OIL: US OIL: January 5 - Americas End of Day Oil Summary: Crude Higher

US OIL: January 5 - Americas End of Day Oil Summary: Crude Higher

WTI Crude prices ended higher amid uncertainty over Venezuela’s crude output and heightened geopolitical risk after the US captured President Maduro over the weekend. While it may take years for Venezuelan oil infrastructure to be repaired to good order should foreign oil majors decide to return, there could be some short-term downside to oil prices if cargoes destined for China are redirected toward US ports.

- Venezuela’s oil producing region appears to have seen minimal impact from the weekend’s events, though PDVSA has begun cutting crude production as it runs out of storage due to the US blockade.

- At least 16 oil tankers hit by U.S. sanctions appear to have made an attempt to evade a major American naval blockade on Venezuela’s energy exports over the last two days the NY Times reports.

- Bloomberg reports US Energy Secretary Chris Wright will meet this week with oil-industry executives about reviving Venezuela’s energy sector at the Goldman Sachs Energy, Clean Tech & Utilities Conference in Miami where executives from Chevron, ConocoPhillips and other companies are scheduled to attend.

- Venezuela’s oil industry needs significant investment after an extended period of neglect which will be a long process and so there is unlikely to be an increase in Venezuelan oil exacerbating the 2026 market surplus.

- US intervention in Venezuela will likely choke oil flows to China, though the short-term impact will be softened by large volumes of sanctioned crude stored at sea, Bloomberg reports.

- On Sunday, OPEC as expected decided to stick to the plan for unchanged output quotas in Q1. The next meeting is scheduled for Feb. 1.

- The US could raise tariffs on India if it does not meet Washington’s demand to curb purchases of Russian oil, President Trump said on Sunday, cited by Reuters.

- Observed crude exports from Saudi Arabia rose in December to 6.9m b/d, the highest since April 2023, according to Bloomberg.

- Morgan Stanley expects global oil supply to peak in mid-2026 and has cut its Brent forecasts for Q1, Q2 and Q3 with a low at $55/bbl in Q2, according to Bloomberg.

- UBS forecasts Brent to stand at $62/bbl at the end of Q1, $65/bbl at mid-year, and $67/bbl at year-end.

- Saudi Aramco has set the February Arab Light crude oil official selling price to Asia at $0.30/bbl above the Oman/Dubai average, down from the previous month when the premium was $0.60/bbl.

- P66’s 139k b/d Wilmington, California refinery will have a planned flare event January 6 to February 1 per a South Coast Air Quality Management District filing.

- Cracks are relatively steady overall, though diesel cracks are edging higher as the market assesses the near-term risk to Venezuelan flows after the US captured President Maduro over the weekend.

- WTI Feb futures were up 1.7% at $58.32

- WTI Mar futures were up 1.7% at $58.07

- RBOB Feb futures were up 1.3% at $1.72

- ULSD Feb futures were up 1.3% at $2.14

- US gasoline crack down 0.1$/bbl at 13.96$/bbl

- US ULSD crack up 0.1$/bbl at 31.64/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Bull Channel Breakout

- RES 4: 1.4140 High Nov 5 and a key resistance

- RES 3: 1.4131 High Nov 21

- RES 2: 1.4051 High Nov 28

- RES 1: 1.3939/4016 Low Nov 28 / 20-day EMA

- PRICE: 1.3865 @ 16:35 GMT Dec 5

- SUP 1: 1.3853 Intraday low

- SUP 2: 1.3840 50.0% retracement of the Jun 16 - Nov 6 bull cycle

- SUP 3: 1.3812 Low Sep 23

- SUP 4: 1.3779 Low Sep 22

A bear theme in USDCAD remains intact and Friday’s strong sell-off reinforces a bear theme. The pair has breached an important support at 1.3942, the base of a bull channel drawn from the Jul 23 low. The break highlights a stronger bear cycle and signals scope for an extension towards 1.3840 next, a Fibonacci retracement point. Initial firm resistance to watch is 1.4016, 20-day EMA.

