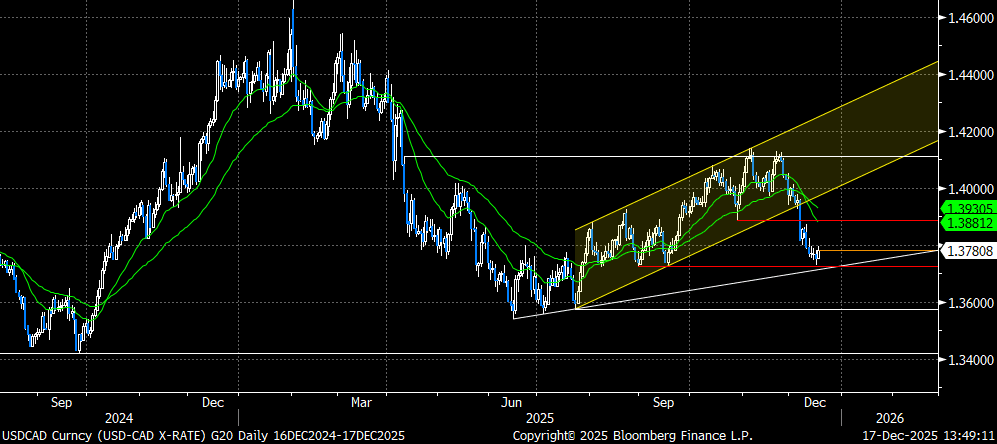

FOREX: USDCAD Meets Primary Target Yesterday, Bearish Trend in Place

Dec-17 13:49

- Despite the current 0.63% recovery for the dollar index from yesterday’s post-NFP lows, USDCAD has relatively underperformed with just a 0.38% rise. Oil prices may be providing a moderate CAD boost here, after President Trump ordered a complete blockade of all sanctioned oil tankers entering and leaving Venezuela while additional sanctions have been threatened against Russia.

- For USDCAD, yesterday’s dip following the US jobs data essentially matched the first primary target for the selloff, trading to within 3 pips of the September lows at 1.3727. Subsequently, price has been consolidating below the 1.38 mark, keeping short-term bearish trend conditions in place following the technical breakdown earlier in the month.

- Further weakness would encounter trendline support just above the 1.37 handle, while 1.3682 (76.4% retracement of the Jun 16 - Nov 6 bull cycle) and 1.3576 (Jul 23 low) represent the next supports. Lows for the year come reside at 1.3540.

- Following tomorrow’s US inflation figures, domestic retail sales data for October is scheduled Friday, before next week’s October GDP release. As a reminder, within the last stellar GDP report from Canada, a contraction in October's flash reading suggests weakness ahead.

- Coming out of last week’s BOC meeting, markets price in ~25bp of cumulative hikes through the October 2026 meeting, with the path through H1 2026 almost completely flat.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

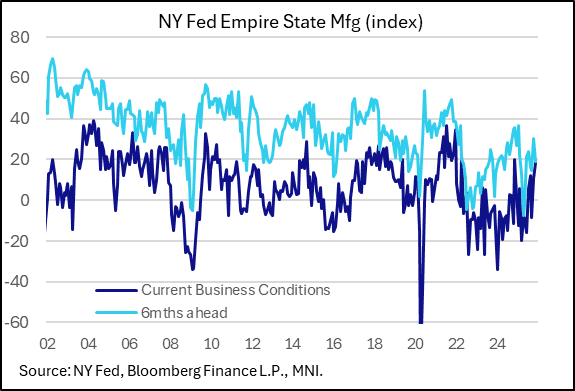

US DATA: Empire Manufacturing Solidifies For 2nd Consecutive Month

Nov-17 13:49

The NY Fed's Empire State Manufacturing Survey impressed in November, with the current General Business Conditions index rising 8 points to a 1-year high 18.7 (well above the 5.8 expected). As such it's the 2nd highest reading since April 2022, with solidly-above-long-term average-readings now for 2 consecutive months, the first time we've seen that since 2021 for this notoriously volatile survey.

- The 6-month outlook pulled back 19.1 from to 30.3 prior, which had been the highest optimism since January.

- Activity indices were strong. New orders jumped to 15.9 from 3.7, setting a 12-month high just 2 months after setting a 17-month low; shipments rose 2 points to 16.8 while inventories turned positive after 3 consecutive negative months.

- The employment gauge edged up to 6.6 from 6.2, for a fresh 4-month high, while the average workweek rose to a multiyear high.

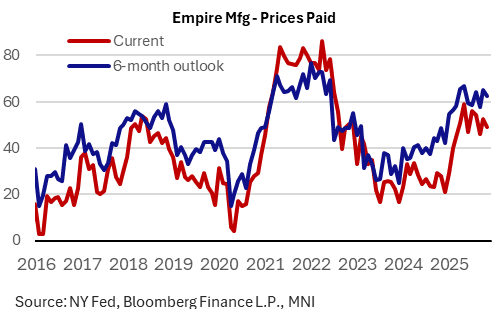

- Inflation remained stubbornly high but didn't show signs of worsening. Current prices paid fell to 49.0 after 52.4, with expected prices paid 6-months ahead down to 62.5 from 65.0. Both are elevated but suggest some moderation after October's sharp M/M rise that suggested inflation was picking up alongside with activity.

- In short, a solid start to the month's regional Fed manufacturing surveys.

GLOBAL POLITICAL RISK: Week Ahead 17-23 November

Nov-17 13:47

Download Full Report Here

Monday 17 November:

- Ukraine-France: French President Emmanuel Macron is hosting his Ukrainian counterpart, Volodymyr Zelenskyy, in Paris. During their meeting at Villacoublay air base near Paris, the two signed a letter of intent for Ukraine to purchase up to 100 Rafale fighter jets, as well as other French-made military equipment, in its efforts to repel Russia’s invasion. The purchases are due to be realised over a period of around 10 years, although questions remain on the ability of Kyiv to fund these purchases, having signed a separate letter of intent to purchase 100-150 Gripen jets from Sweden.

US TSY FUTURES: BLOCK: Dec'25 5Y Buy

Nov-17 13:45

- +5,000 FVZ5 109-04.5, post time offer at 0836:59ET, DV01 $213,500.

- The 5Y contract trades 109-05.25 last (+1.25)