EMISSIONS: UKAs Trade Rangebound at Multi-Year High

UKAs Dec26 are holding at the highest since April 2023 with optimism over the UK-EU ETS linkage.

- UKA DEC26 up 0.1% at 67.97 GBP/MT

- EUA DEC 26 down 0.3% at 88.25 EUR/MT

- NBP Gas JAN 26 up 0.8% at 73.74 GBp/therm

- TTF Gas JAN 26 up 0.7% at 27.92 EUR/MWh

- ICE UKA futures daily aggregate traded volume stood at 2,029 contracts in the previous session, down 66.22% compared with the 30-day average.

- The EUA Dec26 premium to the UK equivalent has narrowed further to €10.37/ton CO2e at the time of writing. The spread has narrowed sharply since mid-December.

- Correlation between UKA/EUA for 30-day period at 0.33.

- Correlation between UKA/TTF for 30-day period at 0.2.

- Correlation between UKA/FTSE for 30-day period at 0.4.

- The latest two-week weather forecast for London sugges5ts mixed temperatures through the forecast period. Mean temperatures are set to rise early next week briefly, before easing back again. Temperatures are set to be milder in the first week of January.

- Wind output in the UK is forecast to remain strong through most of the forecast period, with lower output late this week/early next week, before rising back up. Output is forecast between 4.34GW and 16.75GW during base load on 25 December – 2 January, according to SpotRenewables.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

