CNH: USD/CNH - Finds Sellers Back Toward 6.9800

The overnight range was 6.9582 - 6.9786, Asia is currently trading around {CNH Curncy}. The pair pop...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Yields Firmer Following US Moves, AU-US 10yr Spread +60bps

Aussie bond futures have ticked down in the first part of Wednesday trade. 3yr (YM) was last off 2.5bps to 95.785, while the 10yr (XM) was off 1bps to 95.18. This follows a firmer US Tsy yield backdrop from Tuesday's overnight session, as better than expected Q3 GDP data for the US aided front end yields (2yr up +3bps, 10yr year around flat). ACGB yields are 1-2bps firmer in early dealings, with the front end slightly outperforming.

- Aussie 10yr futures remain towards the bottom end of recent ranges. Recent lows rest at 95.12, with downside focus likely to rest on a test under 95.00. Any recoveries need to break back above 95.900 (the Oct 17 high) to signal near-term bullish traction.

- On the cash yield side for the 10yr a push above the 4.80% region (last near 4.76%) is likely to remain topside focus. A break above this region would bring 5.00% into focus. The 20-day EMA sits back around 4.685%.

- For the 3yr cash yield, we are more the mid point of recent ranges (last 4.13%), with the 20-day EMA near 4.04%, while recent highs were marked just above 4.20%.

- The 3/10s curve is steady at +63bps, while the AU-US 10yr spread is around +60bps, little changed so far this week.

- Market pricing for the Feb meeting next year has remained fairly steady with hike odds around 34% per OIS pricing. By Dec next year the OIS implied rate sits just above 4%.

- The local data calendar swings back into gear in early Jan next year. Note that Nov CPI prints on Jan 7 (local markets are shut tomorrow and Friday).

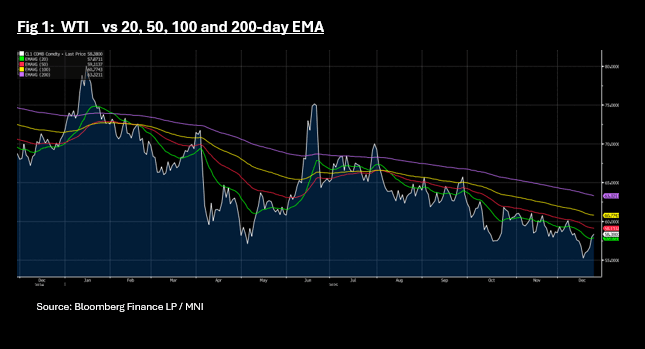

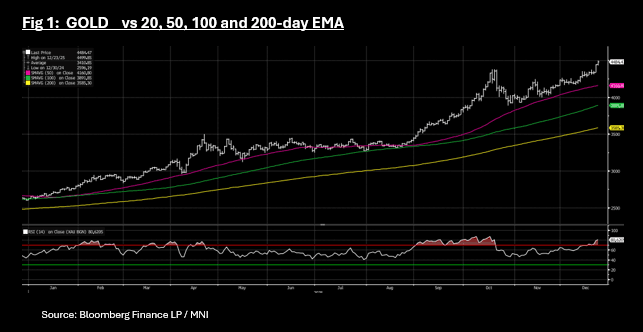

COMMODITIES: WTI Through Key Tech Level; Gold Overbought on RSI

- The US has boarded a Venezuelan oil tanker, is in pursuit of a second tanker by the US coastguard and seized another as Washington ramps up its pressure on Venezuela and the government of Maduro.

- The ongoing threat to Venezuelan shipments, the unresolved conflict in Ukraine and the rising threats from the US of land strikes on drug operations continue to weigh heavy on oil prices.

- A cargo of Russian crude from US-sanctioned Rosneft PJSC has finally been delivered to a Chinese oil terminal after spending three months at sea, ship-tracking data from BBG show.

- WTI finished the US trading day up +0.88% to US$58.46 bbl. The gains takes WTI back to flat for December in what has been a volatile month with ranges from US$55.18 to US$60.14.

- The gains takes WTI back above the 20-day EMA of US$57.87 with topside resistance from the 50-day EMA of US$59.11

- Brent finished up +0.73% at US$62.51 bbl but remains down by -1.1% for December. Brent too has moved above the 20-day EMA of US$61.75 bbl with topside resistance from the 50-day EMA at US$63.00 bbl

- Gold closed at a new high of US$4,484.47 overnight following gains of +0.92%.

- That leaves gold up +71% year to date in what has been a record breaking year for the precious metal.

- Ongoing volatility from the US trade war has supported gold this year but the key has been the uptick in purchases from key central banks looking to diversify away from the USD.

- Exchange-traded funds added 388,309 troy ounces of gold to their holdings in the last trading session, bringing this year's net purchases to 15.4 million ounces, according to data compiled by Bloomberg. This was the biggest one-day increase since Sept. 26.

- Gold continues to be overbought on the 14-day relative strength index, where it spent most of September and October.

BONDS: NZGBS: Yields Drift Down Despite US Tsy Yield Gains, Mkts Shut Thurs/Fri

NZGB yields sit down a touch in the first part of Wednesday dealings, despite a mostly positive yield lead from US Tsys on Tuesday. NZGB yields are down close to 1bps for most parts of the curve. The 2yr rests at 2.71%, the 10yr near 4.43%. US Tsy price action gapped lower overnight after stronger that expected economic data (Q3 GDP +4.3%) that tempered rate cut expectations through mid-2026 (June '26 the first FOMC date to price in a 25bp cut). US Tsy yields finished -1 to +3.5bps firmer across the curve, with the front end outperforming in yield terms.

- Broader ranges remain intact for NZGBs are we approach the Christmas break. The 2yr remains close to recent lows just under 2.70%, while the 10yr remains up from recent lows sub 4.40%.

- The 2/10s curve is at +172bps, so off recent cycle highs. The NZ-US 10yr spread is at +29bps, so slightly tighter. Earlier Dec highs for this spread were near +40bps.

- The NZ 2yr swap rate (NDSO) is a touch weaker, but at 2.75% remains comfortably within recent ranges as well.

- On the data front, the data calendar doesn't really swing back into gear until mid January, while note that Q4 CPI prints on Jan 23 next year.

- RBNZ pricing is mostly flat out to the May meeting next year (OIS implied rates holding near 2.25%), while by Oct next year a full 25bps rate hike is more than fully priced.

- NZ markets are shut tomorrow and Friday.