ASIA FX: USD/CNH Remains Close To Cycle Lows, KRW Continues To Underperform

In North East Asia FX, market moves have been fairly modest in Friday trade to date. USD/CNH has edged up a touch, but at 7.0525 remains close to recent year to date lows (7.0480). The China Central Economic Work Conference didn't produce a lot of surprises, with the main take aways being a steady but supportive backdrop from a policy standpoint. CNH is outperforming broader cross asset trends in terms of US-CH yield differentials and China to global equity ratios. Still, this time of year is seasonally supportive of the yuan and continues into the new calendar year (ahead of China's new year). USD/CNH remains under spot USD/CNY as a further sign the market is looking for further CNH gains. A clean break under 7.0500 is likely to see 7.00 targeted.

- Spot USD/KRW is holding above 1470 for now, a notable laggard in terms of broader USD softness seen in recent sessions (along with CNH and JPY gains). Focus remains on whether we will see greater USD supply, particularly ahead of year ahead (when lighter liquidity may bring about sharper moves). The 20-days EMA support point is around 1466.5.

- Spot USD/TWD is back lower, but at 31.20/25 remains comfortably within recent ranges. Local equities are higher today, the Taiex back above the 28k level.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOJ: Rinban Purchase Offer

The BoJ offers to buy a total of Y720bn of JGBs from the market:

- Y300bn worth of JGBs with 1-3 Years until maturity

- Y305bn worth of JGBs with 5-10 Years until maturity

- Y115bn worth of JGBs with 10-25 Years until maturity

OIL: Crude Holds Most Of Tuesday’s Gains Ahead Of Key Reports

After rising around 1.5% on Tuesday, crude is slightly lower on Wednesday as the market waits for key information released later. WTI is down 0.3% to $60.84, holding above $60 through the session, while Brent is 0.3% lower at $64.99 after falling to $64.90. The USD index is up 0.1%.

- The excess oil supply driven by increased OPEC and non-OPEC output remains in focus with the spread between the WTI December-January contracts only 4c, suggesting an expected easier market. The EIA short-term outlook, IEA annual report and OPEC monthly report are published Wednesday. As well as US industry-reported inventory data.

- While expected excess supply has pressured oil prices, the market remains unsure over the impact of the latest sanctions on Russia. There has already been an increase in diesel prices and signs that India is looking for sources that are not Lukoil or Rosneft. Also, Russia’s Lukoil’s West Qurna 2 field in Iraq has been transferred to state firms to ensure production continues, according to Bloomberg.

- Our US analysts believe that the post-shutdown data schedule should be published next week with a risk that October CPI won’t be released. See their FAQ here.

- Later the Fed’s Barr, Williams, Paulson, Waller, Bostic, Miran and Collins speak as well as the ECB’s Schnabel and de Guindos. The Eurogroup meeting is taking place. There are no data of note.

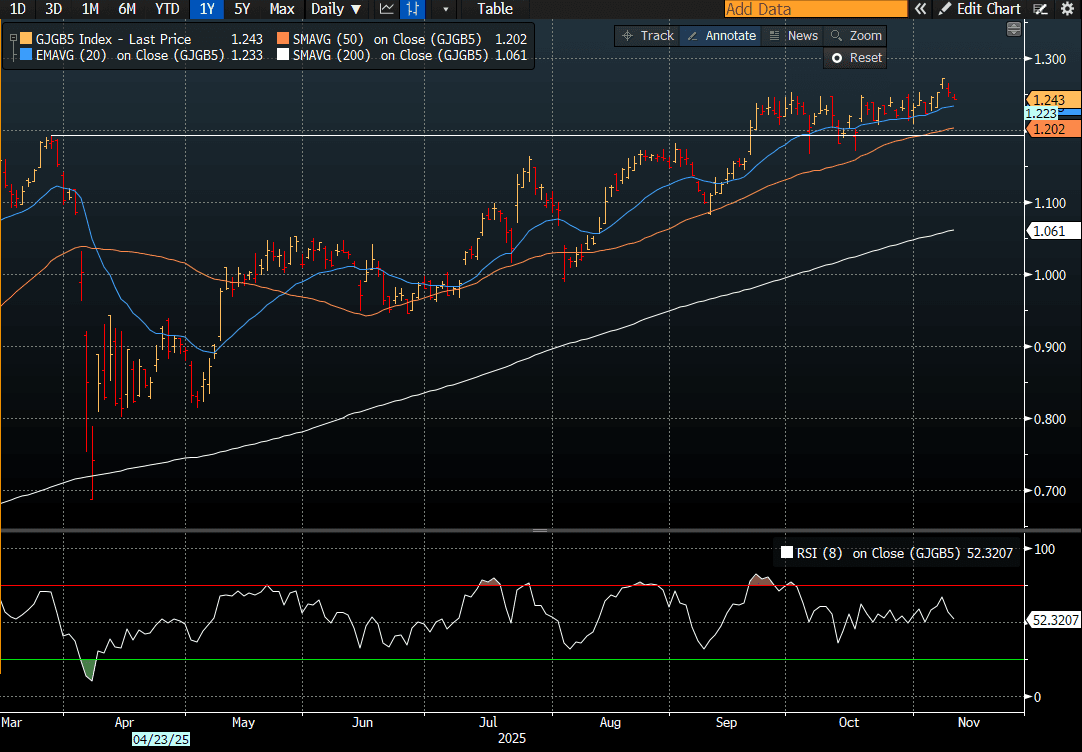

JGBS: 5Y Richer Ahead Of Tomorrow's Supply, Long-End Cheaper

JGB futures are stronger and at session highs, +14 compared to settlement levels, on a data-light day.

- Cash US tsys are 2-4bps richer in today's Asia-Pac session after being closed yesterday for Veterans Day.

- Cash JGBs are 1.5bps richer (7-year) to 1.5bps cheaper (20- and 40-year) across benchmarks. The benchmark 5-year yield is 0.9bp at 1.243% versus the cycle high of 1.272% (see chart).

- Ahead of tomorrow's 5-year supply, the 2s/5s curve has steepened to near its cycle high of 32bps, last reached in late 2023.

- Regression analysis shows a strong pro-cyclical, but atypical, relationship between the 5-year yield and the 2s/5s curve over the past 12 months.

- This dynamic is supported by expectations that the 5-year sector will sit in the "sweet spot" for increased issuance, as Prime Minister Sanae Takaichi looks to deploy her first stimulus package to jump-start the economy.

- Swap rates are 1bp lower to 1bp higher, with a steepening bias.

- Tomorrow, the local calendar will see PPI and International Investment Flow data alongside 5-year supply.

Source: Bloomberg Finance LP