CNH: USD/CNH Fixing Error Rises, USD/CNH Still Close To Recent Lows

The USD/CNY fix printed at 7.0686, versus a BBG market consensus of 7.0528. This was a decent drop on yesterday's fixing outcome, in line wi9th USD softness. This continued the recent trend of positive fixing errors though(today's outcome was +158pips). This is slightly below recent highs on this metric of +164pips, seen on Dec 4.

- USD/CNH is little changed in response, holding near 7.0550 in latest dealings, close to recent lows from Dec 3 (7.0540). Headlines crossed a short while ago that Mexico will impose tariffs on China goods next year of up to 50%. The market reaction has been minimal (the Mexico government talking about implementing such tariffs for quite a number of months).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

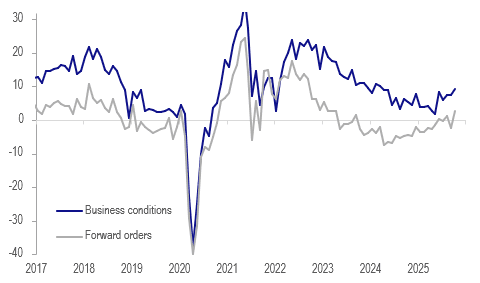

AUSTRALIA DATA: NAB Survey Signals Ongoing Recovery & Lower Inflation

NAB business confidence and conditions were little changed in October with the former down 1 point to +6 and the latter up 1 point to +9. The survey details were generally positive though with forward orders positive and their highest in two and a half years, investment up, labour demand steady and cost/price increases moderating. It is consistent with an ongoing economic recovery and contained inflation and therefore the RBA on hold.

Australia NAB business survey outlook

Source: MNI - Market News/LSEG

- Business conditions rose to their highest since March 2024 with profitability up 3 points, trading +5 and employment steady but one point below the 2025 average. Capital expenditure rose 4 points to +11. While exports remained positive, they are struggling as they weakened in October.

- The labour demand component is currently signalling a stabilisation in employment growth, which has trended lower since mid-year.

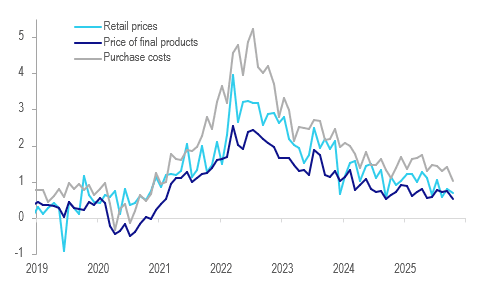

- The 3-month change in purchase costs moderated to 1.0%, the lowest since February 2021 and below Q3’s 1.4% average. Labour costs rose 1.5% 3m/3m down from 1.6% in September.

- Final product prices increased only 0.5% 3m/3m after 0.75% in Q3 and the slowest since February 2021. Retail prices increased 0.7% 3m/3m after Q3’s 0.8%.

