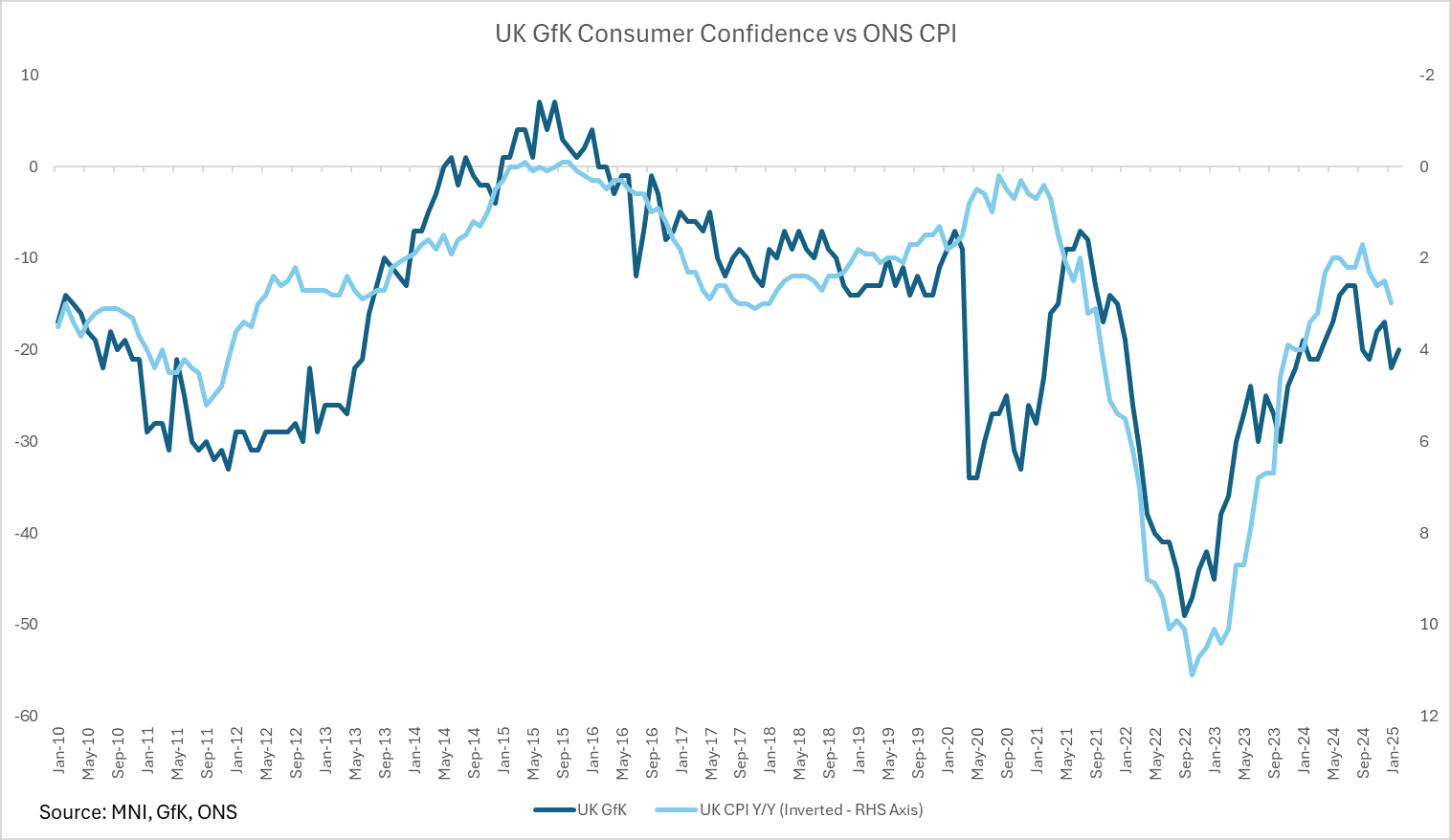

UK DATA: UK GfK Consumer Confidence Marginally Above Consensus

UK GfK Consumer Confidence in February rose 2 points above consensus to -20 (vs -22 consensus and prior).

