US DATA: UMichigan: Consumers Increasingly Concerned About Jobs, Gov't Policy

Among the dozens of indicators underlying the flat sentiment reading in October's preliminary UMIchigan consumer survey (slightly better current conditions/slightly weaker expectations), a few areas of interest that generally show weak conditions in the labor market and purchasing sentiment:

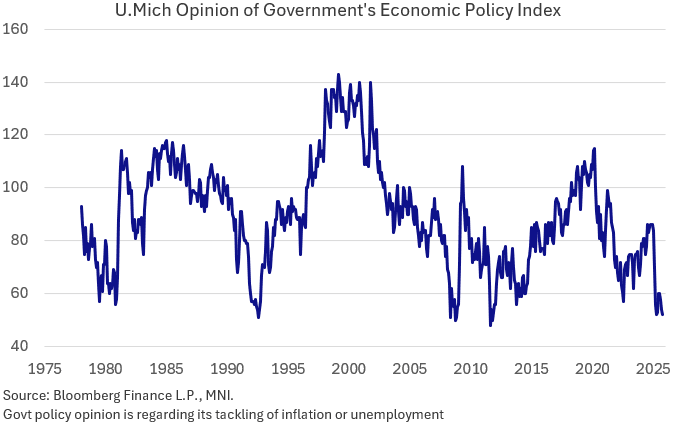

- A 3rd consecutive drop in the net opinion of the government's economic policy, to 52 from 54, marking the lowest since April which had been the lowest since 2011. This came amid the federal government shutdown (though the report notes "interviews reveal little evidence that the ongoing federal government shutdown has moved consumers’ views of the economy thus far") as well as continued concerns over inflation and, increasingly, jobs.

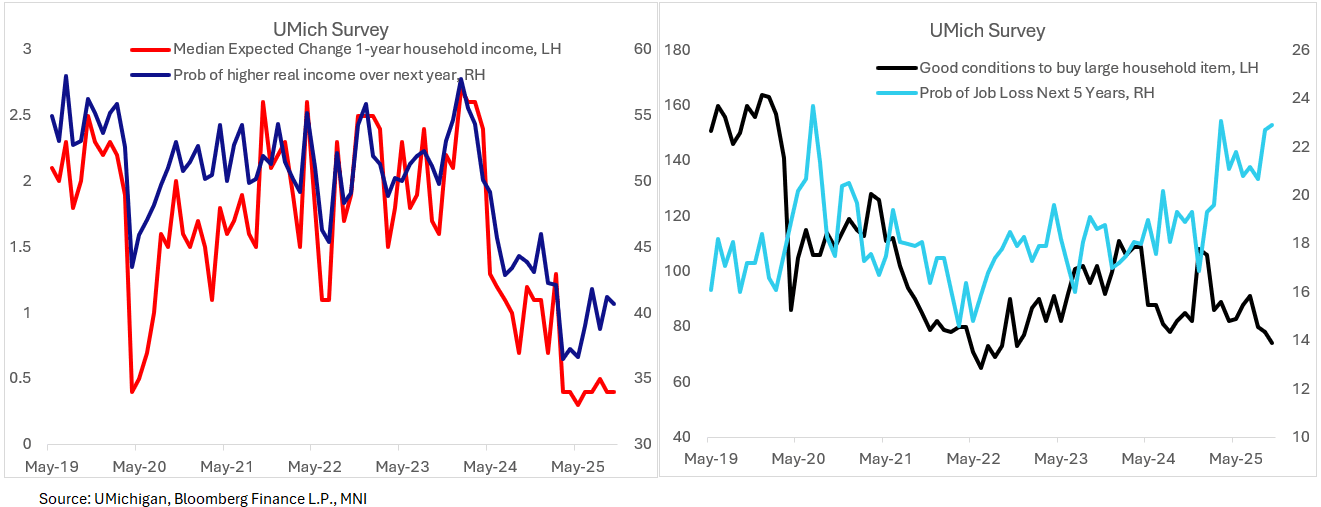

- Perceived probability of job loss in the next 5 years ticked up to 22.9% from 22.7%, for the highest since March, then before that in July 2020 and March 2009.

