sub recent highs and while offshore flows remain negative, the pace of selling has moderated from earlier in the week (when market sentiment was jittery on the FinMin replacement).

- New FinMin Purbaya Yudhi Sadewa announced late yesterday a review of the 2026 budget. He wouldn't be drawn on whether the deficit as a share of GDP would shift. Via BBG: "When asked whether a review would include a change in the deficit target, Purbaya told reporters that it “may be changed, may be not. Can be higher, can be lower, we’ll see later.”

- This will remain a focus point for markets. Next week we have the BI decision, with no changed expected by the economic consensus. Per the BBG survey, 9 economists surveyed so far see a steady 5.00% policy rate outcome.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

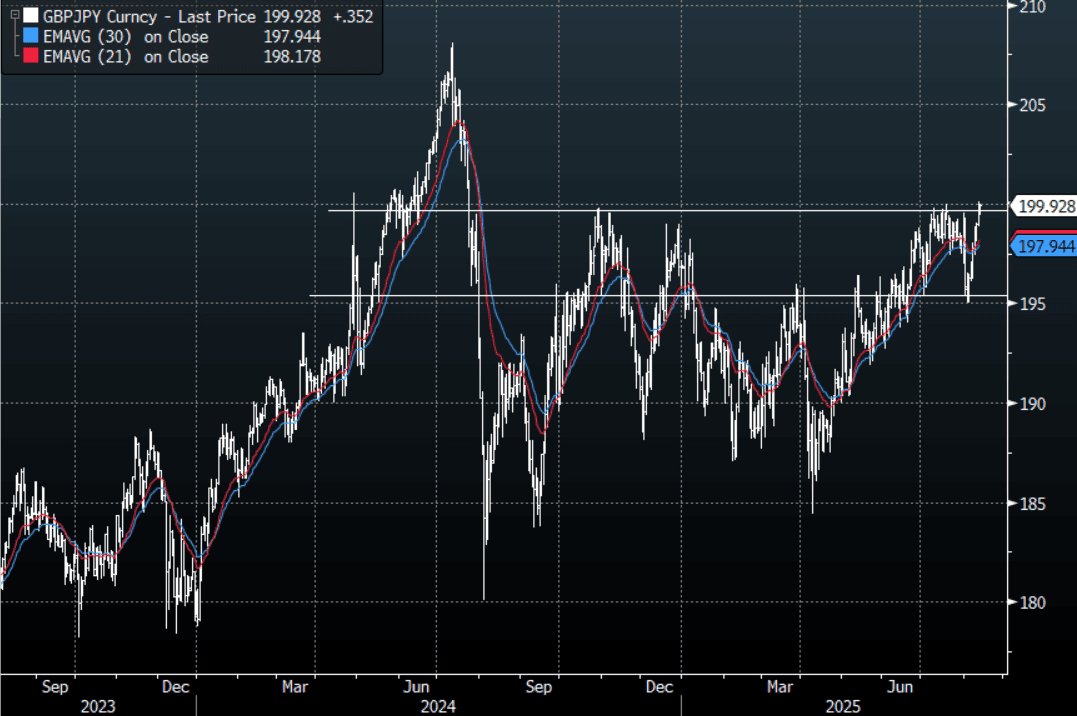

FOREX: JPY Crosses - Push Higher As US Stocks Makes New Highs, GBP/JPY Tests 200

US Equities stormed to new all-time highs in the N/Y session as the market gears up for a potential series of rate cuts. This morning US futures have opened pretty muted albeit still at their highs, ESU5 -0.04%, NQU5 +0.03% The JPY crosses remain better bid as risk extends higher, GBP/JPY leads the move eyeing a test of 200.00.

- EUR/JPY - Overnight range 172.08 - 172.86, Asia is trading around 173.00. This pair bounced off its support just below 170.00 and has put a base in now around 170.00. While risk continues to trade positive this will remain bid now on dips.

- GBP/JPY - Overnight 198.13 - 200.08, Asia trades around 199.90. Risk has broken higher again overnight and there has been no sign of a pullback which has seen the pair blow through what should have been decent resistance. A move back above 200.00 could generate fresh impetus higher and dips back towards 198.50 should now find support first up.

- NZD/JPY - Overnight range 87.80 - 88.18, Asia is currently dealing 88.20. The pair found solid demand towards the 86.50 area, I felt sellers should remerge on a bounce back towards 88.50 first up but the price action in the other JPY crosses would make you question a fade for now. A sustained move back above 89.00 would reinstate the momentum higher.

- CNH/JPY - Overnight range 20.5518 - 20.6465, Asia is currently trading around 20.6100. This pair found solid demand back towards its first support area around 2.4000. A sustained break back below 2.3000 is needed to turn momentum lower again, until then dips will probably continue to be supported.

Fig 1 : GBP/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Slightly Richer After Today's Q2 Wages Data

ACGBs (YM +1.5 & XM +0.5) are slightly stronger after today’s wages data.

- The Q2 WPI rose 0.8% q/q leaving annual inflation at 3.4% y/y after a recent trough at 3.2% in Q4 2024 and 4.1% in Q2 2024. Public sector quarterly wage gains outpaced the private sector for the third consecutive quarter at 1.0% q/q compared with 0.8%. Public wage growth is now up 0.1pp to 3.7% y/y, while private was 3.4% y/y. The RBA had forecast 3.3% for Q2 and in its August projections is expecting the WPI to trend lower to around 3% by Q2 2026. 2025 to date is showing some stabilisation in wage inflation.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session.

- Cash ACGBs are flat to 2bps richer with a steeper 3/10 curve and the AU-US 10-year yield differential at -5bps.

- Expectations of sustained strong pricing at auctions proved accurate, with the latest round of ACGB Dec-35 supply seeing the weighted average yield print 0.22bp through prevailing mids. Moreover, today’s cover ratio rose to 3.2417x from 2.6500x.

- The bills strip is +1 to +3.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in September is given a 41% probability, with a cumulative 40bps of easing priced by year-end.

JGBS AUCTION: Poll: 5-Year JGB Auction

*JAPAN 5Y GOVT BOND AUCTION MAY HAVE 99.72 LOWEST PRICE:POLL – BLOOMBERG