CNH: USD/CNH Makes Fresh Lows, But Jan Gains Slower Versus Dec

Spot USD/CNH tracks near 6.9630 in early Friday dealings, just up from intra-session lows on Thursda...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Slightly Richer With US Tsys After US Data Dump, Oct-36 Supply

ACGBs (YM +0.5 & XM +1.0) are slightly stronger after cash US tsys finished moderately richer, but off post data bests. Focus turned away from the 4.6% unemployment rate with possible assistance from that heavy -105k in Oct NFP.

- Bloomberg reports, "Australia Expects Slightly Narrower Budget Deficits Through 2029. Australia government expects slightly narrower budget deficits across the forecast horizon, Wednesday's mid-year update will show, as it tightens the reins on spending and rolls out new savings measures. The government said it has found A$20 billion in savings in the MYEFO and will keep average real spending growth to 1.7% over the seven years to 2028-29, or almost half the 30-year average of 3.3%."

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +57bps.

- The bills strip is flat to -2 across contracts, with a flattening bias.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for February to 102% by June and 155% by December 2026.

- Today, the local calendar will see Westpac Leading Index data.

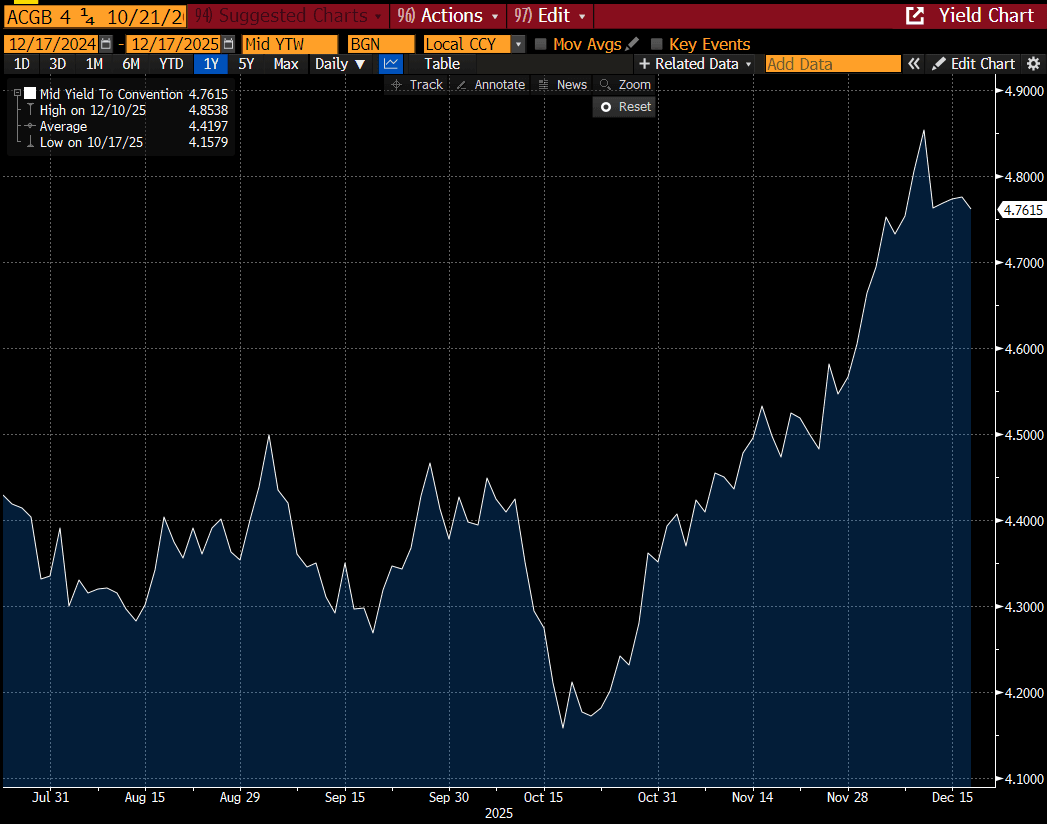

- The AOFM plans to sell A$1000mn of the 4.25% 21 October 2036 bond today. The Oct-36 bond was issued by syndication at a yield to maturity of 4.36% in late July, compared to its current level of 4.76% (see chart).

Bloomberg Finance LP

NEW ZEALAND: Q3 Current Account Deficit, As % Of GDP, Continues Improvement

The Q3 headline current account deficit widened to -NZD8.365bn, from, -NZD1.297bn in Q2, but this is part of the typical seasonal norms. In seasonally adjusted terms we were slightly wider in Q3 at -NZD3.8bn. As a percent of GDP, the deficit was -3.5% in YTD terms, slightly wider than the -3.4% forecast but still an improvement on the Q2 outcome of -3.7%. The deficit trend as a share of GDP continues to improve, we were at -9.0% of GDP at the end of 2022.