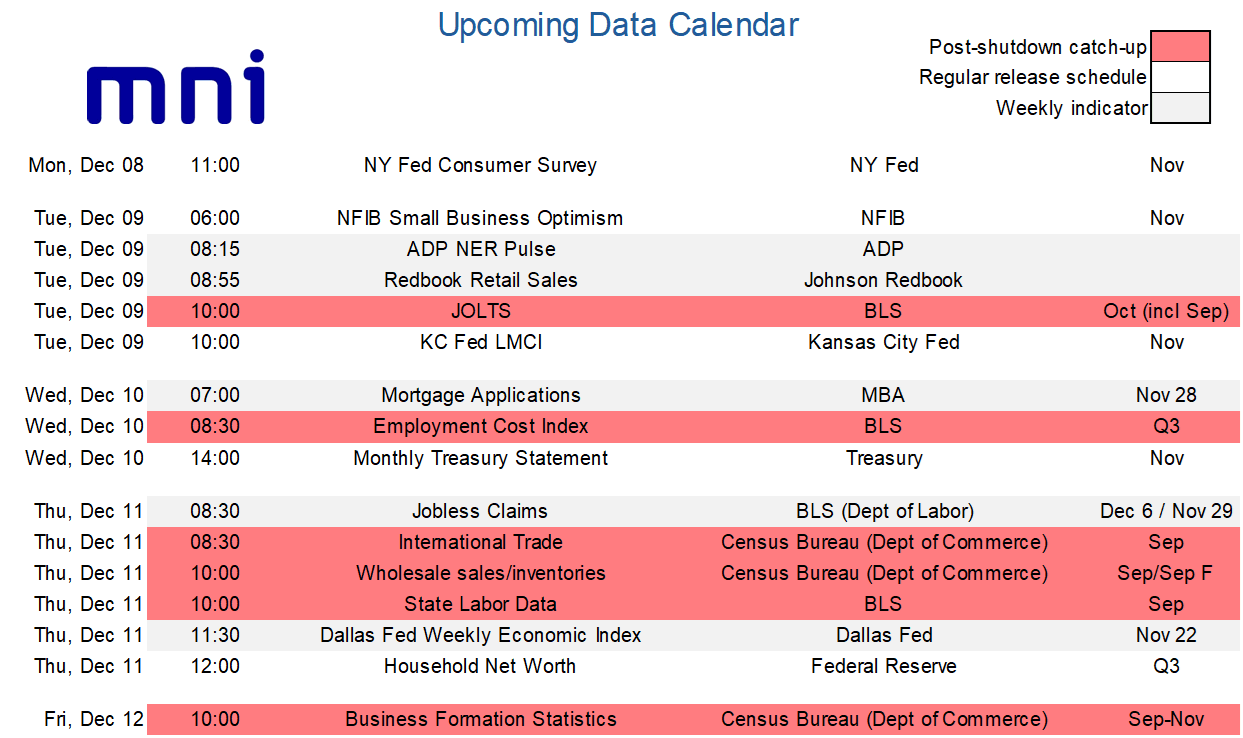

LOOK AHEAD: US Week Ahead: FOMC Decision Dominates, Post Shutdown Data Catch-Up

- Next week’s US calendar is dominated by the FOMC decision on Wednesday, with a third consecutive 25bp cut almost fully priced.

- Expect it to be a contentious meeting however, with many arguing for a pause not least whilst they’re still relatively in the dark on key official data releases following the government shutdown.

- Fed Chair Powell opted for a surprisingly hawkish tone at the late October press conference, highlighting a deeply divided committee on prospects for another cut in December.

- The “fog” had appeared to win out until NY Fed’s Williams, a senior permanent voter, gave unusually explicit guidance on still seeing room “for a further adjustment in the near term”. With no pushback from FOMC members or media briefings, it appears this message has approval from the core of the FOMC which should be enough to see a rate cut this month. The likely catalyst was the further increase in the unemployment rate to 4.44% back in September, although subsequent tracking suggests stabilization and jobless claims data don’t show any signs of deterioration.

- We’ll be looking for the number of hawkish dissents (we’d be surprised if anyone joins Miran dissenting for a 50bp cut) and expect a greater number to object to a cut in the 2025 dot plot, whilst the distribution of dots for 2026 should be in greater focus.

- As for the economic projections, we expect upward revisions to GDP growth but downward revisions to near-term core PCE inflation with tariff passthrough proving less severe than previously feared.

Aside from the Fed, we also receive two months worth of JOLTS data along with other delayed releases as the shutdown data backlog is slowly caught up.

AUDUSD TECHS: Bullish Impulsive Wave Extends

- RES 4: 0.6723 High Oct 21 ‘24

- RES 3: 0.6707 High Sep 17 and a key resistance

- RES 2: 0.6660 High Sep 18

- RES 1: 0.6649 Intraday high

- PRICE: 0.6630 @ 16:32 GMT Dec 5

- SUP 1: 0.6580/6533 High Nov 13 / 20-day EMA

- SUP 2: 0.6517 Low Nov 27

- SUP 3: 0.6466/21 Low Nov 26 / 21

- SUP 4: 0.6415 Low Aug 21 / 22 and a bear trigger

A strong impulsive bull wave in AUDUSD remains intact, having printed 10 consecutive sessions of higher highs. Recent gains have cleared a number of important short-term resistance points, strengthening a bull theme and highlighting scope for a continuation higher. Today’s rally has resulted in a breach of 0.6640, 76.4% of the Sep 17 - Nov 21 bear leg. This opens 0.6707, the Sep 17 high and key resistance. Key support to watch is at 0.6533, 20-day EMA.