EM LATAM CREDIT: Tupy: Company Update – Neutral

(TUPY; NR/BB+neg/BB+)

• Brazil based global commercial vehicle manufacturer Tupy has struggled with lower sales volumes and margin pressure for a few quarters now and when the company reports Q3 earnings next week we expect more of the same. Weak EBITDA led to an increase in net debt leverage from 1.8x at the end of 2024 to 2.45x in Q2 and was expected to rise through year end 2025 before declining in 2026 on better operating results. Note that debt has not grown materially and operational cash usage has not been a problem.

• Bonds sold off starting in late September as part of an overall Brazil corporate bonds selloff from Braskem contagion. While several Brazil credits with stable credit profiles recovered to near unchanged, those with challenging profiles such as Tupy did not. TUPY 31s were last quoted at 9.09%, up 163bp since June 30th and up 130bp YTD. Note that Tupy 31s were quoted at 7.5% after the 2Q earnings report, which was the same yield as at June 30th and 30bp lower since Dec. 31st so the spike in yields this past month seems mostly due to the fallout from Braskem and not the challenging business conditions.

• Despite the challenges, we have a favorable view of Tupy over the medium term. Cash burn has been minimal with cash usage throughout the year mostly used for debt reduction. Liquidity is robust as Tupy has enough cash to pay off the next five years of debt maturities. We expect sales volume to reverse course next year as nearly 1 in every 3 trucks in Brazil is over 16 years old, 32% of the fleet is over 16 years old and the 11 to 20- year range has grown significantly according to the company. 47% of agricultural machines are over 20 years old and over 50% of the tractor fleet is over 20 years old, especially on small farms. Margins should improve as well with a lower cost structure from this year’s corporate restructuring.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURGBP TECHS: Sights Are On The Bull Trigger

- RES 4: 0.8835 High May 3 2023

- RES 3: 0.8800 Round number resistance

- RES 2: 0.8769 High Jul 28 and the bull trigger

- RES 1: 0.8751 High Sep 25

- PRICE: 0.8737 @ 16:13 BST Sep 29

- SUP 1: 0.8662/8597 50-day EMA / Low Aug 14 and the bear trigger

- SUP 2: 0.8562 50.0% retracement May 29 - Jul 28 upleg

- SUP 3: 0.8540 Low Jun 30

- SUP 4: 0.8514 61.8% retracement May 29 - Jul 28 upleg

EURGBP is trading closer to its recent highs and a bullish theme remains intact. The latest recovery paves the way for an extension towards the bull trigger at 0.8769, the Jul 28 high. Clearance of this level would strengthen the bull theme. Support to watch lies at 0.8597, the Aug 14 low. A breach of this level would instead reinstate a recent bearish threat. First support is 0.8662, the 50-day EMA.

