OIL: Ukraine Attacks on Tankers Won't Hurt Oil Supplies: Putin

"*PUTIN: UKRAINE'S ATTACKS ON TANKERS WON'T HURT OIL SUPPLIES" - BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK FISCAL: PM Refuses To Rule Out Income Tax Threshold Freeze

Facing Prime Minister's Questions in the House of Commons, PM Sir Keir Starmer refuses to rule out a freeze in income tax thresholds at next week's budget. Asked by Leader of the Opposition Kemi Badenoch first why the government briefed that it was looking at raising income tax in the Budget, before Chancellor of the Exchequer Rachel Reeves then decided against it, Starmer claims it "will be a Labour Budget with Labour values, that means we will focus on cutting NHS waiting lists, cutting debt and cutting the cost of living,”.

- Badenoch asks four times about income tax thresholds, at one point asking, “The Prime Minister needs to come clean, can he confirm that he won’t break another promise by freezing income tax thresholds?”

- Starmer does not answer directly, instead claiming “The budget is one week today, and we will lay out our plans. But what we won’t do,[...] is inflict austerity on the country as they did. What we won’t do is inflict a borrowing spree like Liz Truss inflicted and done huge damage...”

- The lack of a concrete answer from Starmer will be viewed as an effective admission that thresholds will be frozen.

US TSY FUTURES: December'25-March'26 Roll Update: Early 5Y Lead

The latest Tsy quarterly futures roll volumes for December'25 to March'26 outlined below. Percentage complete still in the single digits ahead the "First Notice" date of Friday, November 28. Current roll details:

- TUZ5/TUH6 appr 13,400 from -5.88 to -5.62, -5.88 last; 5% complete

- FVZ5/FVH6 appr 172,500 from -2.75 to -2.25, -2.75 last; 11% complete

- TYZ5/TYH6 appr 29,200 from 1.5 to 2.0, 1.75 last; 12% complete

- UXYZ5/UXYH6 5,000 from 5.25 to 5.5, 5.25 last; 5% complete

- USZ5/USH6 3,600 from 13.0 to 13.75, 13.25 last; 8% complete

- WNZ5/WNH6 appr 3,300 from 9.75 to 10.25, 10.0 last; 6% complete

- Reminder, Dec'25 futures don't expire until next month: 10s, 30s and Ultras on December 19, 2s and 5s on December 31. Meanwhile, Dec'25 Tsy options will expire this Friday, November 21

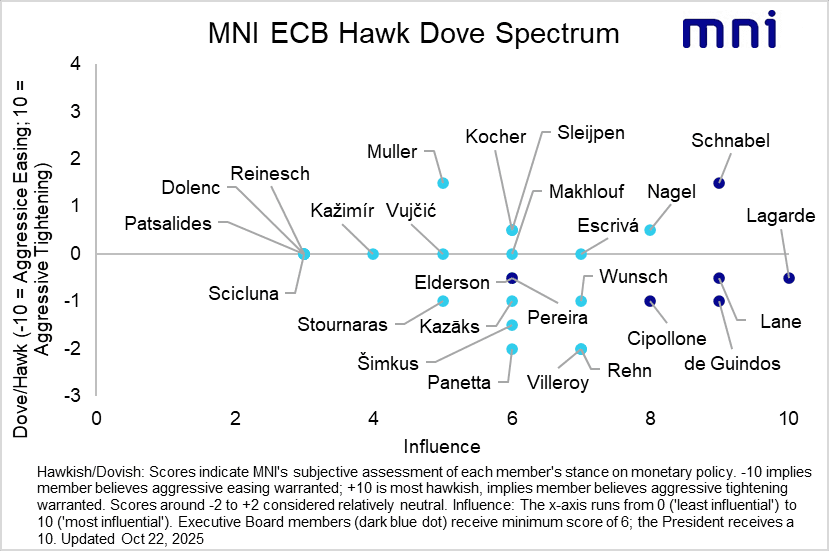

ECB: ECB Speak Wrap (Oct 31 – Nov 19) - A Few Tweaks To Hawk/Dove Matrix

The implied probability of another ECB cut this cycle has pulled back since the ECB’s October decision. OIS markets now price just 9bps of easing through September 2026 (vs ~12bps before the October decision). A combination of resilient growth signals and fairly cautious ECBspeak have factored into recent repricing, even with some Governing Council members still cognizant of downside inflation risks in the medium term.

The introduction of the EU’s ETS2 carbon pricing scheme is likely to be delayed by a year to 2028. This is expected to mechanically pull down the ECB’s 2027 inflation projection by ~0.3pp, deepening the expected undershoot of the 2% target, but policymakers have warned against relying too much on these dynamics for calibrating near-term policy.

Taking into account commentary since the October decision, we’ve made a few tweaks to our ECB hawk/dove matrix. See the full report for more