- A continued deterioration in the index for "good time" to buy large household durables fell to to 74, lowest since November 2022, from 78 prior. Buying conditions for vehicles and homes remained subdued.

- Median expected change in 1-year household income remained in the 0.4-0.5% area for a 5th consecutive month, levels consistent with the bottom of the pandemic in 2020. The implied probability of higher real income over the next year fell to 40.7 from 41.2, actually better than the Q2 lows - presumably as inflation expectations were pared from the highs.

- All that being said, there was a wealth effect offset to weak job and income expectations: the probability of adequate retirement income remained elevated (46%) with 56% expecting stock markets to rise in the next year, and the current value of stock market investments at all time highs. While year-ahead expectations for home values was flat (1.9%), 5Y expectations oddly equaled the series high at 5.3%.

- For all that, there wasn't much difference in sentiment shifts among the three income brackets though the highest-income were the most positive (bottom third 50.5, middle third 53.3, top third 61.9).

- The usual partisan splits prevailed, with consumer sentiment near all-time lows at 36.3 for Democrats and 53.9 for independents, but ticking up to near post-2020 highs for Republicans at 98.2.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US EIA: CRUDE OIL STOCKS EX SPR +3.94M TO 424.6M SEP 05 WK

- US EIA: CRUDE OIL STOCKS EX SPR +3.94M TO 424.6M SEP 05 WK

- US EIA: DISTILLATE STOCKS +4.72M TO 120.6M IN SEP 05 WK

- US EIA: GASOLINE STOCKS +1.46M TO 220.0M IN SEP 05 WK

- US EIA: CUSHING STOCKS -0.36M TO 23.9M BARRELS IN SEP 05 WK

- US EIA: SPR +0.51M TO 405.2M BARRELS IN SEP 05 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE +0.6% TO 94.9% IN SEP 05 WK

SCANDIS: Fresh Strength For NOK and SEK Since the US Equity Open

Fresh strength seen for Scandi FX since the US cash open, seemingly a function of the broader dollar pullback post-US PPI rather than in response to any fresh domestic catalyst. NOK and SEK outperform the G10 basket on an intraday basis.

- USDNOK (-0.9%) is narrowing the gap to the June 17 low at 9.8615, clearance of which would expose the December 2022 low at 9.6982.

- A reminder that this morning’s August inflation report was stronger-than-expected, driving a 7bp intraday rise in 2-year NOK swap rates and placing heightened focus on tomorrow’s Q3 Regional Network Survey. A Norges Bank hold next week is still possible if that survey is hawkish.

- USDSEK meanwhile has registered a fresh multi-year low, with support seen at 9.2307 (March 2022 low).

- Tomorrow’s Swedish calendar includes the final August inflation report, details of which will be important to judge the likelihood of a September rate cut. With Riksbank Deputy Governor Jansson not coming across as overtly dovish following the lower-than-expected flash release last week, the Executive Board could decide to keep rates steady in September, and save some dry powder for later this year if required.

- Riksbank Governor Thedéen also speaks tomorrow at 1200BST. The topic of the speech is banking sector liquidity.

GLOBAL: MNI Tech Trend Monitor - Highlighting Key Longer-Term Trends

MNI Tech Trend Monitor: https://emedia.marketnews.com/marketnewsintl/MNITechTrendMonitor.pdf

We introduce the MNI Tech Trend Monitor - This document highlights a selection of key longer-term trends that we have identified in markets that could be reaching inflection points, trend reversals/extensions or technically significant levels.

Covering:

- UK Gilt 10y Yield

- UK Gilt 30y Yield

- ICE USD Index

- Europe Banking Stock Index (SX7E)