OIL: US Jet Fuel Stocks Fell by 911k bbl in Week to Dec. 26: EIA

US Jet Fuel Stocks Fell by 911k bbl in Week to Dec. 26: EIA

- EIA data showed US jet fuel stocks drew by 911k bbl to 43.98m bbl in the seven days to Dec. 26, a 2% fall week-on-week.

- PADD 1 stocks were down 359k bbl, or 3.73% to 9.266m bbl,

- In PADD 3, the USGC refining hub, stocks were up 769k bbl, or 5.4% to 15.006m bbl,

- On the USWC (PADD 5), stocks were down 825k bbl, or 6.8% to 11.302m bbl,

- Four-week average jet demand rose by 0.89% to 1.705m b/d. Meanwhile, weekly demand was up by14.75% to 1.774m b/d.

- When looking at the average of 2019-2024 and excluding the pandemic year of 2020, current four-week average demand for this period in 2025 is higher by 1.705m b/d.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Schatz downside Put Fly

DUF6 106.90/106.70/106.50p fly, bought for 4.5 in 2.5k.

GERMANY: CDU Young Group Reiterates Oppo. To Pension Reforms, Could Mean Defeat

The 'Young Group' of lawmakers within Chancellor Friedrich Merz's centre-right Christian Democratic Union (CDU) have once again come out in opposition to planned pension reforms, threatening the continuation of the 'grand coalition' between the CDU/CSU and the centre-left Social Democrats.

- A statement from the group of 18 younger CDU lawmakers who have opposed the reforms, suggesting that they create an unsustainable financial burden that will be borne by future generations, claimed that their position remains "unchanged". The coalition has 328 seats to the opposition's 302, meaning if the Young Group voted against the reforms, it would lead to the defeat of the gov't.

- However, the statement makes clear that "All freely elected members of parliament bear their own responsibility to the state," indicating that the group may not vote en masse, but each lawmaker will be able to make their own decision.

- The uneasy 'grand coalition' can afford to lose the support of 12 lawmakers. Thirteen defections would lead to a 315-315 tie, and in the Bundestag, tied votes are deemed to be a rejection of the motion.

- The CDU holds a parliamentary group meeting on 2 Dec, in which a vote will be taken, giving an indication of the threat posed to the pension reforms ahead of a Bundestag vote later in the week.

- Late last week, Merz claimed that a pledge to enact comprehensive pensions reform in 2026 had alleviated the risk of the current reforms being defeated, but it remains to be seen whether this holds true.

