AMERICAS OIL: US OIL: January 16 - Americas End of Day Oil Summary: Crude Rises

Jan-16 19:34

US OIL: January 16 - Americas End of Day Oil Summary: Crude Rises

WTI Crude prices ended higher after the pull back from a high on Jan 14. The market is weighing geopolitical risk in Iran amid a buildup of US forces in the region against oversupply risks. US economic fundamentals remain net positive.

- The US total oil and gas rig count was down 1 rig on the week at 543 rigs, according to Baker Hughes. This puts total US oil and gas rigs down 37, or 6.4% on the year.

- Oil: 410 (1) - down 68 rigs, or 14.2% on the year.

- Axios reports that Israeli officials think that despite the delay, a U.S. military strike could take place in the coming days. Adds, "The U.S. military is sending additional defensive and offensive capabilities to the region to be ready in case Trump orders a strike, U.S. sources say."

- There is no shortage of Iranian oil in the market, with Iranian crude in transit conservatively estimated at around 80m bbl, Platts said.

- Trafigura is preparing to discharge its first cargo of Merey 16 oil at the Bullen Bay terminal in Curacao to store oil for possible future distribution to international markets.

- Venezuela acting President Rodríguez presented a reform to the nation’s hydrocarbons law to create two funds for dollar investment funds from oil sales.

- A Republican proposal aims to replenish the US Strategic Petroleum Reserve (SPR) with discounted Venezuelan crude, but the SPR cannot accommodate such heavy grades of oil, according to Energy Intelligence.

- US involvement in Venezuela could lower regional risk and indirectly benefit Guyana’s booming offshore oil sector, rooted in the long-running Essequibo territorial dispute, Platts said.

- WTI hovering below $60/b mark is beginning to hit investment, rather than just sentiment, Bloomberg said. Production can hold up in the short term, as much shale remains viable around $50/b. The real impact is on future supply, through fewer rigs, delayed well completions and a gradual pullback in capital spending.

- The 166k b/d PBF Torrance refinery had an unplanned flare event on Jan. 16, according to Bloomberg. The refinery produces approximately 1.8b gal of gasoline per year, which represents ~10% of the gasoline demand in California.

- Cracks are mixed as the market watches geopolitical risks in Iran amid signs of a buildup in US military presence.

- WTI Feb futures were up 0.4% at $59.44

- WTI Mar futures were up 0.4% at $59.30

- RBOB Feb futures were up 0% at $1.79

- ULSD Feb futures were up 1.2% at $2.24

- US gasoline crack down 0.2$/bbl at 15.49$/bbl

- US ULSD crack up 0.9$/bbl at 34.50/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDJPY TECHS: Support At The 50-Day EMA Remains Intact

Dec-17 2025 19:30

- RES 4: 158.87 High Jan 10 and a key resistance

- RES 3: 158.29 2.618 projection of the Sep 17 - 26 - Oct 1 price swing

- RES 2: 158.00 Round number resistance

- RES 1: 156.95/157.89 High Dec 9 / High Nov 20 and bull trigger

- PRICE: 155.50 @ 16:33 GMT Dec 17

- SUP 1: 154.03 50-day EMA

- SUP 2: 153.62 Low Nov 14

- SUP 3: 152.82 Low Nov 7

- SUP 4: 151.54 Low Oct 29

The latest pullback in USDJPY appears corrective. The trend condition remains bullish and this is highlighted by moving average studies that are in a bull-mode position. Support to watch lies at 154.03, the 50-day EMA. A clear breach of this average would undermine the bull theme and signal scope for a deeper corrective pullback. For bulls, a resumption of gains would open 158.00.

US STOCKS: Late Equities Roundup: IT, Communication Services, Industrials Lag

Dec-17 2025 19:26

- Stocks extend lows late Wednesday - the Nasdaq leading the decline as longs took profits ahead of the Christmas & New Years holidays. Currently, the DJIA trades down 153.34 points (-0.32%) at 47956.34, S&P E-Mini Futures down 65.75 points (-0.96%) at 6791, Nasdaq down 339.6 points (-1.5%) at 22771.63.

- Information Technology, Communication Services and Industrials sector shares continued to lead declines in the second half: Lam Research -5.10%, Oracle -5.04%, Broadcom -4.95%, Advanced Micro Devices -4.86%, Super Micro Computer -4.71%, Palantir Technologies -4.64%, Western Digital -4.51% and Dell Technologies -4.27%.

