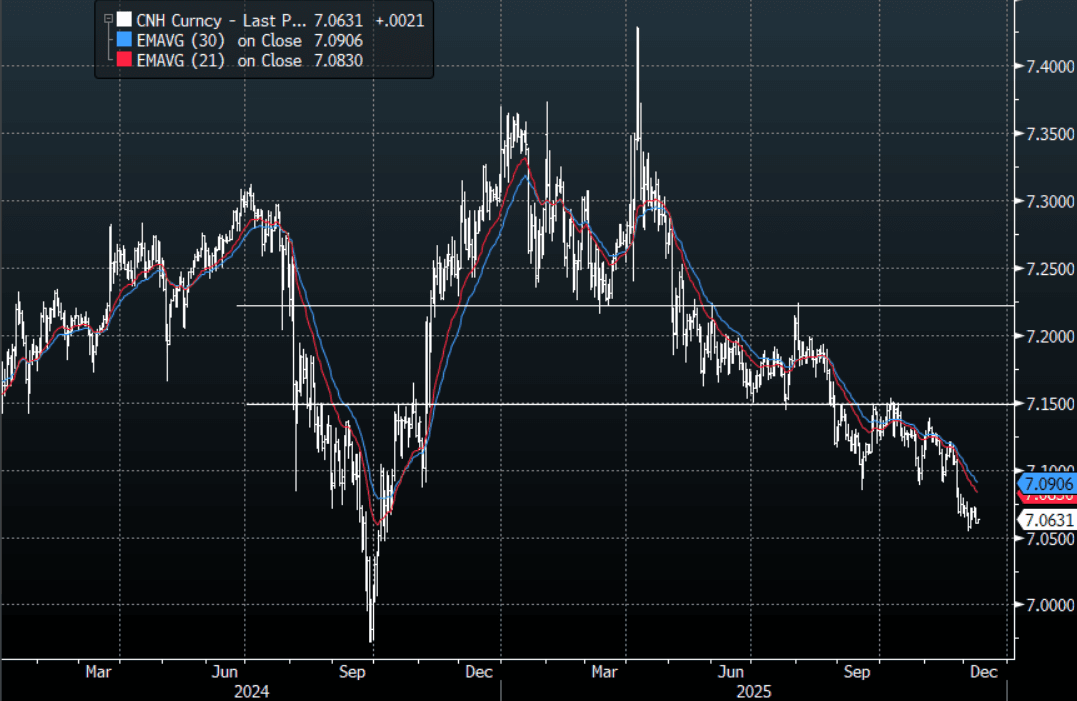

CNH: USD/CNH - Continues To Trade Heavy Below 7.0700

The overnight range was 7.0600 - 7.0702, Asia is currently trading around 7.0630. The pair continues to trade heavy for the moment ignoring the rebound in the USD. The pair still looks to be under pressure and the PBOC has a job on its hands to turn this around, especially with the surplus now over $1 trillion. US yields are much higher over the week as we head into the FOMC and the USD is bouncing, does the PBOC push back on the stronger CNY today ? On the day resistance is back toward the 7.0750-7.0850 area at first then 7.10-12 above. I suspect sellers will be lining up again on a bounce back towards the 7.0900-7.1200 area if they do see it.

- Brad Setser posted on X regarding comments from Jens Eskelund: “Amazing pair of stats from Jens Eskelund of the European Chamber in China -- who comes from the shipping industry and knows this data cold.”

- “Eskelund says that China’s trade imbalance with the world is even more pronounced than the $1 trillion figure suggests, given the relative weakness of the Chinese yuan. When calculated by value, China accounts for roughly 15% of global goods exports. But in volume terms, Eskelund estimates that every shipping container being sent from Europe to China is outnumbered by the four containers heading in the other direction. In volume terms, he estimates that China accounts for some 37% of everything being exported in shipping containers.”

- https://www.wsj.com/economy/trade/chinas-exports-rebound-in-november-97f24e06?st=s9TUrb

- USD/CNY Options : Closest significant option expiries for NY cut, based on DTCC data: 7.1088($1.2b). Upcoming Close Strikes : none - BBG

- The USD/CNH Average True Range for the last 10 Trading days: 122 Points

- Data/Event : Money Supply, CPI and PPI are out today with modest improvements forecast for CPI, whilst PPI remains firmly negative.