Australia NAB business survey price/cost components % 3m/3m

Source: MNI - Market News/LSEG

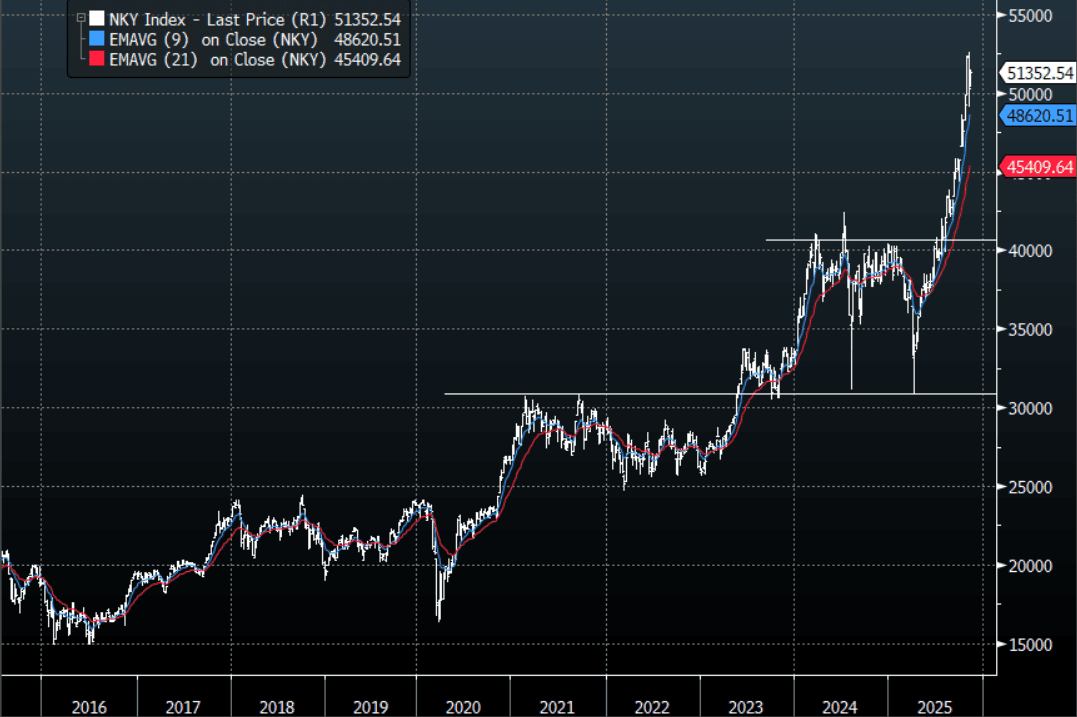

JAPAN: Nikkei(NHZ5) - Surges Back Above 51000 As Global Sentiment Improves

The NHZ5 contract overnight range was 50750 - 51330, closing +1.60%. The Nikkei surged higher overnight with global risk and opened bid again this morning, +0.20%. The Index has gone parabolic starting in August/September, it looked to finally be putting in some sort of a top last week but with global sentiment improving again this price action could potentially continue into year-end. The support between 49000-49500 proved to be solid last week and while this continues to hold, I suspect the bulls will be around on dips as the focus turns back to the year's highs above 52 600 and a potential “Santa Rally.” This price action is pretty wild and the acceleration higher has been relentless but I do become wary when price action becomes parabolic, it's very hard to call a top when the price moves like this but history tells us when it does eventually stall the pullback could be just as brutal.

Fig 1: Nikkei(NHZ5) Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

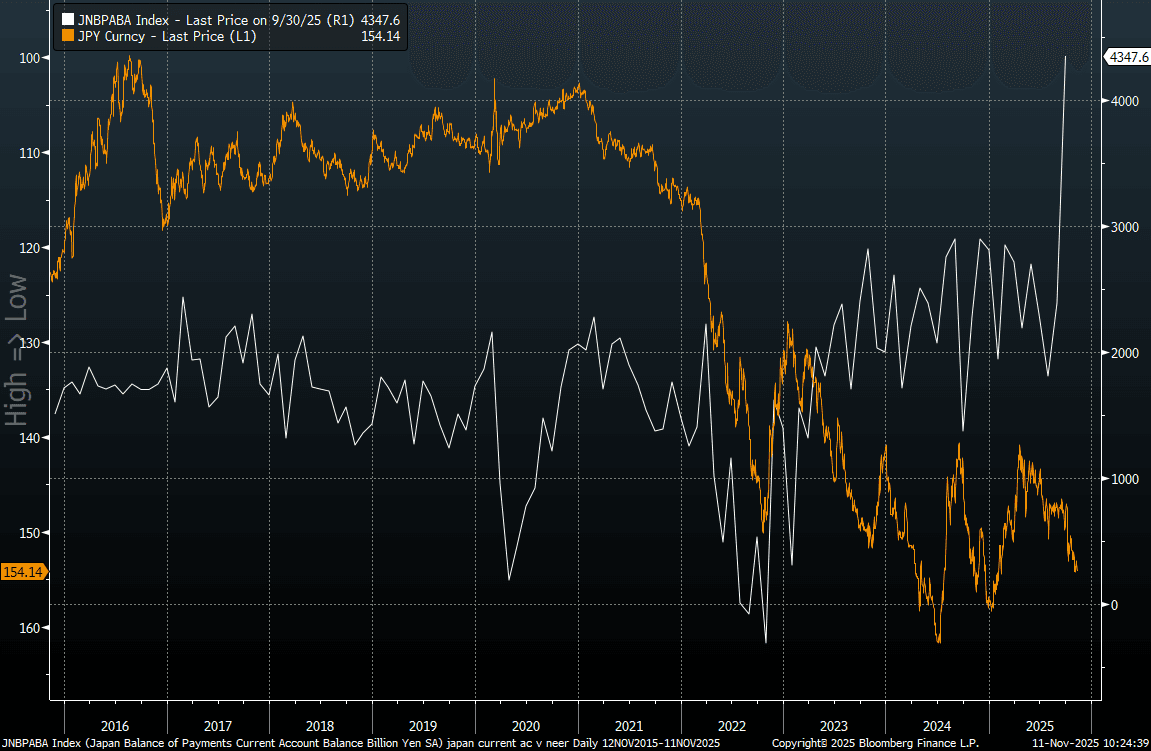

JAPAN DATA: Current A/C Surplus Surges On Income Inflows, But May Not Aid Yen

Japan Sep trade and current account balance data were stronger than forecast, particularly on the current account side. In unadjusted terms we printed ¥4483.3bn, versus ¥2456.6bn projected and ¥3701.4bn prior. In seasonally adjust terms we were at ¥4347.6bn for the current account, close to double the consensus projection and prior outcome. This is the best outcome for at least a few decades. This isn't necessarily a yen positive though, at least based off recent correlations. Current account shifts haven't coincided with yen shifts in recent years.

- The trade balance on a BoP basis aided the current account improvement. We were up to a surplus of ¥236bn, versus a projected deficit of -¥100.1bn. The trade balance remains within recent ranges. The Citi terms of trade proxy for Japan is pointing to positive trade balance outcomes continuing in the near term.

- The bigger driver for the current account improvement though was the surge in the primary income balance, ¥4728.1bn, versus ¥2968.4bn in Aug. These outcomes are usually fairly steady, but point to a pick in net income earned from Japan's offshore investments.

- The chart below plots USD/JPY, which is inverted on the chart (the orange line) against the current account position (the white line). It shows the lack of relationship between the two series, with much of the surplus in Japan potentially re-exported offshore via capital outflows.

- This may benefit the yen at some point, particularly if we see the US authorities (especially Tsy Secretary Bessent) making noises about yen being undervalued relative to Japan's external balances.

- However, this is likely to play out over the medium term rather than in the near term. Short term dynamics around the BoJ/Fed outlooks, which will drive US-JP yield differentials, along with broader risk trends, are likely to remain more important USD/JPY drivers.

Fig 1: Japan Current Account & USD/JPY (Inverted) Trends

Source: Bloomberg Finance L.P./MNI