US LNG: US LNG Flows to LatAm Rebounded in Nov: Platts

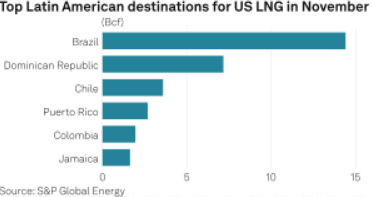

US LNG exports to Latin America and the Caribbean rebounded in November, rising nearly 17% from October to 31.42 Bcf, according to Platts.

- Shipments were also well above year-earlier levels, up 31% from November 2024 and almost 78% higher than in 2023.

- Exports reached six destinations — Brazil, the Dominican Republic, Chile, Colombia, Jamaica and Puerto Rico — up from five in October.

- Brazil remained the largest buyer for the fifth consecutive month, taking 14.41 Bcf, double October’s volume and far above levels seen in the past two years.

- Chile resumed imports with one cargo, while Puerto Rico’s intake fell sharply to 2.68 Bcf. Colombia and Jamaica each received one cargo.

- In total, ten US cargoes were shipped to the region, mostly supplied by Sabine Pass, Plaquemines and Freeport.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US ISM OCT SERVICES COMPOSITE INDEX 52.4

- MNI: US ISM OCT SERVICES COMPOSITE INDEX 52.4

- US ISM OCT SERVICES PRICES 70.0

US DATA: October Services PMI Trimmed In Final Print, Margin Compression Noted

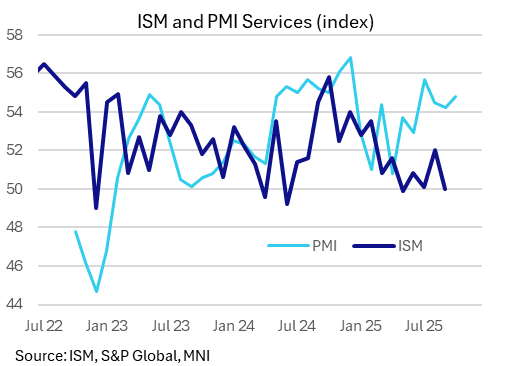

The S&P Global service PMI saw a reasonably large downward revision in the final October print although still firmed from September for still its highest since July. At 54.8, it’s still likely to show a much more optimistic business activity than the 50.8 expected for ISM services after its 50.0. Within the S&P Global survey, note growing margin compression in the comment below.

- S&P Global US services PMI: 54.8 in Oct final (cons & flash 55.2) after 54.2 in September

- S&P Global US composite PMI: 54.6 in Oct final (cons 54.9 & flash 54.8) after 53.9 in September

- PMI press release (link): "Latest PMI® survey data from S&P Global showed that the US service sector registered a solid and accelerated pace of activity growth during October."

- "Higher service sector output was accompanied by a firm rise in incoming new business, although an uncertain economic and political outlook reportedly meant that hiring growth was modest and confidence about the future fell to a six-month low."

- "Moreover, selling price inflation was limited by competitive pressures, dropping to its lowest level since April despite elevated cost pressures from tariffs and rising employee expenses."

- Further on margin compression from the S&P Global Chief Business Econ: "However, there are signs that new business is coming at the cost of service providers having to soak up continued high input price growth to remain competitive. Customers are often pushing back on price rises, especially in consumer-facing markets. While good news in terms of inflation, this lack of pricing power hints at weak underlying demand and lower profits."

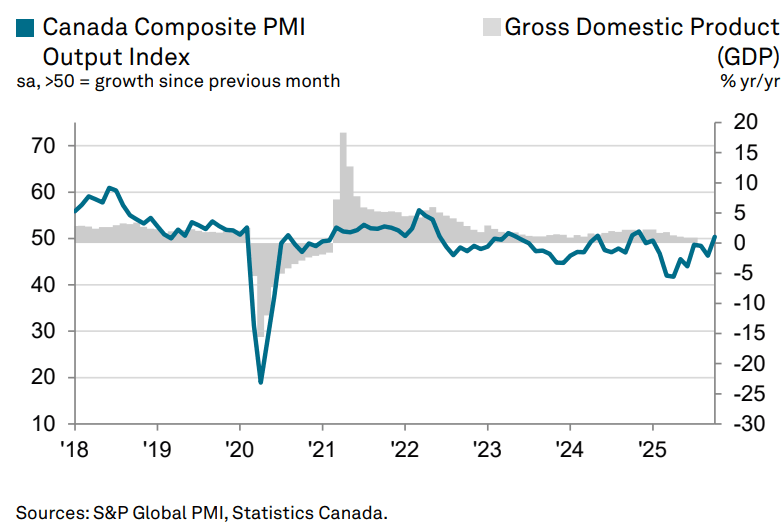

CANADA DATA: PMI Indicates Return To Expansion For Services, But Outlook Flat

Canadian Services PMI jumped in October to 50.5 from 46.3 prior, an 11-month high. It's the first above-50 reading since November 2024 and the 3rd highest reading in the last 29 months.

- The report itself isn't so enthusiastic about the significance of this development however: "Whilst a noticeable improvement on the severe declines seen earlier in the year, growth was nonetheless marginal as some hesitancy and uncertainty amongst clients continued to weigh on new business volumes.

- And services employment appeared to be negative: "Staffing levels also fell as firms generally chose not to replace any leavers and confidence remained below trend." That's the second consecutive month of employment contraction.

- Meanwhile businesses didn't appear to be able to pass through price increases, suggestive of soft demand: "Latest prices data showed another round of steeply rising operating expenses, although competitive pressures meant the degree of cost pass through to clients remained relatively subdued. "

- While Manufacturing remained in contraction in October, at 49.6 it was enough to nudge the Composite reading above 50.0 also for the first time since November 2024 (prior was 46.3). That's largely consistent with a positive GDP reading though at best at a very flat rate.

- Additionally while private sector output may have risen in Octoberm "Activity growth was however not accompanied by an

increase in new orders, which fell modestly in October whilst there was a further drop in employment. Backlogs of work

declined steeply whilst confidence in the outlook was again below trend."