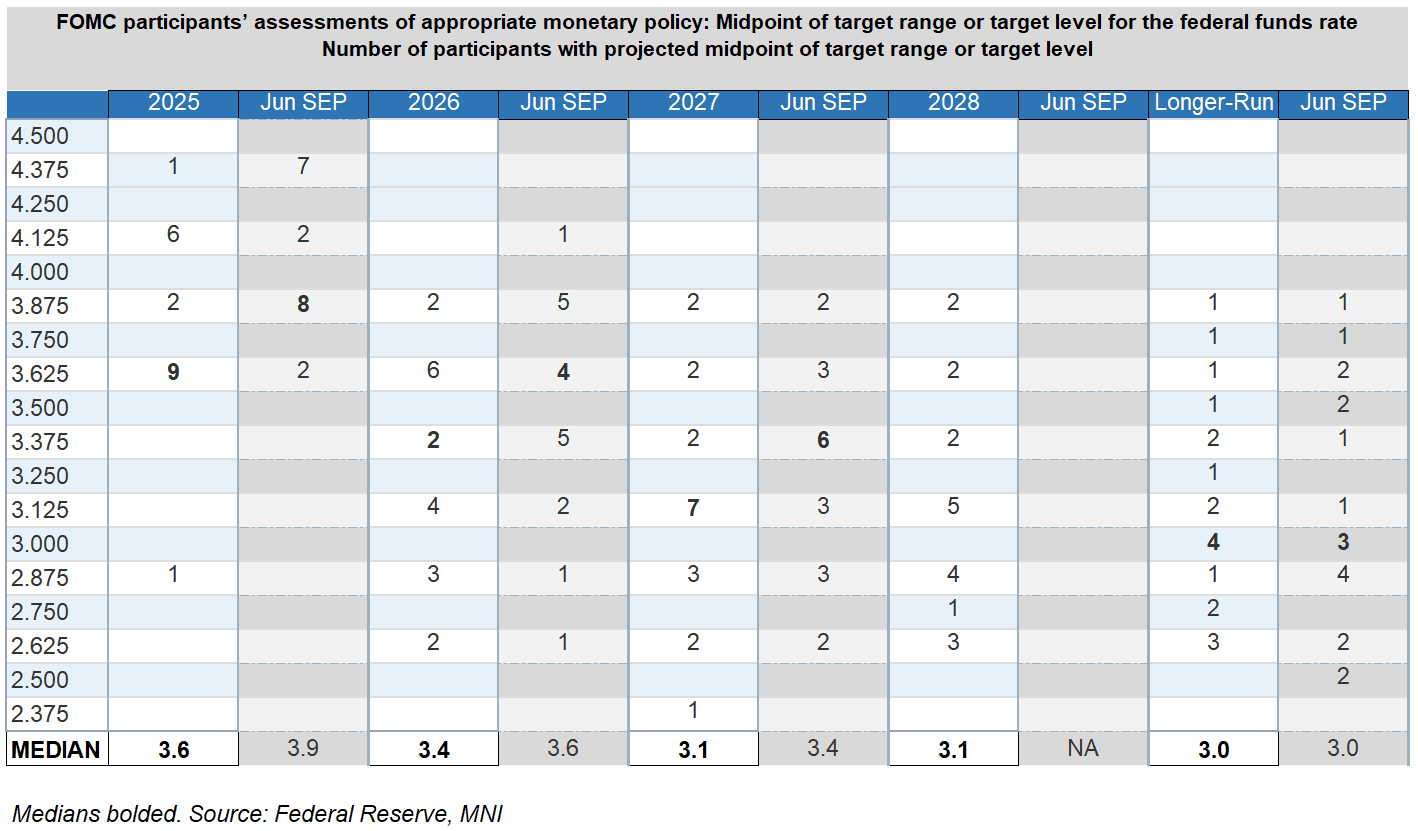

FED: NY's Williams: Don't Want To See Job Weakness Go Too Far

NY Fed Pres Williams signals in a Q&A Monday that he would be supportive of further rate cuts, saying "from my perspective, monetary policy has been and continues to be what we call restrictive." We think he's one of the 9 (of 19) FOMC members who is penciling in a total of 3 cuts by end-2025, including the one delivered last month.

- Historically he's been a dove, though prior to the September meeting he had sounded slightly wary of easing given risks that inflation could pick back up on tariffs.

- However today he says that there "doesn't seem to be any signs of inflationary pressures building", with the tariff impact being more limited than expected, and "underlying inflation continues to move down".

- He highlights labor market risks building: "We've seen a labor market that's been been remarkably resilient, gradually softening over the past year. We've seen the unemployment rate tick up. We've seen some other measures move kind of to signs that the labor market is softening. I don't want to see that go too far.... labor market indicators [are] softening somewhat. At the same time, the some of the upside risks to inflation, in my view, have come down."

- On the September rate cut and the path ahead: "It made sense to move interest rates down a little bit, to get them to take a little bit of the restrictiveness out of there. I still see monetary policy as putting downward pressure on inflation, but just a touch less. And so when it comes to the next question of, well, what do we do next? Do we need to do more cuts or are we, you know, I think the most important thing is we need to be driven by the data."

- Williams says his current model estimate for the real neutral rate is 0.75% - if that's what he has input into the Dot Plot in September, it implies that he has increased his longer-run rate forecast since June. September has 2 dots at nominal 2.75%, whereas there were none in June. The lowest longer-run dots are now at 2.625%, versus a 2.50% low in the June SEP.

GBPUSD TECHS: Remains Below Resistance

- RES 4: 1.3789 High Jul 1 and key resistance

- RES 3: .3661/3726 High Sep 18 / 17

- RES 2: 1.3537 High Sep 23 1

- RES 1: 1.3485 50-day EMA

- PRICE: 1.3421 @ 16:12 BST Sep 29

- SUP 1: 1.3324 Low Sep 25

- SUP 2: 1.3282 Low Aug 6

- SUP 3: 1.3254 Low Aug 4

- SUP 4: 1.3144 38.2% retracement of the Jan 13 - Jul 1 bull cycle

GBPUSD traded lower last week, marking an extension of the current bear cycle that started Sep 17. The move down has resulted in a break of 1.3491, a trendline support drawn from the Aug 1 low. This undermines a recent bullish theme. Note too that 1.3333, the Sep 3 low and a key support, has been pierced, opening 1.3282 next, the Aug 6 low. Initial key resistance to watch is 1.3537, the Sep 23 high. A break of it would signal a reversal.