CNH: USD/CNH Edges Up, But Limited Reaction To Weaker July Data

USD/CNH is up a touch, last near 7.1850. Earlier we had softer across the board July activity data, along with further house price declines. The caveat on the data is the authorities noting it was impacted by flooding and higher temperatures. Still, it follows the recent soft new loans data. China equities are modestly higher at this stage, while Hong Kong markets are down over 1%. This was largely reflected at the open though, with not a huge reaction post the data prints.

- Outside of potential monthly disruptions from weather, market impact may be limited given the recent announcement around subsidy plans on loan interest for individuals and businesses aimed at improving consumption.

- For USD/CNH, recent highs rest just above 7.1980.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

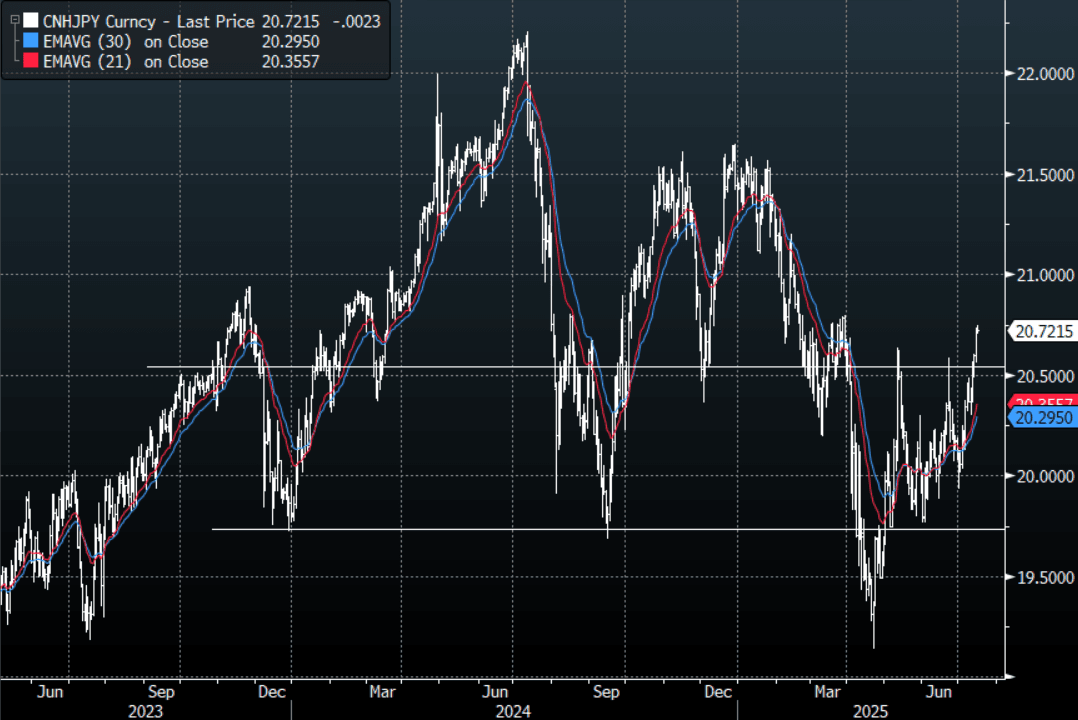

FOREX: JPY Crosses - JPY Longs Remain Under Pressure, Even While Risk Turns Down

This morning has seen US futures open under pressure, ESU5 -0.11%, NQU5 -012%. The USD has surged higher and Stocks reversed lower on the back of the US CPI showing clear signs that tariffs are beginning to impact the core goods data. The JPY continues to underperform in the crosses which is very unusual considering the reversal in risk, this continues to point to a positioning problem. Should the risk backdrop sour even further going forward this should eventually provide these crosses with headwinds to move higher.

- EUR/JPY - Overnight range 172.45 - 173.08, Asia is trading around 172.80. This pair has had a decent move higher and has led the charge against the JPY longs. Short-term it is starting to look a little stretched but the direction is clear and should expect demand on dips. First support 170.50 area then the more important 168.50 area.

- GBP/JPY - Overnight 198.32 - 199.52, Asia trades around 199.35. The pair has failed initially towards the 199.00/200.00 resistance a break of which could see more JPY longs pared back. First support is around 198.00 then the more important 196.50 area. The pair bounced off its first support brushing off Bailey's comments and renewing the pressure on JPY longs.

- NZD/JPY - Overnight range 88.28 - 88.90, Asia is currently dealing 88.60. NZD/JPY broke through the resistance around 88.00 but has failed to really accelerate through it. Price is consolidating above 88.00 looking for a reason to extend. The Support towards 87.00 needs to hold for the focus to remain on the 90.00/91.00 area.

- CNH/JPY - Overnight range 20.55663 - 20.7344 Asia is currently trading around 20.7200. This pair is now breaking back above its pivot and points to potentially further losses from here as positioning is pared back. Look for demand now back towards the 2.40/50 area.

Fig 1 : CNH/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

CHINA PRESS: PBOC Has Further Room For Easing

The People’s Bank of China still has room for cuts in the reserve requirement ratio and interest rates, given low inflation, stable yuan and major economies’ rate-cutting cycle, said Sheng Songcheng, dean at the China Chief Economist Forum Institute. However, the PBOC needs to observe the effects of previous measures before launching new easing, while the timeframe for monetary policy transmission could be longer than the usual 3-6 months if there is greater economic downward pressure, said Sheng. (Source: National Business Daily)

AUSSIE BONDS: Cheaper But At Session Bests, Strong Demand Seen At Mar-36 Auction

ACGBs (YM -2.0 & XM -3.5) are cheaper but sit near Sydney session bests.

- (Bloomberg) The prime minister of Australia, Anthony Albanese, sought to focus his trip to China on business and trade opportunities, sidestepping thornier issues around US-China competition.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session after yesterday's post-CPI sell-off.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -7bps.

- The latest ACGB Mar-36 auction saw strong demand, with the weighted average yield coming in 0.41bps through prevailing mid-yields, according to Yieldbroker, continuing the trend of firm pricing at recent ACGB auctions. Moreover, the cover ratio rebounded to a solid 4.45x from 2.5792x.

- The bills strip cheaper with late whites leading and pricing -2 to -3.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in August is given an 87% probability, with a cumulative 54bps of easing priced by year-end.