FOREX: USD Index Rangebound, Trump Announcement Eyed

Aug-06 09:09

- The USD Index holds within a tight range so far Wednesday, keeping the weekly range at 98.585 - 99.073 for now. With relatively little data to distract, focus will remain on Trump's activities this week, particularly as the White House's deadline for Russia establishing a ceasefire with Ukraine expires this Friday. Trump's special envoy is meeting with the Russian President in Moscow today - and any comments following the discussions will be carefully watched.

- As such, the USD is mixed across G10 - but outperformance in AUD, NZD currencies is noted. AUD/USD is through to a new weekly high at 0.6496 on continued equity strength - but the 50-dma remains out of reach for now at 0.6513. Equities in Europe are firmer, and US futures are also strong as markets look to reverse the weak daily close on Wall Street after the ISM services print.

- AUD/JPY continues to trade either side of the 200-dma, and a break above 96.17 is needed to make progress back toward the cycle high of 97.43 and a formal resumption of the broader uptrend.

- Tier one datapoints are few and far between Wednesday, with just Canadian final July PMI numbers and Weekly MBA mortgage applications due. Fed's Cook, Collins and Daly are on the schedule to speak today, and while none of them dissented at the most recent Fed meeting, markets will still be looking to gauge any signal on what could tip their vote to cut rates later this year.

- Possibly more importantly, President Trump is set to make an announcement at 2130BST/1630ET today, and while the President has yet to specify what topic this will cover, markets expect he could be covering a decision on Russian secondary sanctions, his nomination for the next Fed governor to replace Kugler or the appointee to lead the Bureau of Labor Statistics, after he fired the previous head of the department on Friday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBP: USD Bounce Has Major Pairs Testing Key Levels

Jul-07 09:05

- The USD's bounce Monday is providing some relief for the USD Index, which now sits 1% above last week's cycle lows to put the currency on a surer footing. As a result, the major pairs are seeing pressure toward the the post-NFP lows - with EUR/USD and GBP/USD challenging 1.1718 and 1.3586 respectively.

- Rates markets are endorsing USD gains here: the US curve is steeper as the global long-end continues to underperform. This backdrop, allied with any deterioration in trade relations between the US and the RoW remains a key market focus, particularly with the fluidity around Trump's approach to tariffs and the suite of reciprocal trade tariff deadlines looming over markets this summer.

- A correction lower through 1.3563 would be consequential for GBP/USD, and raise the likelihood of a test on the 50-dma support in the near-term. This level has held well and helped define the rally over the course of 2025 - crossing at 1.3477 today. In trend terms, we note that the 50-dma now trades with the largest % premium over the 200-dma since the bounce off lows in 2009. The premium currently sits at ~4.2% vs. the 2009 peak of ~8.2%, mid-Global Financial Crisis.

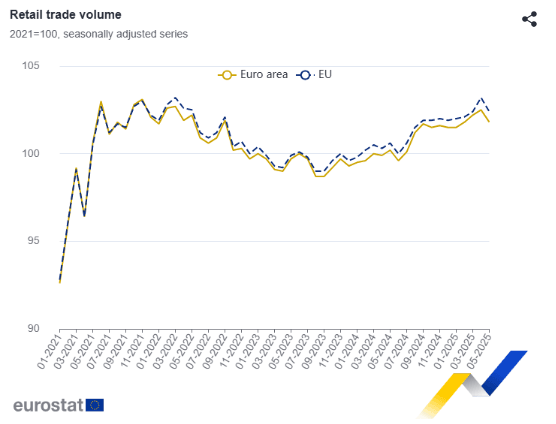

MNI: EUROZONE MAY RETAIL SALES -0.7% M/M, +1.8% Y/Y

Jul-07 09:00

- MNI: EUROZONE MAY RETAIL SALES -0.7% M/M, +1.8% Y/Y

EUROZONE DATA: May Retails Sales Weak As Expected, Non-Food & Fuel Carry Y/Y

Jul-07 09:00

Eurozone (real) retail sales were overall broadly in line with (weak) expectations in May on a sequential comparison, at -0.7% M/M (-0.6% M/M cons; +0.3% April, revised from +0.1%).

- Across sectors, all main categories fell: Food, drinks, tobacco -0.7% M/M, non-food products (except automotive fuel) -0.6%, automotive fuel -1.3% - neither of the categories has exhibited a clear directional trend YTD.

- Also across countries, May weakness appears quite broad-based, with Spain the strongest out of the "big 4" EZ countries at a mere 0.2% M/M.

- The overall Y/Y print was 1.8% in May, a bit firmer than consensus of 1.4% (2.7% Apr, revised from 2.3%). Across categories, previous trends prevail here: Non-food products and auto fuel tend to fare better than the food, drinks, tobacco category.

- Consumer confidence gives a rather weak outlook for retail sales in the Eurozone: "Consumer confidence remained broadly stable [on a, we would say, weak level of -14.8]. Although consumers were notably less pessimistic about the future general economic situation in their respective country, their intentions to make major purchases over the next 12 months dropped. Additionally, their perceptions of both their household’s past and expected financial situation deteriorated somewhat", the European Commission commented on the latest respective release.

- A June McKinsey study found that inflation remains consumers' main concern in the EU, although this has decreased compared with last year.