- The bulk of the deficit remains on the income side, close to -NZD3bn. The goods and services balances remain modestly in deficit.

- The goods balance has improved in recent years. Focus going forward will be on export growth, amid signs that whole milk prices are trending lower, a key NZ export. Imports may also improve if we see a stronger domestic demand impulse.

- Note this Friday delivers Nov trade data.

- The NZD will be influenced by the structural current account deficit trend, with the Kiwi likely to remain sensitive to risk off episodes in global markets. Near term correlations though ware likely to remain strong with NZ-US rate differentials.

BONDS: NZGBS: Little Changed Despite Modest Post-Data Rally By US Tsys

NZGBs are unchanged despite US tsys finishing moderately richer, but off post data bests. Focus turned away from the 4.6% unemployment rate with possible assistance from that heavy -105k in Oct NFP. Rounding and already known higher survey error saw retrace gains.

- Retail sales growth was flat in October after rising 0.1% prior, a little softer than the expected 0.1% gain - core sales were significantly stronger than expected, implying strong retail momentum at the start of Q4.

- No Fed speakers during yesterday's session. Focus on Wednesday in the US: several regional Fed economic measures, Fed speakers (Waller, Williams, Bostic) and $13B 20Y Bond re-open.

- NZ current account deficit was 3.5% of GDP in the 12 months through September, down from 3.7% in Q2.

- "RBNZ to Phase in New Bank Capital Requirements From Early 2026. The package includes reduced requirements for common equity, more granular risk weights, simplification of capital instruments, and greater alignment of instruments for the "big four" banks with Australian settings." (see BBG link)

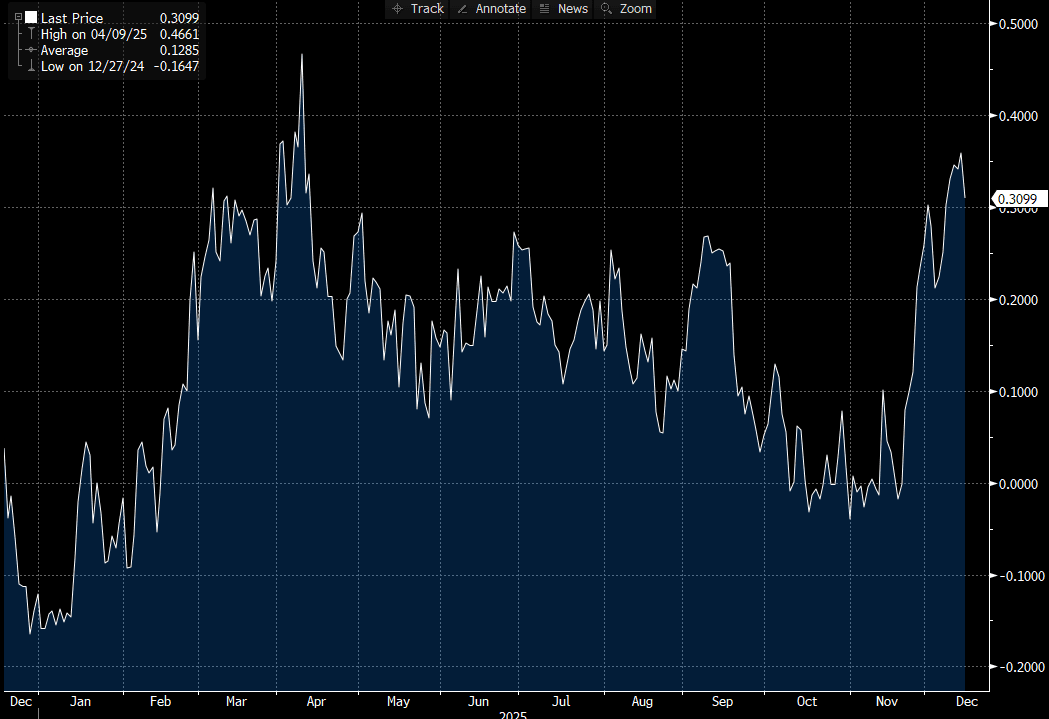

- NZ-US 10-year yield differential is 3bps wider at +31bps (see chart).

- Swap rates are little changed.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while November 2026 assigns 44ps.

Bloomberg Finance LP