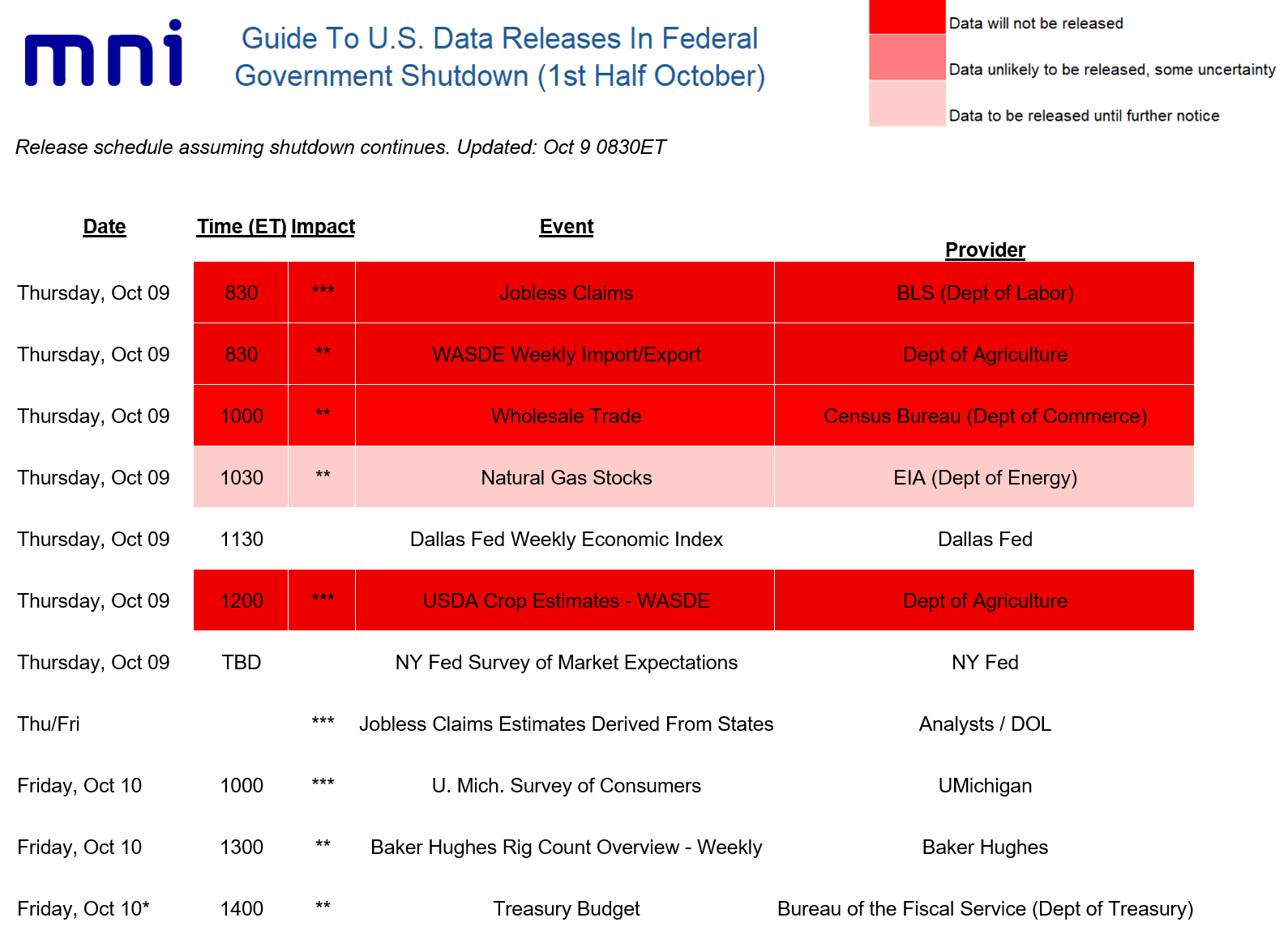

US DATA: Upcoming Data Guide: National Claims Data Off, But State-Level On

Oct-09 12:59

The weekly jobless claims report is postponed for a 2nd consecutive week due to the federal government shutdown, while wholesale trade data will also be postponed.

