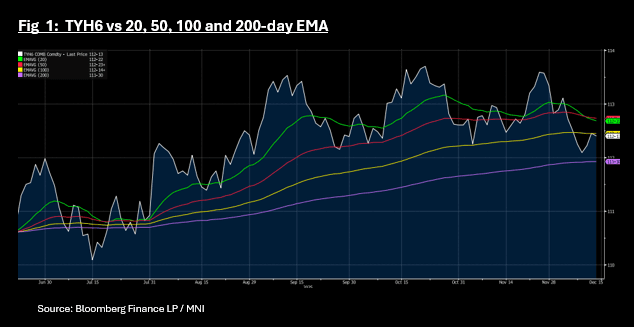

US TSYS: TYH6 Fails Key Resistance, Bond Yields Grind Lower on Slow Day

US bond futures are modestly lower Friday as volumes dip ahead after a busy week. The 10-Yr is down -02+ to 112-12+. Earlier TYH6 approached the 100-day EMA of 112-14+ but failed to break above and has consolidated below. Downside resistance is the 200-day EMA of 111-30.

Cash yields are better with movements lower of up to 1.4bps in shorter dated bonds.

- The 2-Yr is 3.531% down -1.2bps

- The 5-Yr is 3.722% down -1.4bps

- The 10-Yr is 4.153% down -0.6bps

- The 30-Yr is 4.798% down -0.4bps

Projected rate cut pricing has gained slightly vs. early US morning levels (*): Jan'26 at -6.1bp (-5bp), Mar'26 at -13.8bp (-12.7bp), Apr'26 at -19.1bp (-19.1bp), Jun'26 at -32bp (-32bp).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

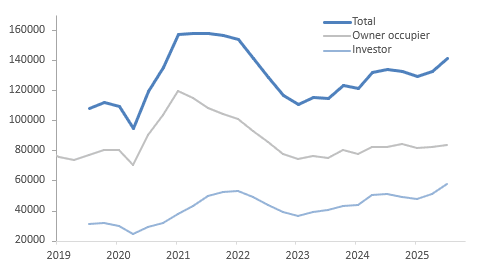

AUSTRALIA DATA: Strong Home Lending May Contribute To Extended RBA Hold

There was a strong rise in the number of new dwelling loans and their value in Q3 as house price inflation rose. The recovery in home lending began in Q2 after the RBA began easing in February and the 75bp to August appears to have contributed to the sharp rise. The Board is unsure how restrictive policy is and remains cautious. It noted this month that “the housing market is continuing to strengthen, a sign that recent interest rate reductions are having an effect”. The lending data is consistent with this and likely to add to its caution about easing further.

- The total number of home loans rose 6.4% q/q to be up 5.8% y/y driven by both owner occupiers and investors, but particularly the latter. Values increased 9.6% q/q to be 13.2% y/y higher as higher home prices added to the amount.

- Owner-occupier loans rose 2.0% q/q after 0.9% q/q to be +1.7% y/y with the growth split between first-time buyers (+2.3% q/q & 0.9% y/y) and others (+2.8% q/q & 3.3% y/y). The level is below that recorded in Q4 2024.

- The softness in owner-occupier lending compared to investors likely reflects poor affordability in the Australian housing market. Our affordability index has improved since Q2 2024 helped by higher incomes and lower rates but remains around 36% below trend and close to its series low.

- Loans to first-time homebuyers are likely to rise further in Q4 with the introduction of the government’s 5% deposit scheme.

- Investor loans soared 13.6% q/q after 5.9% in Q2 to be up 12.3% y/y with strength across states and territories.

No. of new loan commitments dwellings ex refi

Source: MNI - Market News/ABS

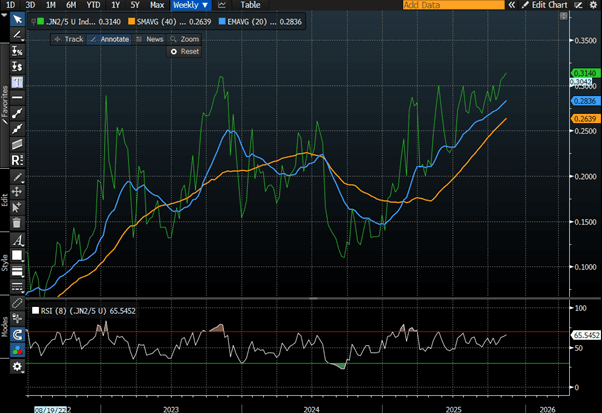

JGBS: 2/5 YC Near Cycle High Ahead Of Tomorrow's 5Y Supply

In Tokyo morning trade, JGB futures are slightly stronger, +6 compared to settlement levels.

- Cash US tsys are 3-4bps richer in today's Asia-Pac session after being closed yesterday for Veterans Day.

- Cash JGBs are little changed across benchmarks. The benchmark 5-year yield is 0.3bps lower at 1.249% versus the cycle high of 1.272%, set this month.

- “JGBs traders can’t relax even though a 30-year sale is out of the way, as this week’s 5-year auction could be more challenging. That duration falls in the sweet spot where increased bond issuance is likely to fall as Prime Minister Sanae Takaichi aims to use her first stimulus package to jump-start the economy.” – BBG

- Ahead of tomorrow’s supply, the 2/5 yield curve has pushed close to the cycle high of 32bps set in late 2023. (see chart)

- The 30-year yield is little changed today after yesterday's heavy close (+3.6bps cheaper) following another lacklustre auction.

- Swap rates are little changed.

Source: Bloomberg Finance LP

CHINA: Central Bank Injects CNY130bn via OMO

Money market rates are slowing starting to moderate as the PBOC has another day of significant liquidity injection. The overnight money market rate spiked yesterday to its highest level since July.

- The PBOC issued CNY195.5bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY65.5bn.

- Net liquidity injects CNY130bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.43%, from prior close of 1.51%.

- The China overnight interbank repo rate is at 1.40%, from the prior close of 1.40%.

- The China 7-day interbank repo rate is at 1.49%, from the prior close of 1.51%.