FOREX: USD On Backfoot Headed Into Prelim UMich Sentiment

With the pullback in the USD persisting through the US cash equity open - EUR/USD stretched again to a new daily high, putting price closer to flat on the week. More notably, 1.1665 marks the prevailing level before Tuesday CPI - reversing the entirety of the inflation-based losses in the pair.

- For AUD/USD, this keeps the Powell-firing-furore high at 0.6554 as the first upside target headed into the prelim UMich sentiment, at which inflation expectations are expected to hold sticky at 5.0% for the 1-year, but drop to 3.9% from 4.0% on the 5-10-year expectation component.

- AUD/JPY also trades well - the 15-min candle chart shows uptrendline resistance drawn off the Jun30 NY high intersecting at ~98.15 which could contain any further rally here.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK: BOE: Instant Answer questions for BOE June 19 meeting

The Instant Answer questions for the June 19 Bank of England policy decision, due at midday Thursday.

1. Was the Bank Rate changed, and if so by how much?

2. Number of members voting for unchanged Bank Rate?

3. Number of members voting for 25bp cut?

4. Number of members voting for 50bp cut?

5. Number of members voting for other rate decision?

NB: On questions 2-5 we will name the dissenters (and the direction / magnitude of dissent)

6. Did the MPC drop reference to a “gradual approach” from its guidance?

7. Did the MPC drop reference to “careful” in the guidance?

8. Did the MPC drop reference to “restrictive” from its guidance?

9. Did the MPC again say it will “decide the appropriate degree of monetary policy restrictiveness at each meeting”?

10. Did the MPC leave its guidance paragraph materially unchanged versus the March policy statement?

BUNDS: Bund Issuance Risks Approach

- Bunds have given away their temporary gains following middle east escalation in full, and returned to levels seen earlier this month, around the 2.55% yield mark in the 10y segment. Next to global risk sentiment, domestic factors could prove decisive for price action over the next week:

- A Q3 refunding announcement on 24 June will likely be where we will see a material ramp-up of Bund issuance following the debt brake loosening earlier this year, and that announcement looks likely to be followed by a 2025 budget press conference on 25 June from finance minister Klingbeil.

- DFA (the German DMO) has touted the re-introduction of a 7-year Bund for that refunding - we see a Nov-32 maturity most likely, for more details see page 2 of our EGB Daily Supply publication here.

- The 2025 budget will give more clarity around plans for German public investment rising to E110bln this year (channelled through both the core budget and special funds, from around E75bln 2024), the E46bln tax breaks through 2029 (E9.2bln per year on average, or 1.9% of 2024 federal spending), the military spending increase (potential commitment for a gradual move up to 3.5%/GDP), and a more longer-term debt brake reform and structural reform agenda.

- Despite this push, Finance Minster Klingbeil has urged ministries to identify savings and attempts to signal that fiscal prudence remains key for the current government (similar statements seen from Merz). This also comes amid lower tax estimates for Germany (-E6.7bln/year, around 0.2% of GDP or 1.6% of projected revenues at the federal level).

- We'd not be surprised to see an additional sources report from local media potentially citing net issuance for 2025 in the lead-up to the refunding and budget announcements - we will cover accordingly.

- On balance, JP Morgan think "the peak in German government debt will likely be at around 70% of GDP (versus last year’s 62%), rather than the near-90% that the fiscal space would allow."

