CNH: USD/CNH Sub key EMAs, US Lawmakers Visit China, LPRs Seen Steady

USD/CNH tracks near 7.1150 in early Monday dealings, which is slightly off end Friday levels from NY last week (closer to 7.1200). Broader USD sentiment continued to recovery on Friday, the BBDXY index up a further 0.22%, while the DXY gained 0.30%. Still, both indices were little changed for whole of last week. Spot USD/CNY finished up at 7.1182, while the CNY CFETS basket tracker rose a further 0.17% to 96.36 on Friday. This index remains within recent ranges.

- On the Xi-Trump call on Friday: "“The call was a very good one, we will be speaking again by phone, appreciate the TikTok approval, and both look forward to meeting at APEC!” Trump added." (via BBG). The deal on Tiktok (final steps etc) still reportedly has to be signed off on though.

- Also note that senior US lawmakers arrived in China on Sunday for talks with senior China government officials (the first such trip in six years). They met with China Premier Li Qiang. This trip is aimed at improving ties and strengthening the US-China relationship.

- For USD/CNH, we remain sub key resistance points, with the 20-day EMA near 7.1275, while the 50-day is holding just above 7.1505. Downside focus is likely to rest with recent lows at 7.0851.

- US-CH yield differentials stabilized post the Fed last week, the 2yr spread near +213bps, the 10yr spread at +233bps. China equity outperformance also cooled, likely tempering CNH gains.

- Today on the data front we have the 1yr and 5yr Loan prime rates. Not change is expected in either rate.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: NatWest Now Sees Cuts In 2025, Starting In September

As with Deutsche earlier, NatWest has changed its Fed call after the Powell Jackson Hole speech to reflect a 25bp September cut. Previously, the call was for no cuts in 2025. The new baseline outlook includes further 25bp cuts in December and March, bringing rates closer to neutral ("however, the changing composition of the committee becomes far less clear once Powell term expires in May").

- "While the August jobs and CPI reports will be watched carefully, it is clear to us that Powell has already seen enough to decide renewed action to counter downside economic risks is likely warranted, and so we now look for a 25 basis point rate cut on September 17th.

- "We expect officials will very much downplay the likelihood of a 50bp rate cut leading up to the jobs data, but we have to admit if the report is "weak enough" (e.g., the unemployment rate increases by 0.3pct to 4.5% (where officials had it at year end) anything can happen and wouldn't rule anything out. However, given the latest pivot and with financial markets pricing (86% of a 25bp rate cut) a lot has to happen (unemployment rate 3-handle and core CPI +0.5%) for the FOMC to undeliver and hold off from a rate cut in September. "

USDCAD TECHS: Bull Cycle Hindered

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3968 High May 20

- RES 1: 1.3925 High Aug 22

- PRICE: 1.3840 @ 16:55 BST Aug 22

- SUP 1: 1.3794 20-day EMA

- SUP 2: 1.3769/22 50-day EMA / Low Aug 22

- SUP 3: 1.3576 Low Jul 23

- SUP 4: 1.3557/40 Low Jul 3 / Low Jun 16 and the bear trigger

Gains this week in USDCAD and the breach of resistance at 1.3879, the Aug 1 high, marked a positive development, however the slippage into the Friday close undermines this sentiment - for now. Moving average studies have crossed and are in a bull-mode position, reinforcing current conditions. An extension higher would signal scope for a climb towards 1.4019, a Fibonacci retracement. On the downside, support to watch lies at 1.3769, the 50-day EMA - a level not yet challenged by the correction lower.

