FOREX: USD Index at New YTD Highs, 1% Off Best Levels Since May'24

Jan-15 14:37

This data-tripped dollar rally has the price at new YTD highs, and through the Dec 9 highs. Should t...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Mar'26 2Y Sale

Dec-16 14:36

- -5,000 TUH6 104-11.5, post time bid at 0929:08ET, DV01 $199,000.

- The 2y contract trades 104-11.38 last (-.25)

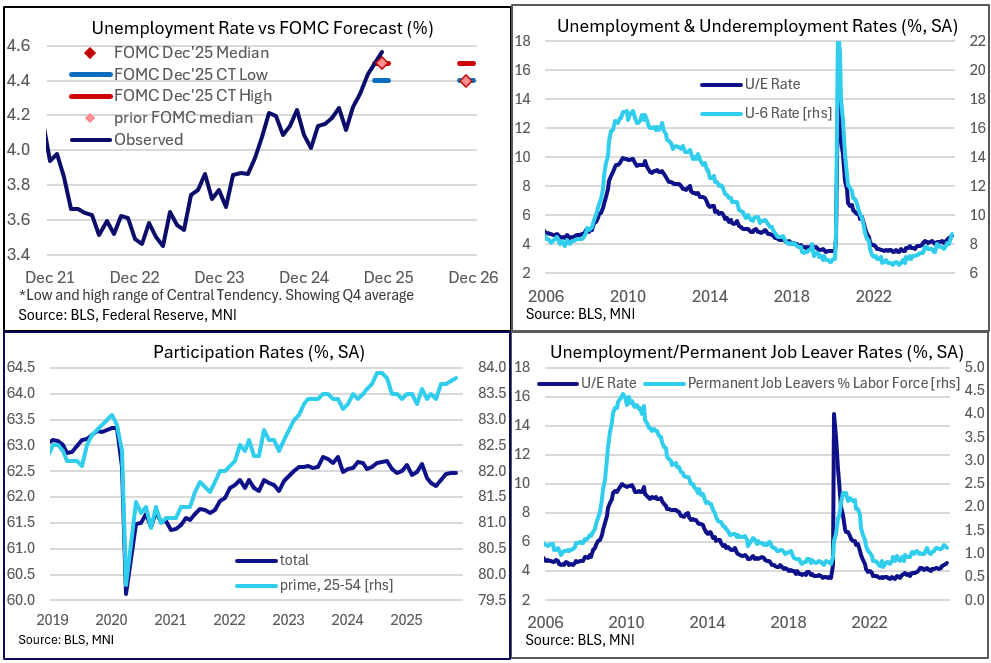

US DATA: Unemployment Rate Jump Driven By Prime Joblessness, But Caveats Abound

Dec-16 14:29

The rise in the unemployment rate to 4.56% unrounded in November from 4.44% in September represented a higher-than-expected reading and a fresh high for joblessness since September 2021. Analyst median consensus was 4.5%, with many more leaning toward 4.4% unrounded than 4.6% - and while the interpolated 0.06pp average monthly increase implies a slower pace of rises vs the preceding 3 months, this puts the U/E rate on track for an overshoot of the FOMC's 4.5% median expectation for Q4.

- Prime-age unemployment rate picked up to 3.91% (highest since Oct 2021) from 3.65% over the course of the two months, with the 0.26pp rise far outpacing the 0.12pp overall increase. And other signs of loosening, the U-6 underemployment rate jumped to 8.7% from 8.0%, easily the highest since August 2021, while the teenage unemployment soared 3.1pp to 16.3%, a post-August 2020 high. And employment grew by just 96k over 2 months, after rising an average 270k in each of September and August.

- However, there are many caveats to the above that imply some oddities in November's collection, above and beyond the late and longer survey period.

- The actual number of unemployed rose only 228k over the two months, an average of 114k which would be on the low side of the preceding 4 months' change.

- And this was driven too by re-entrants to the workforce: 293k over 2 months, a figure not seen since 2021, and arguably a sign of increased confidence in the labor market. In contrast, job leavers totaled only 34k (171k of which were due to temporary layoff, with -136k not on temporary layoff - both outsized numbers for these series and unclear whether affected by the federal shutdown). Permanent job losers fell, both in raw numbers and as a % rate of the workforce (1.13% from 1.18%).

- With participation ticking marginally higher to 62.47% from 62.45%, amid a 323k 2-month rise in the labor force, the overall unemployment rate was nudged higher. Prime-age participation increased 0.1pp to 83.8%, highest since September 2024. For 16-24 it jumped 0.4pp to 55.9%, highest since April (partly explaining the teenage unemployment jump), with 55+ dipping 0.2pp to 37.9% as part of a secular trend that brought it to the lowest level since 2006.

- Prime employment-population dipped to the lowest since July.

EGB FUNDING UPDATE: Spain 2026 Funding Plan Details

Dec-16 14:26

Spain 2026 Funding Plan Update

- The gross issuance target for MT/LT debt is E176.935bln (which is in line with the 2025 target of E176.514bln but E5bln above the E171.514bln expected outcome).

- Redemptions of MT/LT debt in 2026 total E126.935bln (around E5.4bln higher than in 2025). E3.643bln of this will be a repayment to the ESM.

- This leaves net MT/LT issuance at E50bln (2025 initial planned E55bln but revised down to E50bln).

- Gross issuance in 2025 was E171.305bln (net issuance E49.792bln).

- For each of 2023, 2024 and 2025 syndications have accounted for 20% of MT/LT issuance with 80% of issuance via auctions. There is no formal target for 2026, but will continue to be used for launches of "typically those with maturities of 10 years or more."

- Gross issuance of letras is forecast to increase E5.0bln to E108.742bln (it also increased E4.984bln in 2025).

- Spain is expected to receive E6.5bln of NGEU loans (in addition to the E15.934bln in 2025).

- "The Treasury plans to continue reopening the green bond issued in 2021 until its outstanding volume is comparable to that of other benchmark lines on the curve, ensuring adequate liquidity. The 2026 issuance volume will depend on the eligible expenditure identified by the Working Group for the Structuring of Sovereign Green Bond Issuances of the Kingdom of Spain and the Promotion of Sustainable Finance."

- "The Treasury may issue debt through private placements, in which securities are placed directly with a specific investor. These operations are undertaken at the investor’s initiative, routed through the Bonos and Obligaciones Primary Dealers, and will be carried out only on an exceptional basis when they contribute to iversifying

the investor base, reducing the public debt interest burden, and supporting the Treasury’s broader strategic objectives."