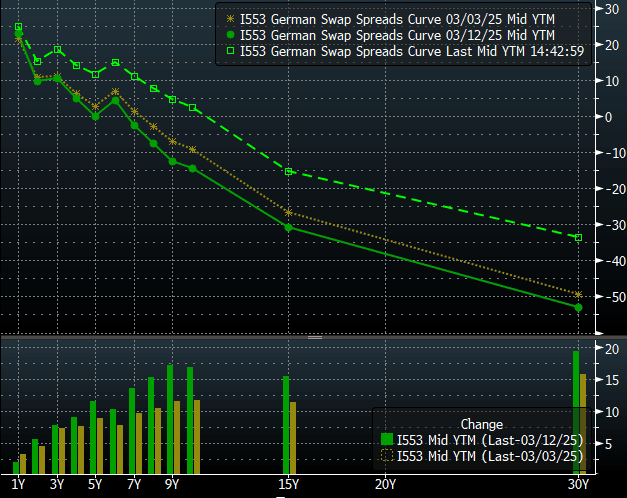

- Swap spreads appear to have largely priced in the German fiscal ramp-up likely being comparatively less pronounced than initially "feared" - since mid-March, German swap spreads have more than reversed their initial tightening seen on the debt brake loosening announcement, widening move than 15bps by now at the long end of the curve.

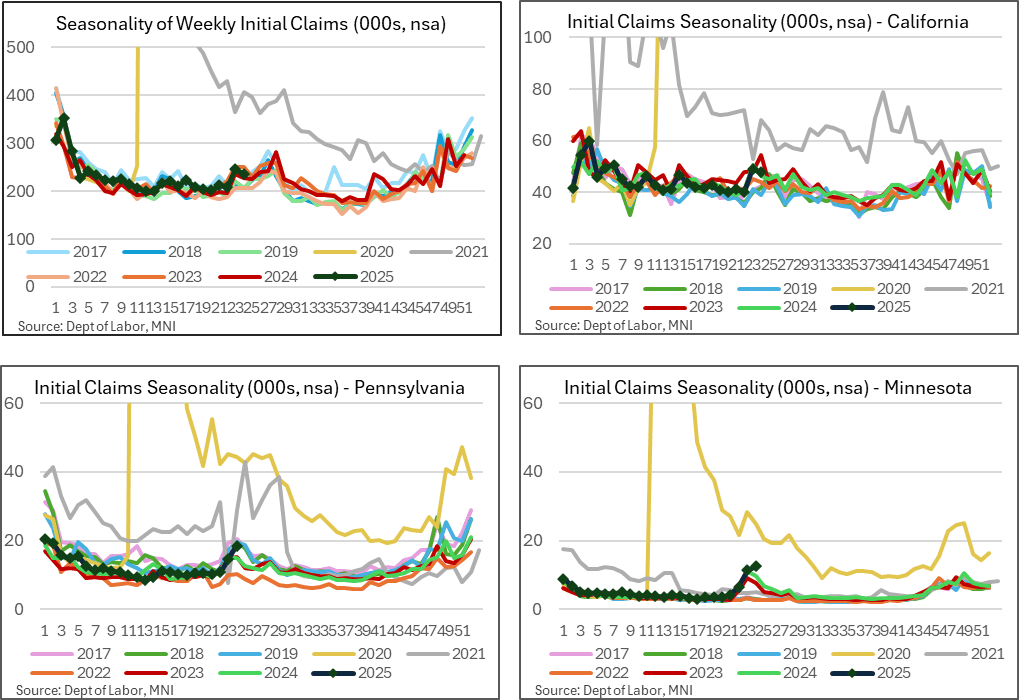

US DATA: Recent Increases In NSA Jobless Claims Relatively Concentrated

The state-levels details of jobless claims data suggest recent increases in non-seasonally adjusted initial claims has been driven by increases in a relatively narrow range of states although a lack of improvement ahead would be notable.

- Adding to the above on jobless claims data, the seasonally adjusted initial claims figures have started to push higher with their highest four-week moving average since Aug 2023.

- The non-seasonally adjusted level of initial claims mostly support this, lifting a little in the past two weeks compared to non-pandemic years although as top left chart shows it’s not wildly different to readings from 2023 and 2024 for the same time of year.

- Of the increase that we have seen, with NSA initial claims rising a cumulative 27k in the latest two weeks, 7.5k has come from California (largest state, similar to 2024 but otherwise elevated) whilst more notable increases for their size have come from Minnesota (+5.9k) and Pennsylvania (+7.7k).

- These latter two are somewhat linked to seasonal norms, but would start to be more notable if they don’t roll over shortly, especially Minnesota.