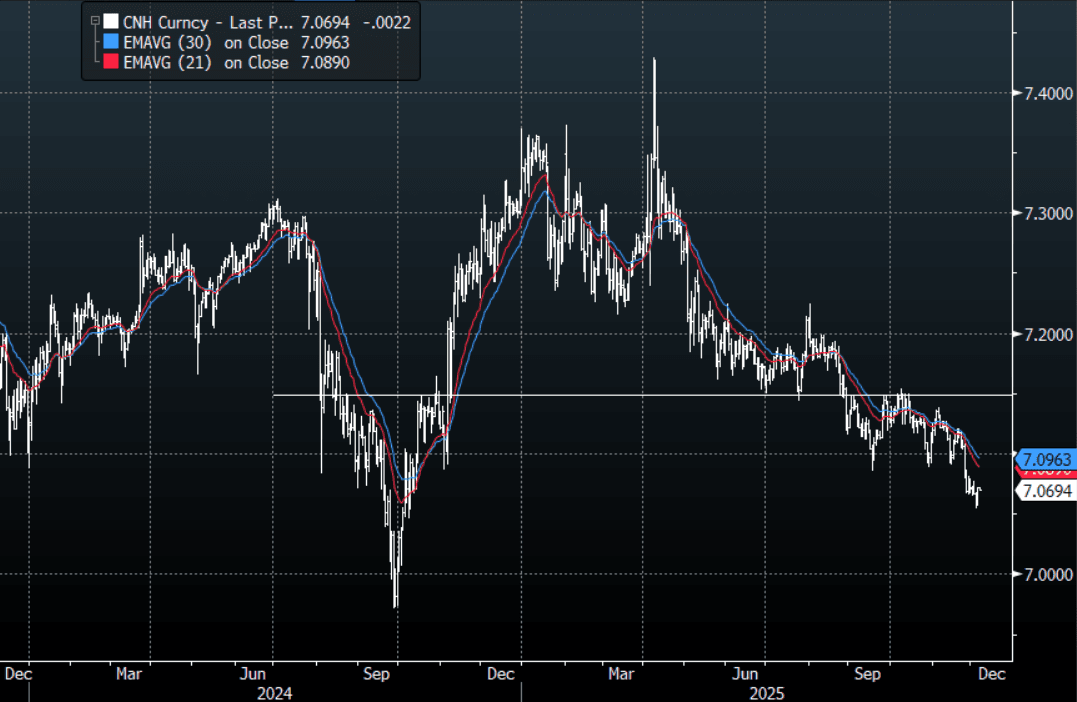

CNH: USD/CNH - The Fix Will Be Watched For More Signs Of PBOC Pushback

The overnight range was 7.0613 - 7.0717, Asia is currently trading around 7.0700. The pair pulled back yesterday as the PBOC pushed back on the relentless USD selling. The pair still looks to be under pressure and the PBOC has a job on its hands to turn this around. The Fix will be closely watched this morning for more signs of a pushback. On the day it feels like we could pullback further in the short-term but I suspect sellers will be lining up again on a bounce back towards the 7.0900-7.1200 area if they see it.

- MNI BRIEF: PBOC To Control Pace To Prevent Side Effects: The People's Bank of China will calibrate the intensity and pace of its policy to avoid excessive moves from reducing policy effectiveness and causing long-term side effects, while taking measures to smooth out economic fluctuations, Governor Pan Gongsheng said in an article in People's Daily on Thursday.

- MNI BRIEF: China New Housing Supply Down 19% Y/Y In 2025. China’s 28 major cities are expected to add 5.68 million square meters of new commercial housing supply in December, a 12% decline from the previous month, with full-year 2025 supply projected to fall 19% from a year earlier, according to a report released Thursday by research firm CRIC.