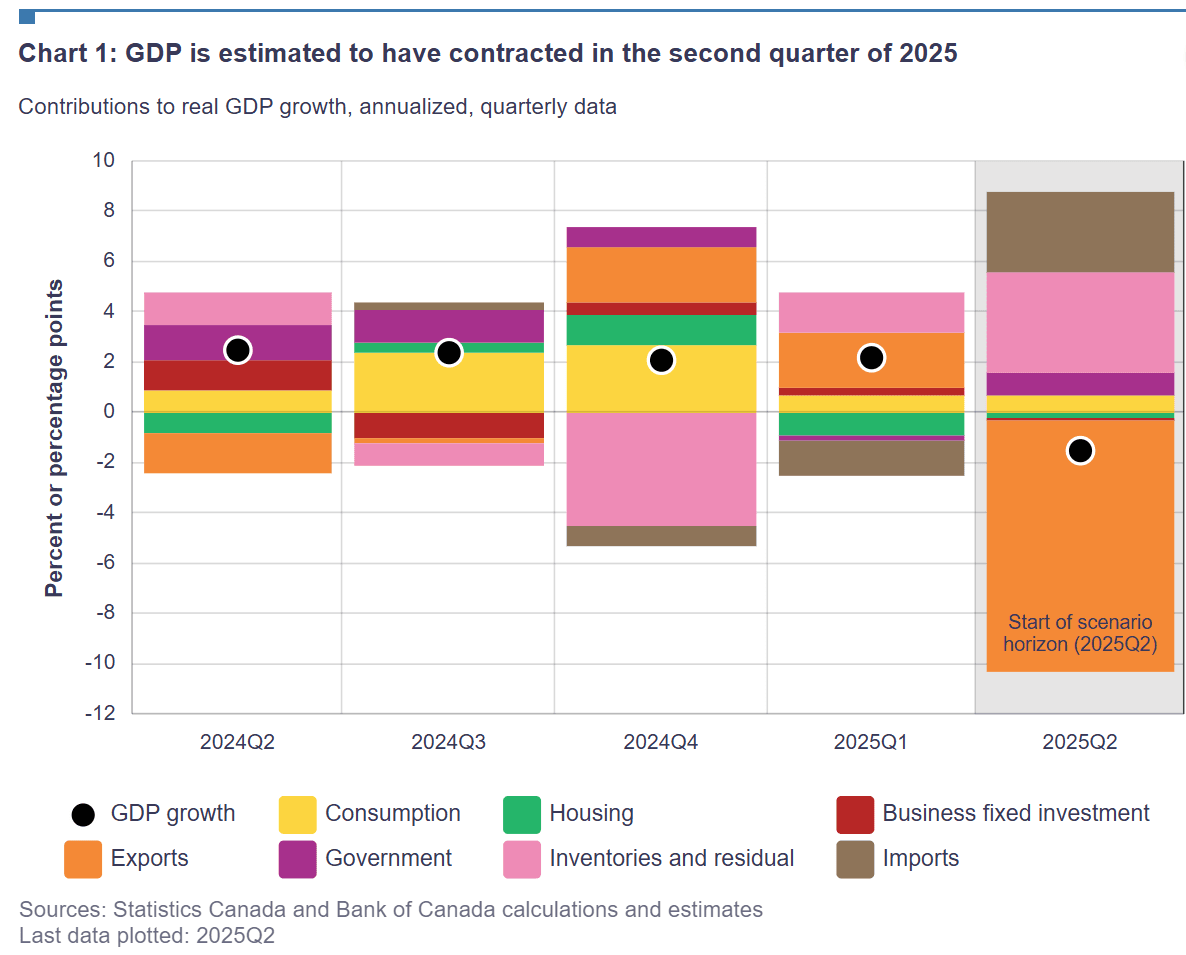

CANADA: Q2 Expected To See GDP Contraction, BOC's Estimate Looks Too Negative

The June retail sales release helps wrap up the last major data before Canadian Q2 GDP is released on Friday August 29.

- Current Bloomberg analyst consensus shows Q2 is expected to show a 0.7% Q/Q annualized contraction, versus +2.2% in Q1. The private sector consensus is more optimistic than the Bank of Canada's -1.5% estimate in its July Monetary Policy Report (which MNI thinks is too low) but the component-by-component breakdown is similar if of differing magnitudes.

- Widely expected are: a softening in household consumption growth (+1.2% in Q1), with a pickup in government spending, continued weakness in fixed investment (-3.0% in Q1) though with residential outperforming business capital formation, and a reversal of Q2's positive contribution from net exports. In short, the data are expected to confirm that trade activity was brought forward to Q1 ahead of tariffs, with the effects reversing in Q2.

- Going forward, the BOC envisages growth resuming in Q3 (+1.0% in its "current tariff" scenario). In the meantime, a weak Q2 reading could provide Governing Council with more conviction to resume easing rates in September, with the July meeting decision noting "If a weakening economy puts further downward pressure on inflation and the upward price pressures from the trade disruptions are contained, there may be a need for a reduction in the policy interest rate".