OIL: US OIL: October 15 - Americas End of Day Oil Summary: Crude Lower

US OIL: October 15 - Americas End of Day Oil Summary: Crude Lower

WTI crude markets are lower today under pressure from demand concerns due to US-China trade tensions combined with rising global supplies. The IEA yesterday raised its forecast of a record surplus for next year amid rising OPEC+ and non-OPEC supplies. Crude stocks are seen higher in a Reuters survey.

- Crude time spreads yesterday extended the declining trend with both Brent and WTI Dec25-Dec26 spreads now in contango amid bearish market pressure.

- IEA has revised the expected oversupply for next year even higher, expected to be 4mb/d, driven by a rise in expected global supply growth, the October Oil Market Report showed.

- Global oil market balances are expected to average a surplus of 3m b/d until April 2026, according to Kpler.

- The UK has announced 90 new sanctions on Russia, including measures targeting Rosneft and Lukoil, four oil terminals in China, 44 tankers in the ‘shadow fleet’, Nayara Energy and the Beihai LNG terminal.

- US-China working-level trade talks occurred on Monday and China reiterated yesterday its right to control rare earth exports and that the US should negotiate.

- US Treasury Secretary Bessent today suggested a further tariff truce could be linked to China delaying measures on rare earth exports.

- MidEast to Asia VLCC freight rates surged to a two-week high on Monday and are expected to stay elevated due to the US-China port fees and concern for US sanction on China’s Rizhao port, Reuters sources said.

- A total of 641mbbls of open Nov25 WTI options positions on CME and ICE are currently due to expire on Oct. 16. Open interest is 361k call contracts and 281k for puts. NOV25 WTI options expire tomorrow.

- A Reuters poll found US crude oil inventories rose by about 300,000 barrels in the week to October 10.

- A bearish theme in WTI futures remains intact and Tuesday’s fresh cycle low reinforces current conditions. The move down last week resulted in a break of support at $60.40, the Oct 2 low. This highlights an extension of the bearish price sequence of lower lows and lower highs and the move down opens $57.50 next, the May 30 low. On the upside, key resistance is at $66.42, the Sep 29 high. First resistance is at $62.47, the 50-day EMA.

- Cracks are mixed as the market awaits day-delayed US inventory data, with API data due today and EIA data tomorrow. A Reuters survey found distillate inventories decreased by about 300,000 barrels last week, while gasoline stocks fell by about 100,000 barrels. Refinery utilization was estimated to be down 0.1% from 92.4% in the previous week.

- WTI Nov futures were down 0.7% at $58.27

- WTI Dec futures were down 0.7% at $57.87

- RBOB Nov futures were up 0.4% at $1.83

- ULSD Nov futures were down 1% at $2.17

- US gasoline crack up 0.6$/bbl at 18.79$/bbl

- US ULSD crack down 0.8$/bbl at 33.04/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Bullish Extension

- RES 4: 1.3753 High Jul 2

- RES 3: 1.3681 High Jul 4

- RES 2: 1.3636 76.4% retracement of the Jul 1 - Aug 1 downleg

- RES 1: 1.3620 High Sep 15

- PRICE: 1.3605 @ 19:30 BST Sep 15

- SUP 1: 1.3475/3333 50-day EMA / Low Sep 3

- SUP 2: 1.3315 61.8% retracement of the Aug 1 - 14 bull leg

- SUP 3: 1.3249 76.4% retracement of the Aug 1 - 14 bull leg

- SUP 4: 1.3142 Low Aug 1 and a key support

A bullish theme in GBPUSD remains intact and price traded higher Monday. The pair has pierced resistance at 1.3595, the Aug 14 high and a bull trigger. A clear break of it would strengthen bullish conditions and open 1.3636, a Fibonacci projection. Initial support to watch is 1.3475, the 50-day EMA. A clear breach of the EMA would highlight a potential reversal and signal scope for a deeper retracement.

US 10YR FUTURE TECHS: (Z5) Bullish Trend Sequence

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-07 1.0% 10-dma envelope

- RES 2: 114-00 Round number resistance

- RES 1: 113-29 High Sep 5

- PRICE: 113-15 @ 19:11 BST Sep 15

- SUP 1: 112-23+ 20-day EMA

- SUP 2: 112-02 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

Treasury futures rallied to a fresh cycle high last Thursday, strengthening current bullish conditions. Note that the recent impulsive rally highlights an acceleration of the uptrend. Also, moving average studies are in a bull-mode position, highlighting a dominant uptrend. This suggests scope for an extension through 114-00 next and a test of 114-10, the Apr 7 high (cont). Initial firm support to watch is 112-23+, the 20-day EMA.

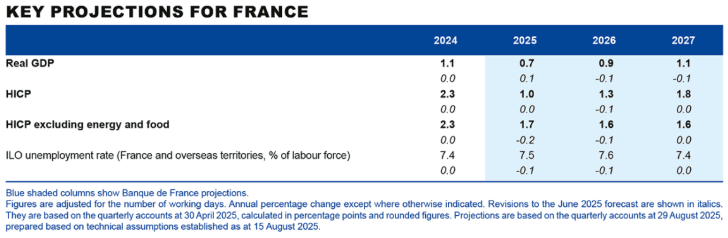

FRANCE: Bank of France Trims GDP Growth Forecasts

The Bank of France downgraded its real GDP growth forecasts on domestic business uncertainty and unfavourable assumptions whilst also warning that less fiscal consolidation might not lead to additional growth. Core inflation forecasts are also on net trimmed, seen below the ECB's 2% target throughout the forecast horizon. Full report here.

- The Bank of France has trimmed its real GDP forecasts for 2026 and 2027 by 0.1pp to 0.9% in 2026 and 1.1% in 2027, "attributable to the more uncertain domestic business environment and more unfavourable assumptions concerning the international environment, notably due to a higher euro exchange rate and oil price, as well as weaker external demand."

- With 2025 real growth nudged up a tenth to 0.7% for 2025, it eyes a very steady improvement ahead.

- "As wage growth outpaces price increases, the annual growth in the purchasing power of wages of approximately 1% should underpin a recovery in household consumption."

- Within the report, core inflation (HICP ex energy & food) is mostly revised lower with 1.7% in 2025 (-0.2pp), 1.6% in 2026 (-0.1pp) and 1.6% in 2027 (unch). That lack of 2027 downward revision goes against last week's ECB 0.1pt downward revision to 1.8% in 2027 for the Eurozone as a whole. The latter was part of the headline inflation revision to 1.9% which Lagarde downplayed as a "big" 1.9%. Of course, the France forecast is already more dovish.

- That said, despite dovish growth and inflation forecasts, there are some mildly hawkish tweaks to the unemployment rate. It's seen at 7.5% in 2025 (-0.1pp), 7.6% in 2026 (-0.1pp) and 7.4% in 2027 (unch).

- Bloomberg quotes Villeroy as saying France should keep targeting a 3% GDP fiscal deficit in 2029 and that the ex-PMs budget plan can be improved on tax fairness.

Fiscal assumptions behind the projections: "in a more uncertain national context following the vote of no confidence in the French government, the projections are based on an unchanged fiscal policy assumption compared to June, which would result in a deficit of 5.4% of GDP in 2025, and a primary structural adjustment of 0.6% of GDP in 2026 and 0.4% in 2027. Less fiscal consolidation should not however lead to additional growth, as the prolonged fiscal uncertainty could lead to a more wait-and-see attitude on the part of households and businesses."