CNH: USD/CNH Downtrend Continues, Yuan Outperforming Cross Asset Trends

Spot USD/CNH hit fresh year to date lows of 7.0480 on Thursday, before edging slightly higher. We track near 7.0500 in early Friday dealings, after CNH gained 0.12% for Thursday's session. If USD/CNH can consolidate its break under 7.0500, the next downside focus point will be 7.00. On the upside, all key EMAs are tracking lower, the 20-day EMA back up at 7.0760/65. Broader USD sentiment was softer Thursday, with the BBDXY index down a further 0.25%, after Wednesday's 0.44% fall. Spot USD/CNY finished up at 7.0571, while the CNY CFETS basket tracker lost a little ground to 97.67.

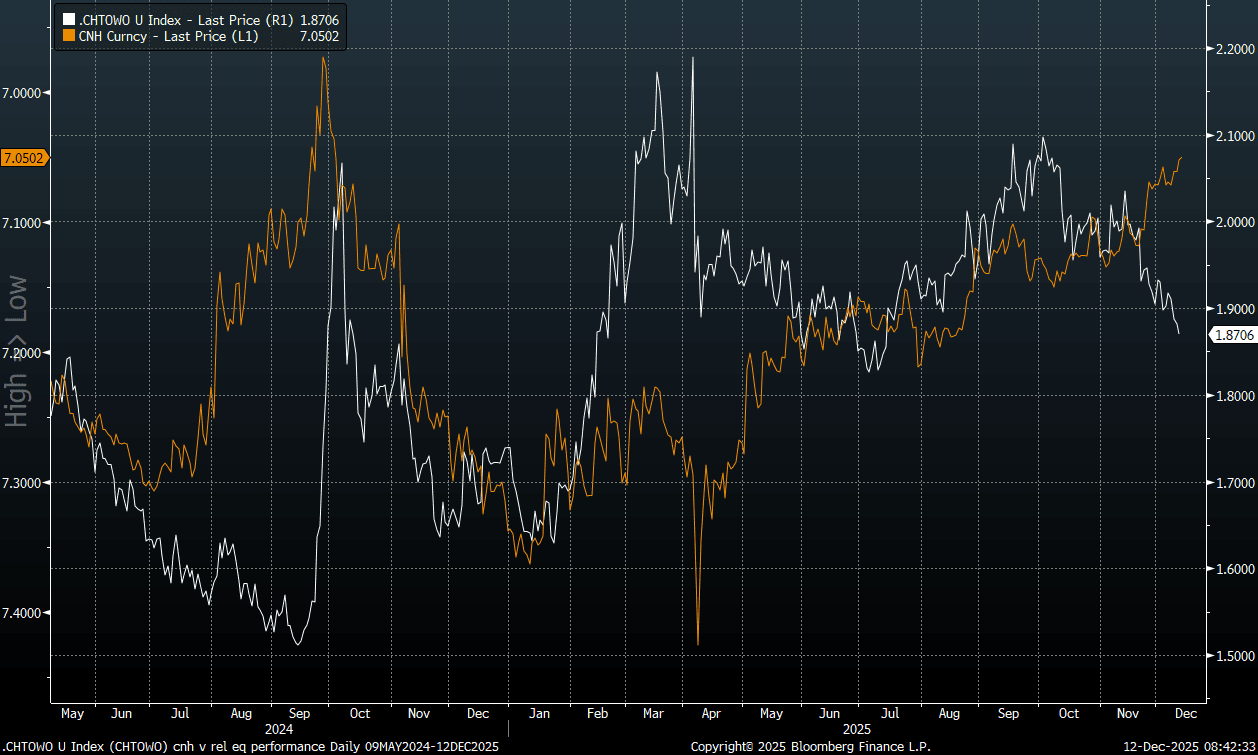

- The yuan is outperforming a steadier US-CH yield differential backdrop, with 2yr spreads around +213bps, while China equities are also lagging the broader equity rally. The chart below shows USD/CNH inverted against the China to global equity ratio.

- We are in a typically seasonally stronger time of year for CNH and the yuan, which tends to rally through Jan and into the China new year period. Fresh yuan gains may also be prompting on-going conversion of offshore proceeds into the local currency.

- News flow late yesterday focused on the conclusion of the Central Economic Work Conference. Via our China policy team: China will maintain necessary fiscal expansion and prioritise stabilising economic growth and promoting a price rebound in monetary policy for next year, Xinhua News Agency.

- While on housing: Authorities will focus on the city-specific polices to control new housing supplies and reduce inventory, encouraging the acquisition of unsold homes with the prime purpose of providing affordable housing, the meeting said.

Fig 1: USD/CNH Inverted Versus China To Global Equity Ratio

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (Z5) Struck by Strong CPI

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.310 @ 16:15 GMT Nov 11

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Having bounced well on the back of the mild US CPI print, Aussie 3-yr futures reversed course last week on strong domestic inflation data containing RBA cut pricing through 2026. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 96.280 as the next major support.

AUSSIE BONDS: Modestly Stronger, Jobs Data Tomorrow

ACGBs (YM +1.0 & XM +2.0) are modestly stronger after US tsy futures closed firmer.

- Looking ahead, Wednesday’s US data is limited to MBA Mortgage Applications and $42bn 10Y Note. Focus on multiple Fed speakers through the session: Williams, Paulson, Waller, Bostic, Miran and Collins.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +25bps.

- The bills strip is little changed across contracts.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 9% probability, with a cumulative 16bps of easing priced by mid-2026.

- Interestingly, AU-NZ 1-year forward 3-month swap (1Y3M) spread at 103bps is now at its highest level since 2012.

- Today, the local calendar will see Home Loan data alongside RBA Jones' Fireside Chat.

- However, the highlight of this week's AUS calendar will be Thursday's October jobs data. The unemployment rate rose 0.2pp to 4.5% in September.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035bond today and A$800mn of the 1.75% 21 November 2032 bond on Friday.

GOLD: Corrective Phase Over, US Data Release Schedule Likely Next Week

Gold increased back above $4140 following concerning US ADP data but the move wasn’t held with it then falling to $4097.25. It has recovered somewhat to $4126.85 to be up 0.3% and 3.1% in November finding support from the weaker US dollar (BBDXY -0.1%). The market has around a 67% chance of a December Fed cut but gold’s response to the upcoming end of the US government shutdown signals that it thinks the delayed data will drive increased easing expectations when it is released.

- Advance ADP data suggested private sector job losses in the four weeks to 25 October but the providers noted the data is preliminary and could be revised.

- Our US analysts believe that the post-shutdown data schedule should be published next week but there is a risk that October CPI won’t be released. See their FAQ here.

- Bullion reached $4149.0 on Tuesday, remaining below initial resistance at $4161.4, 22 October high. The recent recovery in gold prices marks the end of the corrective phase which allowed the overbought condition to unwind. The bull trigger is at $4381.5. A decline below the 50-day EMA at $3890.0 would signal scope for a deeper retracement.

- Bloomberg reported gold ETF outflows in the 3 weeks to November 7 following 8 weeks of inflows.

- Silver rose to $51.252, remaining below initial resistance at $52.374, following the ADP data and then fell to $50.290. It then recovered to $51.221 to be up 1.4% on the day and 5.2% on the month. The trend remains bullish with the metal continuing to trade above the 50-day EMA at $46.484.