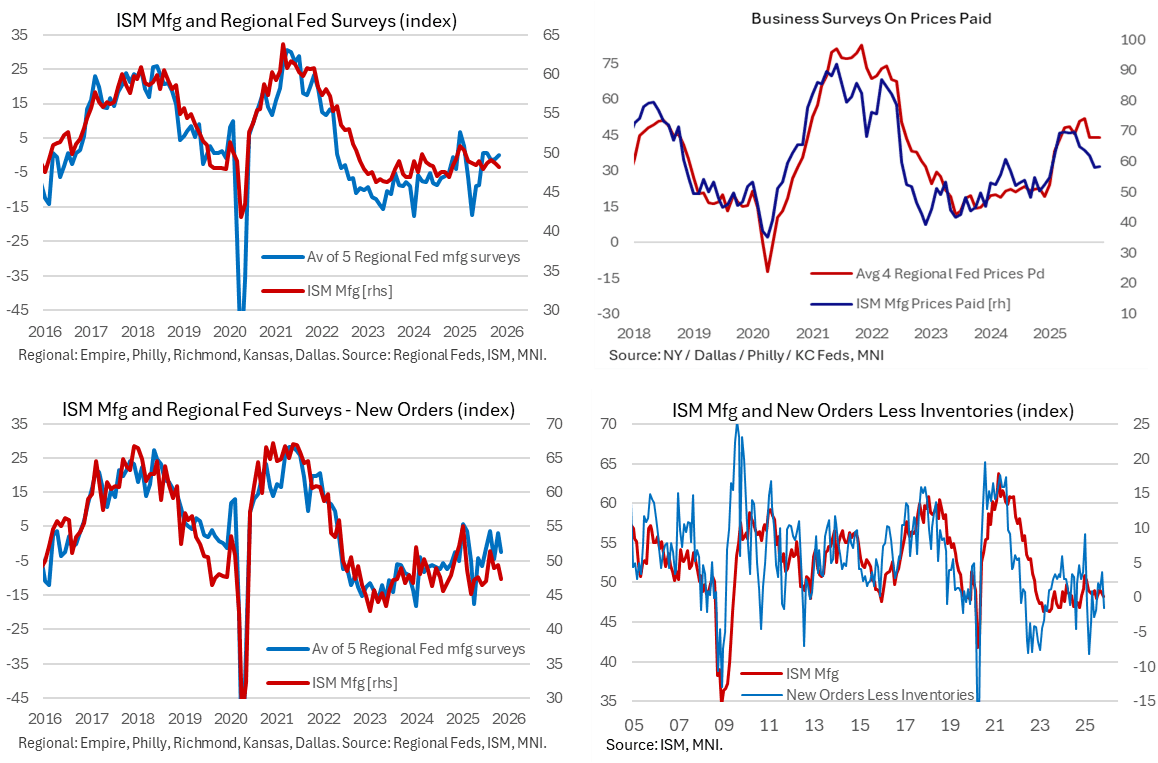

US DATA: ISM Mfg Back At Low End Of Recent Range, New Orders Slip Further

The ISM manufacturing survey for November saw its overall index surprise a little to the downside although it kept to narrow ranges and was within the range of outcomes implied by alternative indicators. We weren’t surprised by the latest weakness in new orders in a finding that points to further weakness more broadly ahead, although thought that prices paid might have seen a larger beat than they did.

- ISM manufacturing: 48.2 (cons 49.0) in November after 48.7 in October.

- Prices paid: 58.5 (cons 57.5, 7 responses) in Nov after 58.0 in Oct.

- New orders: 47.4 in Nov after 49.4 in Oct.

- Employment: 44.0 in Nov after 46.0 in Oct.

- The ISM manufacturing index was lower than expected in November as it fell 0.5pts to 48.2 vs expectations of some stabilization.

- It leaves it back at the low end a narrow range of 48.0-49.1 since March, having eased back from Jan and Feb seeing the first months above 50 (i.e. in expansionary territory) since late 2022 including a high of 50.9 in Jan.

- As noted earlier, alternative indicators had been mixed so this small miss shouldn’t be a notable surprise: regional Fed surveys had pointed to mild upside risk, the S&P Global US PMI suggested downside risk from a momentum perspective but was still much more optimistic in level terms, and the MNI Chicago PMI pointed to firm downside risk after it slid sharply last week.

- New orders weakness (-2pts to 47.4 for lowest since July) was less of a surprise to us with what had been more uniform downside risk. The MNI Chicago PMI again led the downside risk here, seeing its largest one-month decline since Sep 2023 in last week’s November survey.

- The downside of new orders falling and inventories rising firmly is that the new order less inventories metric fell from 3.6 to -1.5 for its lowest since July, pointing to further weakness in the overall index ahead.

- The employment index at 44.0 (-2pts) is its lowest since some depressed readings in Jul-Aug but makes up only ~10% of payrolled employment.

- On the pricing side, we’re actually a little surprised there wasn’t a larger beat here, as we’d flagged stronger relative levels for regional Fed surveys along with a strong bounce in the MNI Chicago PMI series. The S&P Global PMI had however noted manufacturing input price inflation cooled to the lowest since February in the flash release, a finding that looked to hold in the final survey released shortly ahead of the ISM report.