- The USD/CNH Average True Range for the last 10 Trading days: 118 Points

Fig 1 : USD/CNH Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Market Unwinds Post-RBA Sell-Off

ACGBs (YM +3.5 & XM +2.5) are stronger after cash US tsys finished with modest gains ahead of today’s non-government produced economic data: ADP employment, S&P Global US Services/Composite PMI and ISM Services, as well as the US Tsy Quarterly Refunding announcement.

- MNI RBA WATCH: Bullock Strikes Cautious Tone Following Pause. The Reserve Bank of Australia may not need to ease as much as its peers, Governor Michele Bullock said on Tuesday after the Board unanimously decided to hold the cash rate at 3.6%.

- Bullock said the economy had probably retained more demand than previously expected, which continued to drive inflation, particularly in market services and new-dwelling costs. Monetary policy remains tight despite mixed signals on financial conditions, she reiterated.

- Cash ACGBs are 3-4bps richer with the AU-US 10-year yield differential at +24bps.

- The bills strip has bull-flattened across contracts, with pricing +1 to +4.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 12% probability, with a cumulative 10bps of easing priced by February 2026.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond today and A$800mn of the 3.00% 21 November 2033 bond on Friday.

- Today, the local calendar will see S&P Global Composite & Services PMIs.

US TSYS: Yields Grind Lower; TYZ5 Approaches Key Technical

- Treasuries look to finish modestly higher Tuesday - after a narrow range as markets await Wednesday's non-government produced economic data: ADP employment, S&P Global US Services/Composite PMI and ISM Services, the US Tsy Quarterly Refunding announcement and equity markets down on profit taking. TYZ5 finished up at 112-25+ (+03+) as it approaches the 50-day EMA

Cash was strong across the curve, taking back most of the prior day's losses, with yield 2-3bps lower.

- The 2-Yr is at 3.576% (-3.1bps lower)

- The 5-Yr is at 3.694% - lower by -2.9bps

- The 10-Yr is down -2.7bps to 4.085%

- The 30-Yr is lower by -2.6bps to 4.667%

Projected rate cut pricing gains slightly vs. late Monday levels (*): Dec'25 at -17.2bp (-16.4bp), Jan'26 at -26.4bp (-24.6bp), Mar'26 at -34.9bp (-32.9bp), Apr'26 at -41.4bp (-39.1bp).

The ISM Services survey for October (Wednesday, 1000 ET) is expected to see a modest uptick in the headline PMI index to 50.8 (50.0 prior), with the Employment sub-gauge steady at 47.3 (47.2 prior). The latter will be particularly closely watched in a week that will see the October nonfarm payrolls release postponed indefinitely due to the government shutdown.

Analysts' outlooks for Wednesday's refunding reflect almost no expectations for any major changes, but there is increasing attention being paid to the likelihood of increased bill issuance ahead as coupon sizes aren't increased until well into 2026 at least.

BONDS: NZGBS: Richer After UE Rate Holds Steady At 5.3%, 2Y Rate Rejects 20D-EMA

NZGBs are slightly richer, with yields 1-2bps lower, after the release of Q3 labour market and wages data.

- NZ’s jobless rate held steady at 5.3% in the third quarter, matching economist expectations. Employment was unchanged quarter-on-quarter, compared with a revised 0.2% fall in the previous quarter, while employment declined 0.6% year-on-year, a smaller drop than in the second quarter. The labour force participation rate was 70.3%.

- Average hourly earnings rose 0.7% from the previous quarter, and non-government wages increased 0.4% including overtime and 0.5% for ordinary time.

- Overnight, US tsys finished moderately richer across benchmarks with the markets awaiting Wednesday's non-government produced economic data: ADP employment, S&P Global US Services/Composite PMI and ISM Services, as well as, the US Tsy Quarterly Refunding announcement.

- Swap rates are 2-3bps lower, with the 2-year rate rejecting off the 20-day EMA.

- RBNZ dated OIS pricing is slightly softer across meetings. 26bps of easing is priced for November, with a cumulative 33bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP