ASIA FX: USD/Asia Dips Supported In North East Asia, As Oil Rises

In North East Asia FX markets, USD/KRW dips under 1460 have been supported, while USD/CNH was tracking lower, aided by the CNY fixing, but sits back unchanged now (last near 6.8950). USD/TWD is under 31.70, after making fresh highs of 31.78 yesterday (back to May of last year). USD/HKD spot is edging a little higher, but remains under 7.8200, as it continues to recover from Tuesday's sharp pullback to 7.8000. Equity markets are higher throughout the region, rebounding from yesterday, but the continued rise in oil prices, is an offset to this better risk mood.

- There have been a host of headlines emanating out of China as the National People's Congress gets underway. Growth is seen 4.5-5.0% range for 2026, (from around 5% last year). Via our China policy team, it reflects changing dynamics in China's economy and the external environment, as well as a balance between necessity and feasibility. Policy accommodation is expected to continue, while fiscal policy looks similar to last year.

- USD/CNH didn't react much as the headlines crosses, while the USD/CNY fixing fell to 6.9007, fresh lows back to 2023. USD/CNH saw a brief dip under 6.8800, but we are now back around 6.8950, little changed for the session. Moves above 6.9300 are drawing selling interest, while the CNY basket tracker is just off recent highs.

- Spot USD/KRW got to 1455.70 in the first part of trade, but we have steadily recovered since, last 1466/67. We may chop around this 1460/80 region, until the risk picture becomes clearer (and/or oil prices lose some risk premium). Onshore equities have surged, largely recouping yesterday's plunge (the Kospi is up 11%, but still sub end Feb levels).

- USD/TWD is holding at 31.68, so under Wednesday highs of 31.78, but still within striking distance of a move back towards 32.00.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Cheaper After RBA Decision But Off Worst Levels

ACGBs (YM -9.5 & XM -5.5) are holding weaker but well above session cheaps seen shortly after the RBA policy decision.

- The RBA Board unanimously decided to raise the cash rate by 25bps to 3.85%, citing stronger-than-expected private demand, greater capacity pressures than previously assessed, and a still tight labour market.

- The Bank's updated forecasts showed headline inflation rising to 4.2% by June, up from November's 3.7%, before returning below 3% by June 2027 at 2.9%, 20 basis points higher than previous estimates. The projections assume a higher cash rate, peaking at 4.3% by December 2027.

- "RBA GOV BULLOCK: CANNOT ALLOW INFLATION TO GET AWAY FROM US, PULSE OF INFLATION IS TOO STRONG" - [RTRS]

- "RBA GOV BULLOCK: WILL NOT GIVE FORWARD GUIDANCE, BOARD WILL REMAIN FOCUSED ON DATA " - [RTRS].

- Cash ACGBs are 5-8bps cheaper with the AU-US 10-year yield differential at +57bps and the 3/10 curve flatter.

- RBA-dated OIS pricing is 3-7bps firmer across all meetings, with another 25bp hike more than fully priced by August (+30bps).

- Tomorrow, the local calendar will see S&P Global PMI (Composite & Services).

- The AOFM plans to sell A$1200mn of the 4.25% 21 October 2036 bond on Wednesday and A$800mn of the 1.00% 21 December 2030 bond on Friday.

Bloomberg Finance LP

JGBS: Cheaper But Holding Above Worst Levels Despite Poor 10Y Auction

JGB futures are weaker, -27 compared to settlement levels, but holding above today’s session low despite today’s lacklustre 10-year bond auction.

- The 10-year JGB auction delivered weakish results, with the low price failing to meet expectations at 98.75, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.0196x from 3.3037x. The tail was unchanged 0.05.

- This performance came despite an outright yield hovering just below the cycle high, around 15bps higher than the level of last month's auction.

- The 2s/10s yield curve was also steeper than last month’s auction, although around 20bps below its a cycle high.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday’s heavy session.

- Cash JGBs are mixed across benchmarks, with yields 3bps higher (5-year) to 2.5bps lower (30-year). The benchmark 10-year yield is 1.4bps higher at 2.258% versus the cycle high of 2.359%.

- Swap rates are also slightly mixed with a flattening bias.

- Tomorrow, the local calendar will see S&P Global PMI (Composite & Services).