- All 5 subcomponents increased (after all 5 declined in January). In particular, 'Personal Financial Situation over the next 12 months' rose 4 points to 2 - the highest reading since August 2024. The press release notes the BOE Bank Rate cut on Feb 6 is likely to have driven an improvement in sentiment.

- Whilst the GfK index is above consensus, it remains negative and significantly below where the index was between 2014 and mid-2019.

- Recall that the S&P Consumer Sentiment Index also rose in February to 45.4 but it was from a twelve-month low of 43.6 in Jan and remains firmly in contractionary territory. The S&P highlighted persistent job insecurity as limiting the boost to sentiment from lower interest rates.

- ONS CPI data on Wednesday showed headline CPI accelerating to 3.0% Y/Y, and is expected to remain at similar levels in the months ahead with the National Insurance Employee Contribution and National Minimum Wage rising in April. This is likely to keep sentiment dampened going ahead, not only due to cost pressures but due to increased job insecurity as costs rise for businesses.

- The Chancellors Spring Statement in March will also be closely watched for fiscal policy changes that affect businesses and consumers.

- The survey was conducted among a sample of 2011 individuals between January 31 and February 13.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (H5) Trend Needle Points South

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 142.73/144.48 - High Dec 9 / High Nov 11

- PRICE: 141.15 @ 15:56 GMT Jan 21

- SUP 1: 140.00 - Round number support

- SUP 2: 139.38 - 2.764 proj of the Aug 6 - Sep 3 - 9 price swing

- SUP 3: 138.87- 3.000 proj of the Aug 6 - Sep 3 - 9 price swing

A clear downtrend in JGB futures remains intact and the latest fresh cycle lows reinforce this condition. Note too that moving average studies on the continuation chart are in a bear-mode setup, highlighting a clear downtrend. The move down exposes the 140.00 psychological handle next. For bulls, a reversal would open 142.73 and 144.48, the Dec 9 and Nov 11 high respectively. For now, short-term gains are considered corrective.

JGBS: Futures Uptick Overnight With US Tsys, Light Local Calendar

In post-Tokyo trade, JGB futures have upticked, +2 compared to settlement levels, after the US Treasury curve bull-flattened following Monday’s holiday, as market focus remained on Trump administration policies post-inauguration. US yields ended 1-5bps lower.

- Offshore data was limited: the January Philly Fed non-manufacturing survey was soft, and Canadian CPI came in below expectations.

- With 2025 Fed rate cut expectations fairly static (and the FOMC is in its pre-January meeting blackout period), the US tsys short end remained anchored.

- Wednesday's US data calendar remains light, with MBA mortgage data and the December Leading Index - more focus will be on $13B 20Y Bond reopening auction, as well as a Fox interview with Pres Trump airing after Wednesday's cash close.

- Today, the local calendar will see BoJ Rinban Operations covering 1-25-year JGBs.

- BoJ Policy Decision is on Friday, with a 25bp hike expected. A hike will put the BoJ's key rate at 0.5%, its highest level since 2008.

NEW ZEALAND: RBNZ’s Core Measure Likely To Moderate From Q3’s 3.4%

Q4 headline inflation was significantly impacted by some volatile components thus making underlying measures important to gauge the trend. The RBNZ releases its sector factor model estimates today at 1500 NZDT (1300 AEDT) and core is likely to moderate further towards the target band from its Q3 reading of 3.4% y/y. Non-tradeables inflation has a 77% correlation with the RBNZ’s core measure and the two have moved very closely since 2021. The former remained elevated but moderated 0.4pp to 4.5% y/y in Q4, lowest since Q3 2021, signalling a further easing in underlying inflation when the RBNZ data is released.

NZ CPI y/y%