Fig 1 : USD/CNH Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

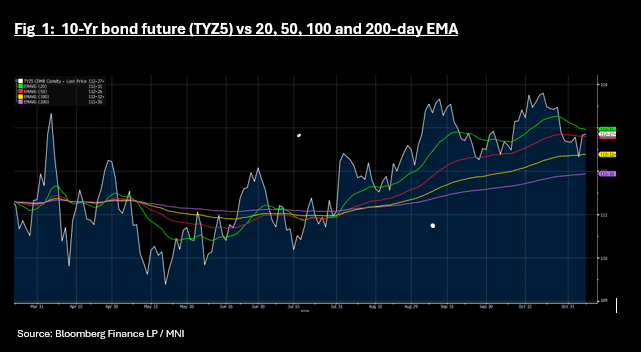

US TSYS: TYZ5 Back Above Key Technical

The 10-Yr bond future finished the week last week higher at 112-27+, back above the 50-day EMA of 112-26+, but below the 20-day EMA of 112-31+.

For cash, yields trended higher over the week as the front end underperformed as uncertainty grows over the next Fed Meeting and the likelihood of a rate cut. The market had priced in a full cut for December but as the uncertainty around that continues, yields may rise.

- The 2-Yr finished the week at 3.56%, a gain of +8bps.

- The 5-Yr finished the week at 3.68%, flat on the week.

- The 10-Yr ended at 4.09%, a rise of 2bps. The 10-Yr has consolidated back above 4% again, and look set to trade back in the 4.00% - 4.20% range.

- The 30-Yr was at 4.70%, up +5bps for the week.

The key auction tonight will b e a US$86bn 13-week and US$77bn 26-week bills auction. The key test will be the US$42bn 10-Yr on the 13th.

There is no scheduled Tier 1 data tonight.

AUSSIE BONDS: Subdued Start To Week, Thurs' Jobs Data In Focus

ACGBs (YM -1.0 & XM -0.5) are slightly weaker after cash US tsys closed on Friday, little changed, having teetered either side of flat. Risk-off flows after the UofM confidence data supported early on but faltered as Wall Street recovered.

- The highlight of this week's AUS calendar will be Thursday’s October jobs data. After the unemployment rate rose 0.2pp to 4.5% in September, the release will be monitored to see if there is any stabilisation.

- Last month’s weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report. (see chart)

- Today, RBA Deputy Governor Hauser speaks at 1030 AEDT on the Outlook for the Australian Economy.

- Cash ACGBs are 1bp cheaper with the AU-US 10-year yield differential at +26bps. At this level, the differential hovers just below the upper bound of its long-established range.

- The bills strip is slightly weaker across contracts.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at an 11% probability, with a cumulative 19bps of easing priced by mid-2026.

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035bond on Wednesday and A$800mn of the 1.75% 21 November 2032 bond on Friday.

Bloomberg Finance LP

BONDS: NZGBS: Little Changed To Start The Week, RBNZ Inf Exp Tomorrow

NZGBs are unchanged after US tsys finished the NY session modestly cheaper on Friday as early risk-off sentiment moderated.

- On Friday, Republicans rejected Senate Democrats on ACA subsidy as the US Govt shutdown looks to enter it's sixth week next week. However, Bloomberg is reporting, "Senate Republican leader John Thune said a deal is "coming together" as he planned a Sunday vote to end the US government shutdown."

- MNI Tech: A short-term bearish threat in 10-year tsy futures (TYZ5) remains intact. Sights are on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-07. Clearance of these price points would expose a trendline support at 112-00 - the trendline is drawn from the May 22 low.

- Fed Vice Chair Jefferson (voter) on wanting to proceed slowly, being closer to a neutral level rather than talking on Powell’s “fog”. He does, though, note a meeting-by-meeting stance being especially prudent with a lack of official data.

- Swap rates are little changed.

- RBNZ dated OIS pricing is little changed across meetings. 28bps of easing is priced for November, with a cumulative 37bps by February 2026.

- Today, the local calendar will be empty. The next release of note will be the RBNZ's Inflation Expectations data tomorrow.