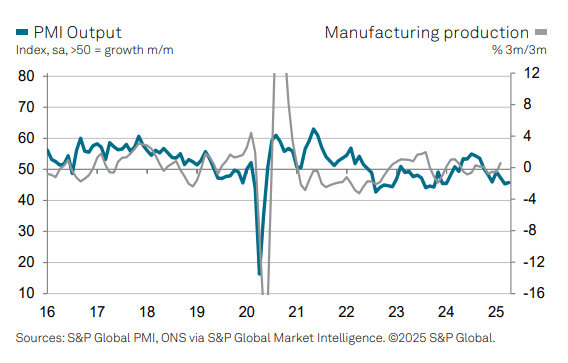

UK DATA: Upward Revision To April Manufacturing PMI; But Details Still Soft

May-01 08:38

Decent upward revision to the UK April manufacturing PMI, with he final read printing at 45.4 (vs 44.0 flash, 44.9 prior). It’s still the seventh consecutive month in contractionary territory, though.

- The broad themes of the report align with the flash release: Trade uncertainty is weighing on demand, particularly in export markets; Increased NIC and wage costs are dragging on employment; and Input price increases are being passed onto output prices.

- This data, alongside the services and composite PMIs next Tuesday, will set the scene for the BOE’s May decision. A 25bp rate cut is widely expected, with focus on updated projections and any tweaks to the statement guidance.

Key notes from the release:

- “Panellists reported that rising economic and trade uncertainties (including prospective US tariffs) had drained confidence from both consumer and business-to-business clients, resulting in an increased reluctance to commit to new contracts”

- “These factors also led to a comparatively large contraction of output and new work received at investment goods producers, suggesting that subdued market confidence was hitting demand for capital goods especially hard”.

- “New export orders fell at the quickest pace in almost five years, with demand from the US, Europe and mainland China all lower”

- “The tough current backdrop, rising cost pressures and increased uncertainty at manufacturers and their clients alike led to lower business optimism, reduced staff headcounts”

- “Manufacturing employment declined for the sixth month running in April. The rate of job losses accelerated and was the second-sharpest in almost five years”…” Many firms noted that lower staff headcounts were necessary to offset the impact of rising national insurance contributions, increased minimum wages”

- “April saw average purchases prices rise at the quickest pace since December 2022”…” Manufacturers passed on some of these cost increases to their clients, leading output price inflation to accelerate to a 26-month high”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RIKSBANK: Maintains FX Hedging Approach, Boosts USD Exposure

Apr-01 08:37

Riksbank's new FX strategic allocation importantly sees an unchanged approach to FX hedging - meaning the Riksbank remain in a "good balance" between contingency planning as well as risk and return.

- Their new FX allocation boosts USD exposure, drops EUR and NOK, maintains GBP and AUD: 70% USD (from 62%) EUR at 17.5% (from 22%), GBP unchanged at 5%, AUD unchanged at 5%, NOK at 2.5% (from 3%)

GERMAN AUCTION PREVIEW: 2.20% Mar-27 Schatz

Apr-01 08:36

This morning, Germany will hold its fourth Schatz auction of the year. On offer will be E4.5bln of the 2.20% Mar-27 Schatz.

- The E4.5bln size is in line with the last Schatz auction on March 11.

- Recent Schatz auctions have passed mostly smoothly, with solid bid-to-covers (in a 2.09x to 2.81x range since August), bid-to-offers (1.69x to 2.17x range since August) - the low prices were above the secondary market mid-prices throughout 2024/5 before the February 18 Schat auction saw them equal to each other, and then the low price was lower than the mid-price last time - both auctions appeared to have not seen an adverse market reaction, however.

- For the last Schatz auction on 11 March, the bid-to-cover stood at 2.37x, while the bid-to-offer came in at 1.84x.

- The next German auction will be tomorrow's E4.5bln of the 2.50% Feb-35 Bund (ISIN: DE000BU2Z049), while a new Jun-27 Schatz will be reopened next on April 22, for E5.0bln.

- Timing: Results will be available shortly after the bidding window closes at 10:30GMT / 11:30CET.

MNI: UK MAR FINAL MANUF PMI 44.9 (FLASH: 44.6); FEB 46.9

Apr-01 08:30

- MNI: UK MAR FINAL MANUF PMI 44.9 (FLASH: 44.6); FEB 46.9