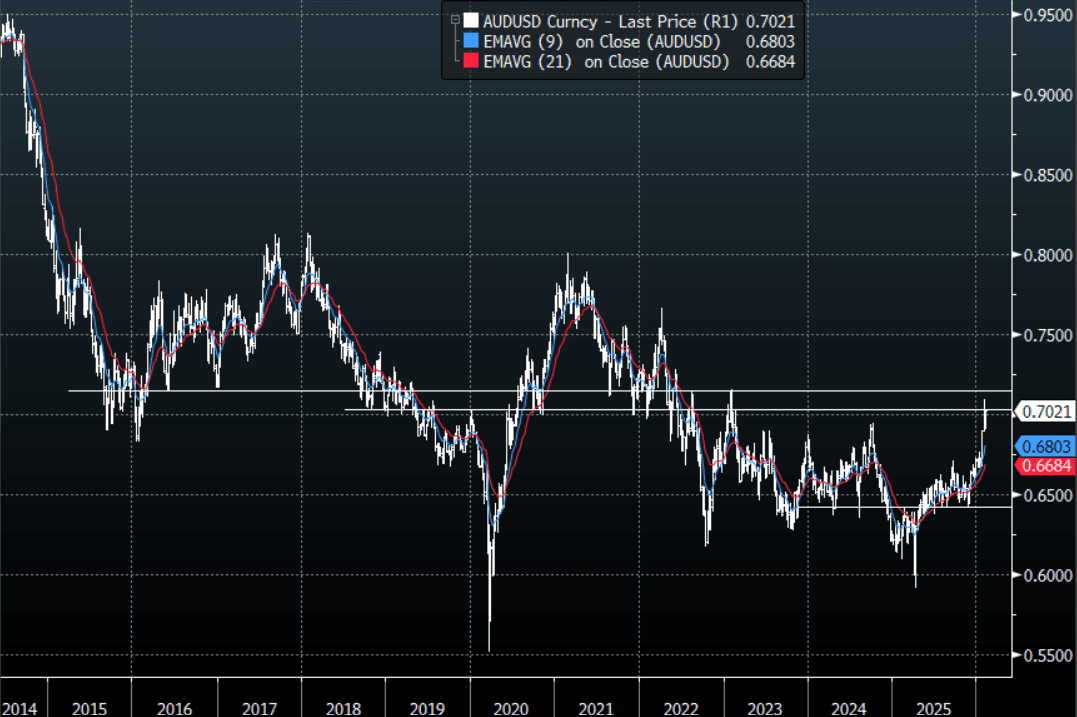

AUD: AUD/USD - Back Above 0.7000 On A Hawkish Hike, Dips To Be Supported

The AUD/USD has had a range today of 0.6945 - 7033 in the Asia- Pac session, it is currently trading around 0.7020, +1.05%. The AUD has exploded higher thanks to a hawkish hike by the RBA. The AUD has been outperforming across the board as leveraged funds increase their longs anticipating today's hike and I suspect these trades will now begin to be added to. The AUD has moved quickly back to 0.7030 where I suspect we find some initial resistance, but this should now see the AUD supported on dips. On the day, the first buy-zone is back toward the 0.6965-0.6985 area, looking for a break above 0.7030 which could give it the momentum to retest the pivotal 0.7100-0.7200 area.

- MNI BRIEF: RBA Lifts Cash Rate To 3.85% On Higher Demand. The Reserve Bank of Australia Board unanimously decided to raise the cash rate by 25 basis points to 3.85% on Tuesday, citing stronger-than-expected private demand, greater capacity pressures than previously assessed, and a still tight labour market.

- The Bank’s updated forecasts showed headline inflation rising to 4.2% by June, up from November’s 3.7%, before returning below 3% by June 2027 at 2.9%, 20 basis points higher than previous estimates. The projections assume a higher cash rate, peaking at 4.3% by December 2027.

- MNI AU - RBA-dated OIS pricing is 3-7bps firmer across all meetings, with another 25bp hike more than fully priced by August (+30bps).

- "RBA GOV BULLOCK: CANNOT ALLOW INFLATION TO GET AWAY FROM US, PULSE OF INFLATION IS TOO STRONG" - [RTRS]

- "RBA GOV BULLOCK: WILL NOT GIVE FORWARD GUIDANCE, BOARD WILL REMAIN FOCUSED ON DATA " - [RTRS]

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6830(AUD315m), 0.6900(AUD338mm). Upcoming Close Strikes : 0.6875(AUD913m Feb 6), 0.6950(AUD1.96b Feb 4) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 81 Points

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P