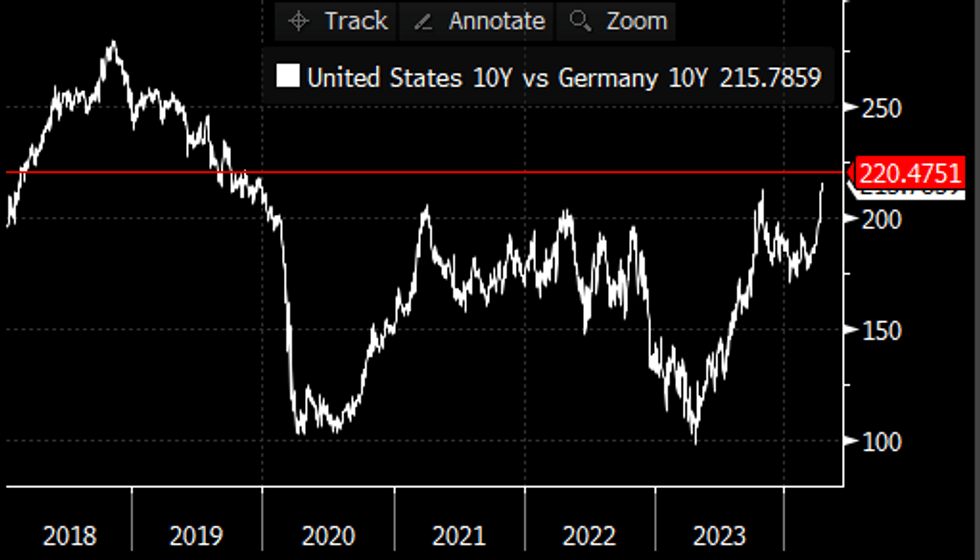

BONDS: US vs Germany widest since December 2019

Apr-12 09:41

- Bund is taking another leg higher and an extension to 132.79 would represent a full US CPI reversal, although the contract did print a 132.86 on that day (Wednesday).

- US Tnote is so far fairly unmoved, as desks favours for the ECB to be the first in cutting their rates.

- TYM4 would require a test all the way to 109.22+ to unwind the US CPI sell off.

- Price action in Futures means that the Tnotes/Bund is seeing further widening, by another 3.4bps today.

- The spread is now at its widest level since December 2019, and the next upside resistance will be seen at 220.5bps, the November 2019 high, and the widest print since early October 2019.

Chart source: MNI/Bloomberg.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: A Touch Firmer As Dovish ECB Speak Weighed Against Heavy Supply

Mar-13 09:41

Core/semi core EGBs have pared early gains but still sit firmer on the day, as markets weigh up heavy supply with this morning's ECB speak.

- Governing Council members Wunsch (after hours Tuesday) and Kazaks (this morning) came across dovish vs their usual leanings, with comments consistent with other recent ECB hawks regarding a potential cut in June.

- Those comments come against a backdrop of heavy morning supply: 3/7/15-year BTPs (and a BTP Green), 10-year Bund, 7/20-year Portuguese OTs, and a Slovenian 10-year syndicated tap.

- Bunds are +17 ticks at 133.30, still almost 100 ticks shy of Friday's post US labour report high. Futures remain in a short-term uptrend and the latest pullback is considered corrective.

- German and French cash yields are 1 to 2bps lower on the day, while 10-year periphery spreads to Bunds are a touch tighter with the exception of Greece. The 10-year BTP/Bund spread sits comfortably below 130bps, currently 1.1bps tighter at 126.8bps.

- The ECB is set to reveal the outcome of its operational framework review later today. See our preview here.

- The regional calendar is otherwise light, with comments from the ECB's Cipollone (1145GMT/1245CET) and Stournaras (1400GMT) scheduled.

US TSYS: Light Bear Flattening In Tight Ranges, 30-Year Supply Due Later

Mar-13 09:41

The modest Tsy rally that came alongside an early London EGB rally has faded.

- EGBs are off session highs and gilts are under some light pressure.

- TYM4 last unchanged at 111-05+, in a narrow 111-04+ to 111-10+ range.

- Tsy yields are little changed to 1.5bp higher with the curve bear flattening.

- FOMC-dated OIS shows ~81bp of ’24 cuts, with yesterday’s post-CPI move extending a little.

- ~19bp of cuts are priced through June.

- 30-Year Tsy supply headlines the U.S. schedule today. That comes after weaker demand at yesterday’s 10-Year auction & Monday’s well-received 3-Year offering.

- The pre-FOMC Fedspeak blackout period continues.

GILTS: A Little Softer After Early Rally Fades, Syndication Eyed

Mar-13 09:32

Gilt futures are now lower on the day, with wider core global FI also off session highs.

- The launch of the New 1.25% Nov-54 I/L gilt will be adding some weight.

- Futures last -19 at 99.61 (range 99.60-100.08).

- Monday’s low (99.37) provides intermediate support, with the bullish technical move stalling a little.

- Cash gilt yields are 0.5-2.0bp higher.

- Macro headline flow has been light since the early ECB speak.

- Largely in line domestic economic activity data didn’t impact markets.

- Yesterday’s labour market data was always going to be more important for markets and BoE policy.

- ~70bp of BoE cuts are priced through year end.

- SONIA futures are -1.5 to +1.5, off early highs alongside gilts.