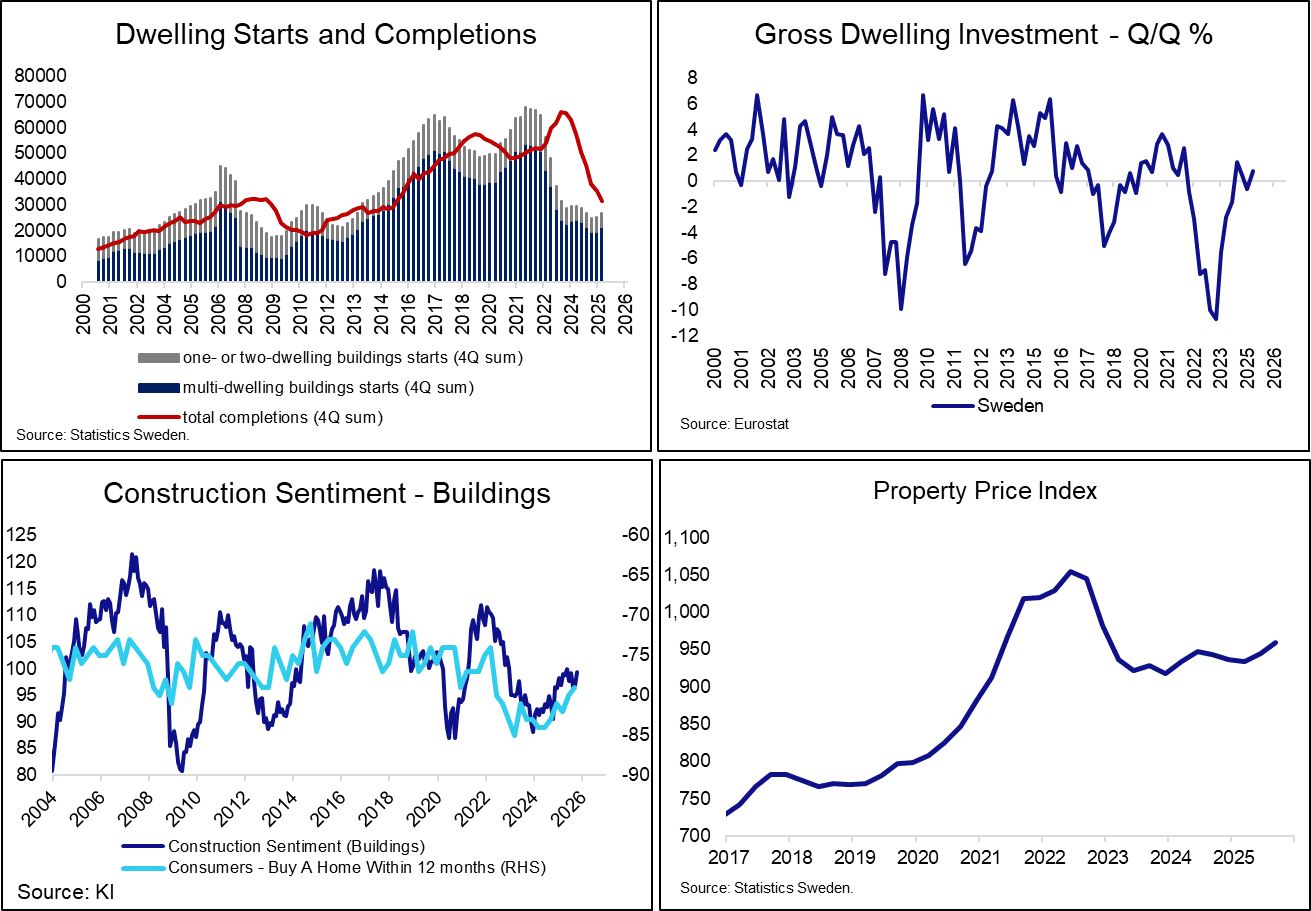

SWEDEN: Recovery in Residential Construction Sector Remains Sluggish

The recovery in the Swedish residential construction sector remains sluggish. Although this year’s rate cuts have provided financial relief, concerns around short- and long-term demand have constrained starts, and prevented completions from bottoming out. Property prices have started trending higher from 2023 lows, but remain well below 2021/2022 levels.

- Total housing starts increased by 6.5k in Q3, down from 7.5k in Q2. Measured as a 4Q rolling sum, total housing starts rose 26.9k in Q3, up from 25.4k in Q2 for the highest in a year.

- The number of completions remains firmly on a downward trend though, increasing 31.5k in Q3 after 35.3k in Q2 and 50.6k a year ago.

- While dwelling investment in the national accounts has rebounded from the Covid-induced slump, recent quarters have seen more stable (but no longer increasing) readings. Q3 GDP is due on Thursday.

- Although sentiment indicators in the Economic Tendency Indicator have stabilised in recent months (see charts), they remain below pre-covid averages.

- Furthermore, the Riksbank’s latest Business Survey noted that:

- “In residential and commercial construction, projects are sometimes being postponed because of uncertainty about how demand will develop. The weak demand for new housing means that construction companies can basically only sell projects that have largely been completed”

- ”Construction companies hope that the lower level of interest rates and the upcoming fiscal policy stimulation measures will kick-start the wider economy. At the same time, they see households as “so hesitant” and are unsure whether the measures will be enough to boost demand for new homes”.

- “In a longer perspective, the major construction companies emphasise that there is already a high supply of housing in the major cities, while population projections do not indicate that demand for new housing will increase in the years ahead.”

UK FISCAL: Rail fares may reduce headline CPI by 0.02ppt / services 0.04-0.05pp

We estimate that the weekend announcement by the government that regulated rail fares will be frozen in March 2026 may knock around 0.02ppt off of headline CPI and around 0.04-0.05ppt off services CPI versus prior expectations.

- If there had been no intervention rail fares would have risen by July 2025 RPI+1% in March 2026. This would have been 5.8%Y/Y. Expectations were probably that this would have been adjusted down to an RPI flat release, which would have still see a 4.8%Y/Y increase this year. However, this would have been similar to March 2025's RPI+1% increase of 4.6%Y/Y.

- Rail fares have a weighting of 0.72507% within headline CPI (1.4477% within services CPI).

- Only 40% of rail fares are regulated (ONS 2022) with unregulated fares including first class and advance tickets.

- Taking a quick back of an envelope calculation and comparing to an RPI flat increase, regulated fares being frozen would reduce headline CPI by 0.014ppt (services CPI 0.028ppt).

- However, its likely that given the regulated fares freeze the government will be strongly encouraging other rail fare increases to be limited elsewhere. And as existing privatised franchises end, there will be even more control here.

- We therefore think that its probably a more reasonable assumption to see a 0.02ppt impact on March 2026 headline CPI and a 0.04-0.05ppt impact on March 2026 services CPI in response to this policy.

- For more on the ONS' methodology on rail fares in CPI see here and here.

BONDS: US Treasuries and UK Roll pace (updated)

As expected circa 50% of the Roll are completed. Would expect for 80% to be done by the end of the Day given the shorter US Week.

- WNA: 55%.

- USA: 55%.

- UXY: 51%.

- TYA: 50%.

- FVA: 57%.

- TUA: 56%.

- Gilt: 38% (as of Friday).