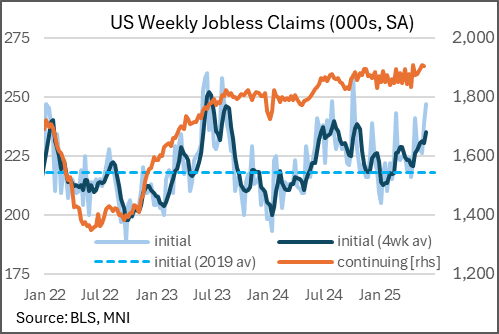

US DATA: Typical Seasonality Pushes Initial Claims To 34-Week High

Jun-05 12:58

Initial jobless claims unexpectedly rose in the week of May 31, rising to 247k (235k expected) from 239k (rev from 240k) prior. That's two consecutive weeks of rises to the highest weekly total in 34 weeks, bringing the 4-week average up to 235k (31-week high).

- Continuing claims meanwhile went in the opposite direction, ticking lower in the May 24 week to 1,904k (1,910k, after a decent 12k downward revision to 1,907k prior) for the first downward move in 4 weeks.

- More focus will naturally be on the rise in initial claims therefore.

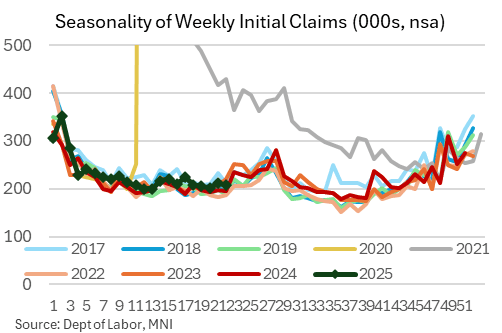

- From a seasonality perspective, there was nothing out of the ordinary for early summer, with the typical seasonal adjustments pushing the SA figure higher: NSA claims if anything were tame, ticking 3k lower to 209k (by comparison, 196k the equivalent week of the prior year translated into 229k SA). NSA claims are set to continue rising over coming weeks as is usually the case for summer.

- State-by-state, Ohio (+6.7k), Minnesota (+6.6k) and Kentucky (+5.9k) each saw the biggest W/W % rises on an NSA basis, but not atypical for this time of year.

- There was also no major rise in DC-region (quite the opposite, ticking lower), with DOGE cuts still failing to make a major mark.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US REDBOOK: APR STORE SALES +6.7% V YR AGO MO

May-06 12:55

- MNI: US REDBOOK: APR STORE SALES +6.7% V YR AGO MO

- US REDBOOK: STORE SALES +6.9% WK ENDED MAY 03 V YR AGO WK

EQUITIES: Estoxx put spread

May-06 12:53

SX5E (17th Apr) 3500/3400ps, bought for 5 in 5k.

STIR: TD Securities Recommend Paying EUR 1y1y vs. GBP 1y1y/USD 1y1y.

May-06 12:50

TD Securities see “more room for USD front-end outperformance on a cross-market basis”.

- They believe that the expected “inflation bump in both the U.S. (H2) and UK (Q3) will be temporary supply- rather than demand-driven.”

- TD also highlight that “even though the UK's growth dynamics are closer to the Euro area, it still has a stronger beta to U.S. markets”

- Meanwhile, they expect “the ECB to ease to 1.5% or lower only if global conditions worsen. In that scenario again, it’s more like that the U.S. (or GBP) front-end still outperforms vs. EUR”.

- As a result, they recommended paying EUR 1y1y vs. GBP 1y1y/USD 1y1y.