OIL: US Crude Stock Build Adds To Market’s Supply Worries

Oil prices were trending lower driven by ongoing concerns regarding the expected record 2026 surplus, but were then pushed down by the EIA report showing a substantial US crude inventory build last week, which added to these supply concerns. The product drawdowns were ignored for the most part signalling market sensitivity to signs of additional oil supply. The IEA’s updated monthly report is released 13 November.

- WTI fell 1.6% to $59.63/bbl, just off the intraday low of $59.52 and around support at $59.64. It reached $61.09 early in the European session. The benchmark is now 2.2% lower this week. The bear trigger is at $55.96.

- Brent was down 1.4% to $63.52/bbl to be off 1.9% this week. It made a high of $64.95 before falling to $63.44, holding just above initial support at $63.37. The bear trigger is at $59.97.

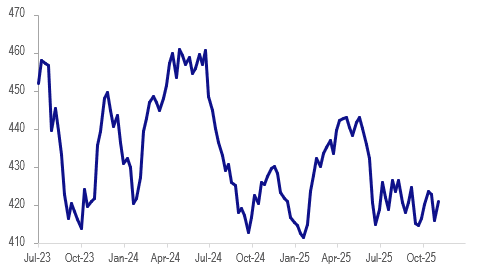

- The EIA reported a US crude oil inventory build of 5.2mn barrels last week after destocking of 6.86mnm keeping levels within the range they have been in since mid-year. Gasoline stocks fell 4.7mn barrels, and distillate was down 0.6mn, the fifth consecutive weekly decline for both suggesting demand remains solid.

- The 0.6pp decline in refining utilisation to 86%, 4.5pp below the same time last year, helped to drive the crude stock build and product drawdown. Seasonal maintenance has also contributed, according to Kpler.

EIA reported US crude inventories mln barrels

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (Z5) Southbound

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.685 - 1.000 proj of the Sep 3 - 12 - 15 price swing

- RES 1: 96.615 - High Sep 12

- PRICE: 96.395 @ 16:23 BST Oct 06

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Aussie 3-yr futures have traded lower and the contract has cleared the Sep 3 low of 96.435. A break of this level negates the recent short-term bullish theme. This breach signals scope for an extension towards 96.280, the May 15 low on the continuation chart. The short-term resistance to watch is 96.615, the Sep 12 high. Clearance of this level is required to reinstate a bullish theme.

AUD: AUD/USD - Drifts Higher With Risk & AUD/JPY

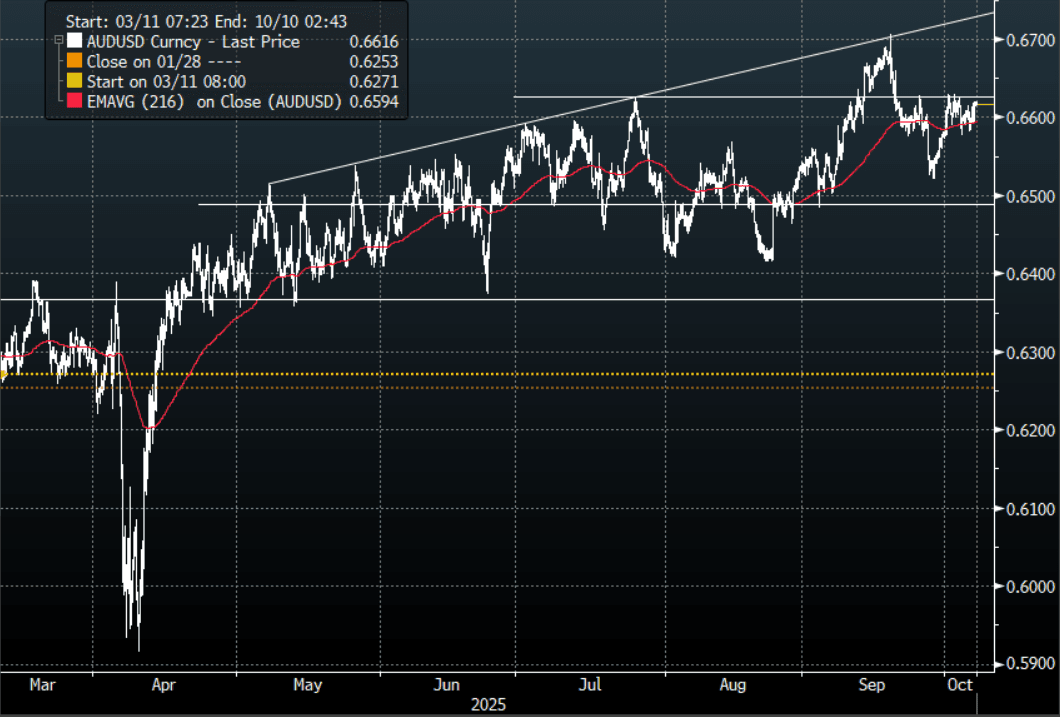

The AUD/USD had a range overnight of 0.6590-0.6620, Asia is trading around 0.6615. US stocks continue to shrug off global politics and the US shutdown, the USD though got a boost from the reaction in USD/JPY. The AUD drifted higher, helped by the way risk continues to push higher and probably some AUD/JPY demand as the JPY crosses surged. A move back through the 0.6625/50 area is needed to gain the momentum to have another look toward the pivotal 0.6700 area.

- Bloomberg - “Australian Rare Earths Stocks Climb on Trump Talks With Firms. A report claimed that US President Donald Trump’s administration was mulling a stake in Critical Minerals Corp., which hopes to develop a project in Greenland. It follows news last week that the Trump government was actively looking at ways to take equity stakes in Australian companies.”

- “Australia, New Zealand to Boost Efforts to Integrate Economies. Australia and New Zealand will fast-track work on a more ambitious Single Economic Market, the program that aims to integrate their economies and reduce barriers for business.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6735(AUD350m). Upcoming Close Strikes : 0.6300(AUD899m Oct 8 )- BBG

- Data/Event: Westpac Consumer Conf SA, ANZ-Indeed Job Advertisements MoM

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

RBNZ: RBNZ To Have New Financial Policy Committee To Ensure Stability

The RBNZ will have a new Financial Policy Committee (FPC) to be in place in early 2026. Its remit will include macro-prudential decisions (Debt-to-income, LTV ratio levels), financial institution’s prudential requirements and decisions related to financial stability.

- The goal of the new committee is to ensure the stability of NZ’s financial system through stronger decision making by engaging experts in the field.

- The RBNZ Board Chair and Governor will sit on the FPC with another 3 RBNZ Board members and up to 2 non-Board members or RBNZ employees.

- The decision to introduce the FPC was made with the Treasury and Minister of Finance following recommendations from the Finance and Expenditure Committee’s Inquiry into Banking Competition.