GLOBAL MACRO: Underlying CPI Inflation Appears To Have Stabilised

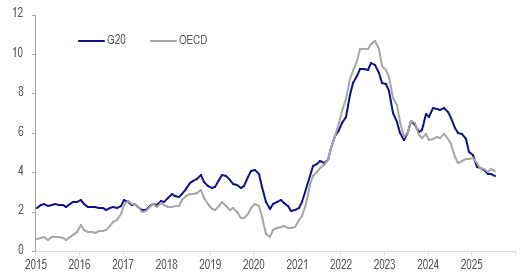

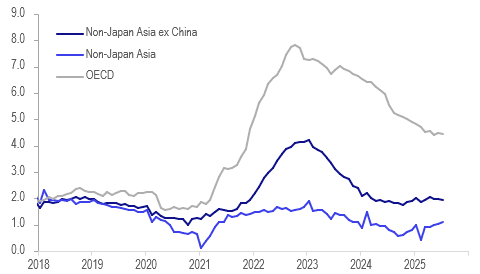

G20 inflation has been trending gradually lower over 2025 with it reaching 3.8% y/y in July, the lowest in over four years. However, both headline and underlying OECD inflation have been fairly stable since March with disinflation progress stalling. Non-Japan Asia ex China core has also been steady around 1.8-2% since the start of 2024. The impact of tariffs on inflation especially in the US remains highly uncertain but lower global demand could put downward pressure on prices.

Global headline CPI y/y%

Source: MNI - Market News/LSEG

- July OECD headline inflation moderated 0.1pp to 4.1%, while core was stable at 4.5%. They peaked at 10.7% y/y and 7.8% respectively in October 2022. August preliminary euro area CPI was steady around 2%.

- US August CPI prints on Thursday and is forecast to show core steady at 3.1% but headline picking up 0.2pp to 2.9%. The data will continue to be watched closely for tariff impacts.

- Non-Japan Asia ex China saw headline inflation moderate 0.3pp to 1.5% y/y in July, the lowest since our aggregate began in 2012. Core was 1.9% y/y down from 2.0% after it peaked at 4.2% in January 2023. China’s underlying inflation picked up 0.1pp to 0.8% in July, the highest in almost 18 months.

- August Asian releases to date saw lower headline and core inflation in Korea and Indonesia, while Taiwan and Thailand were little changed and the Philippines saw both rise.

Asia vs OECD core CPI y/y%

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (U5) Recovers With Treasuries

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.710 @ 14:34 BST Aug 8

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures received a boost from the US Treasury rally that followed a poor NFP print. This keeps Aussie 10-year futures toward the top end of the recent range. To the upside, next resistance is at 96.207, a Fibonacci retracement point. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

SECURITY: Trump To Sign Trilateral Peace Accord With Armenia/Azerbaijan Shortly

US President Donald Trump is shortly due to sign a trilateral peace agreement with Armenian Prime Minister Nikol Pashinyan and Azerbaijani President Ilham Aliyev at the White House. LIVESTREAM The event will provide another opportunity for Trump to style himself as peacemaker, after touting success in brokering peace deals between Rwanda/Congo, Cambodia/Thailand, and India/Pakistan.

- The accord aims to resolve a decade-long dispute over the sovereignty of Nagorno-Karabakh - a breakaway Azerbaijani province that was under de facto Armenian control from the dissolution of the Soviet Union until a 2020 war.

- Trump described the meeting on Truth Social as a “historic peace summit,” noting that the US will also sign “Bilateral Agreements [to] fully unlock the potential of the South Caucasus Region.”

- White House spokeswoman Anna Kelly told reporters that Trump would sign deals with both Armenia and Azerbaijan on energy, technology, economic cooperation, border security, infrastructure and trade.

- A White House official said: "It's about the entire region, and [the leaders] know that that region is known to be safer and more prosperous with President Trump."

- Reuters reports that the US will have development rights to build transportation links in the strategic Zangezur Corridor, a mountainous stretch of Armenian territory between Azerbaijan and its Nakhichevan exclave.

- Politico notes: “But whether this is just a photo opportunity or a lasting end to a conflict that has undermined stability in a region dominated by Russia and Iran will depend on whether the US can address several key challenges.”

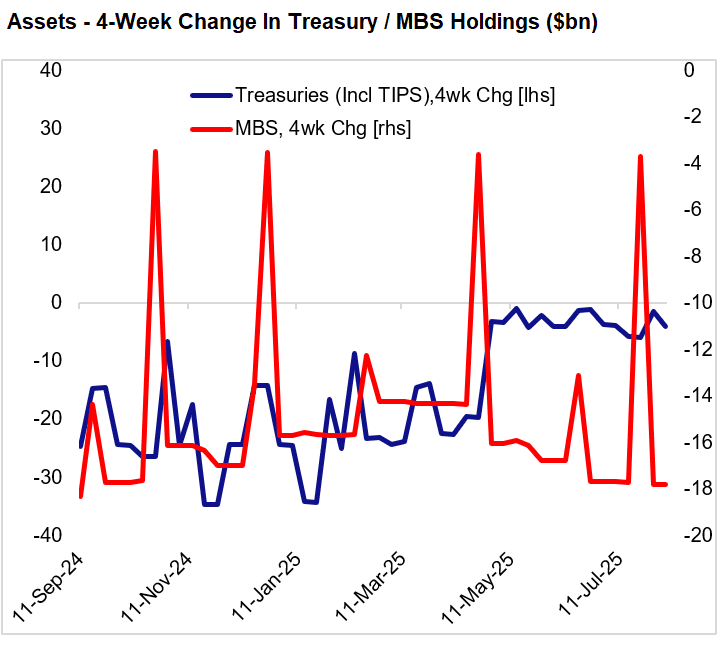

FED: Balance Sheet Runoff Continues At Steady $20B/Month Pace (2/2)

Fed asset holdings were little changed in the past week. SOMA runoff totaled $2.8B (composed of $4.2B less nominal Tsy holdings and $1.4B more TIPS), with emergency lending/liquidity facilities $0.7B lower.

- Over the last 4 weeks, the $20B/monthly expected QT pace was roughly adhered to: MBS fell $18B, with Treasury net holdings down around $2B (a fall in TIPS holdings offsetting a slight rise in nominals).

- Discount window usage accounted for the fall in lending facility usage this week; takeup is now down to $4.9B, down $1.3B in the last month and down from the 1-year high of $6.4B set in July which looks to have been a temporary blip higher.