- However we will get some data. Indeed for jobless claims, individual state-by-state estimates should trickle in, which should allow for some rough estimates of the nation-wide figure to emerge from various analysts starting later Thursday and overnight. MNI will provide an estimate for initial (week of Oct 4) and continuing (week of Sep 27) claims by Friday morning. For last week's release, MNI estimated 223-225k initial claims (week of Sep 27) and 1,916k continuing (Sep 20 week).

- We will get the Dallas Fed's weekly economic index at around 1130ET (which helpfully compiles multiple weekly private sector indicators, and uses their own imputed estimate of jobless claims data so subject to revision later).

- Also today, we are tentatively expecting to get the NY Fed's latest Survey of Market Expectations, whose publication schedule lines up with the FOMC minutes (usually comes out a day later). This is most closely watched for forming consensus Fed balance sheet/QT expectations (it combines the former Survey of Primary Dealers and Survey of Market Participants) but also has several questions devoted to macro expectations.

- Arguably Friday's UMichigan preliminary October consumer sentiment survey could prove to be the week's most important single data release.

- A note on Friday's monthly Treasury budget report: this release date is always uncertain. Treasury releases this report on the 8th business day of the month, but this edition is the fiscal year-end report which they usually take a little more time to compile. In any event there is little suspense as the CBO estimate came out Wednesday: full-year FY2025 (Oct-Sep) deficit $1.809T - $8B smaller than the 2024 deficit of $1.817T.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US REDBOOK: SEP STORE SALES +6.6% V YR AGO MO

Sep-09 12:55

- MNI: US REDBOOK: SEP STORE SALES +6.6% V YR AGO MO

- US REDBOOK: STORE SALES +6.6% WK ENDED SEP 06 V YR AGO WK

FOREX: USD Trades with More Supportive Tone as Labour Market Revisions Awaited

Sep-09 12:53

- The greenback has been trading on a much firmer footing in early NY trade, with the DXY now pressing fresh session highs as we await the US preliminary annual payrolls benchmark revision, due at 1000ET.

- Volatility for the Japanese yen has placed the focus on USDJPY Tuesday, having traded to within 10 pips of the key short-term support at 146.21, the Aug 14 low. The pair now stands a solid 65 pips off the lows as higher US yields provide some stability following the hawkish BOJ driven move earlier in the session.

- The latest bout of dollar strength has been most notable for EURUSD, now down 0.3% on the day at 1.1730. Lingering French political risks will likely be dampening topside momentum for the single currency. Earlier we noted that Fitch may downgrade France’s sovereign rating to A+ on Friday after hours, following Bayrou’s unsurprising ousting as Prime Minister after yesterday’s no confidence vote.

- Short-term parameters for EURUSD appear well defined at 1.1829 (Jul 01 high and bull trigger) and 1.1625 (50-day EMA support).

EU-BOND SYNDICATION: 5/30-year dual-tranche: Allocations

Sep-09 12:49

5-year

- Spread set at MS + 22bp (guidance was MS + 24bps area)

- Tranche Size Set: E5bln

- Books closed in excess of E92bln (inc E4.5bln JLM interest)

- HR: 99% vs. 2.20% Oct-30 Bobl

- Maturity: 14 October 2030

- ISIN: EU000A4EG021

30-year

- Spread set at MS + 119bp (guidance was MS + 121bps area

- Tranche Size: E6bln (increased from E5bln, MNI had noted the potential to increase)

- Books closed in excess of E107bln (inc E6.85bln JLM interest)

- HR: 93% vs. 2.90% Aug-56 Bund

- Maturity: 12 October 2055

- ISIN: EU000A4EG039

For both:

- Settlement: 16 September 2025 (T+5)

- Coupon: Long first

- JLMs: Barclays / BofA / CACIB / LBBW / MS (B&D/DM)

- Timing: Hedge deadline 14:15BST / 15:15CET

From market source / MNI colour

Trending Top

Jun-26 16:22