- Merger/acquisitions continued to make headlines as Paramount Skydance trade down -4.08% after Jared Kushner's private equity firm pulled out of the hostile takeover bid for Warner Brothers, the latter also down 2.04%. Warner executives implored investors to reject the $108B Paramount bid, calling it "illusory" in favor of Netflix's superior offer.

- GE Vernova -8.80%, Quanta Services -5.55%, EMCOR Group -4.84%, Generac Holdings -4.78%, Caterpillar -4.77% and Eaton Corp -4.68% weighed on the Industrials sector.

- On the positive side, Energy and Consumer Staples sector shares outperformed in the first half:

- Texas Pacific Land +6.05% after signing an agreement with Bolt Data to build data centers, followed by: ConocoPhillips +3.96%, Devon Energy +3.85%, Occidental Petroleum +3.37%, Targa Resources +2.60% and Diamondback Energy +1.94%.

- Meanwhile, General Mills +2.87%, Church & Dwight Co +2.64%, Kroger +2.38%, Clorox +1.99%, Procter & Gamble +1.88% and Hormel Foods +1.48% buoyed the Consumer Staples sector in the first half.

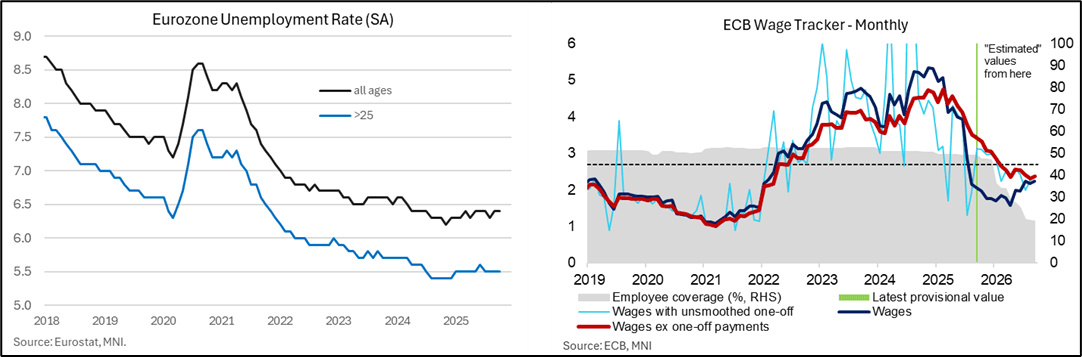

ECB: Macro Since Last ECB - Labour: U/E Rate Higher After Latest Upward Revision

Dec-17 2025 19:25

- The Eurozone unemployment rate was higher than expected in October at 6.4% in the single monthly update since the October meeting, unchanged after an upward revised 6.4% September (initially 6.3%).

- Revisions have been a theme over the past year, and generally to the upside, with this year’s low currently seen at 6.3% in multiple months vs an initially reported 6.1% in February for example.

- A 6.4% rate is still clearly historically low however, up from the series low of 6.2% in Nov 2024 before broadly moving sideways since then.

- The unemployment rate for those aged 25 years and above tells a broadly similar story at 5.5% for a third consecutive month versus series lows of 5.4% through most of 2H24.

- Back to latest data, the level of unemployment was a little more encouraging as it decreased slightly by 13k after two monthly increases.

- Meanwhile, revisions to the ECB wage tracker, released as usual the Wednesday after the ECB decision, saw a marginal upward revision for negotiated wages ex one-off payments for 4Q25 from 3.13% to 3.15% Y/Y.

- New projections for 3Q26 point to this ex one-off payment metric easing to 2.37% Y/Y after a projected 2.49% Y/Y in 2Q26.

- The wage tracker has generally seen marginal upward revisions over time (note the case in the prior September update) although these projections should continue to give the ECB confidence that wage-driven inflationary pressures remain on a disinflationary trajectory.

- That was especially so after realized negotiated wages growth subsequently surprised lower in Q3 at 1.87% Y/Y vs consensus of 2.45%.

- However, this was more recently countered by the December national accounts update showing far stronger than expected compensation per employees growth of 4.0% Y/Y in Q3, unchanged from 4.0% in Q2 vs the ECB’s forecast of a moderation to 3.2%.