WHITE HOUSE: Trump's 13:00ET Announcement Related To Pharma-Press Sec

White House Press Secretary Karoline Leavitt has confirmed that President Donald Trump's announcement, scheduled for 13:00ET/18:00GMT is related to pharmaceuticals. In the past 24 hours, reports from Axios and Reuters suggest that Trump could announce a deal with pharma giants to lower prescription drug prices under the 'most favoured nation' (MFN) regulation. Bloomberg reported on 17 Dec that agreements with Swiss giants Novartis and Roche had been reached, with Reuters reporting AbbVie may be another of the estimated five new firms to sign up.

- Axios: "The so-called most-favored-nation regulation would also have enormous financial implications for manufacturers. The proposed regulation, titled the "Global Benchmark for Efficient Drug Pricing (GLOBE) Model," completed review on Wednesday, according to OMB's website. The listing notes the proposal is "economically significant." The aim of this model would be to tie prices paid by the US gov't under Medicaid for those over 65 to the lowest prices the drugmakers pay in a basket of other countries. Reuters: "Analysts have noted that Medicaid, which accounts for only around 10% of U.S. drug spending, already benefits from substantial price discounts, exceeding 80% in some cases."

- Efforts from the Trump administration to push down drug prices come amid persistent public concerns about 'affordability' and declining approval for the president's handling of healthcare (for more, see MNI POLITICAL RISK-Trump Speaks Again On 'Affordability' In NC).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Fed Should Have Q3 GDP And September PCE Estimates By Its Dec Meeting

What's notable about the majority of post-shutdown rescheduled economic releases so far is that they are essential to compiling advance Q3 GDP and September PCE, both of which were originally due to be published by the Bureau of Economic Analysis at the end of October.

- That leaves it narrowly possible that we get an advance Q3 GDP release by the end of the month (ie Nov 28) depending on whether the BEA has time to compile and is willing to base their estimate on partial data to a greater degree than is usual, and whether the Thanksgiving holiday on Nov 27 forces a delay into the following week. Certainly we are now confident that the FOMC will have a Q3 GDP estimate and September PCE data in hand by the time of its Dec 9-10 meeting.

- September international price indices used in the GDP calculation are now due out by BLS on Dec 3, and September advance goods trade and business inventories data haven't yet been rescheduled (it was originally due out Oct 29, the day before advance GDP), but aside from these the BEA should have enough data to compile an initial Q3 estimate.

- With PPI and CPI data for September all out by Nov 25, BEA's got pretty much all it needs to produce a monthly PCE price estimate for that month, absent a narrow sliver that it gets from import prices. Just conjecture but it's possible that it could get the import prices it needs on an inter-agency basis ahead of Dec 3.

- As for the consumption and income portions of the September PCE report: the September payrolls data (Nov 20) will provide the underlying estimates for wages and salaries needed for the income estimates, while the retail sales data is the lion's share of the consumption data and much of the services consumption is either estimated anyway or derived from September nonfarm payrolls.

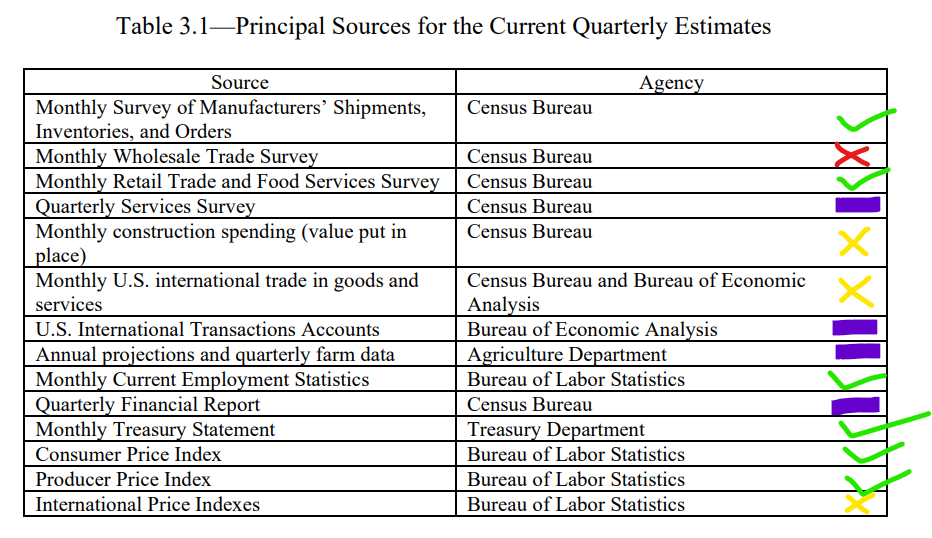

- For the quarterly GDP estimates, the image below shows the major reports used (from the BEA's methodology document) - the green checkmarks are those data that will be in hand by Wednesday Nov 26; the red X (wholesale trade) won't be available, the yellow X's will either likely be partly available or wouldn't have been available anyway by the original GDP release data; and the purple bars represent series that are used more for Gross Domestic Income and future revisions rather than the advance estimate.

- We've only had updates on this morning's trade data rescheduling from the BEA so far, but as we have been saying, they depend heavily on other agencies to compile the source data for their own series. As such we will hopefully hear from them soon as to the PCE and GDP reschedulings.

EQUITY TECHS: E-MINI S&P: (Z5) Bearish Outlook

- RES 4: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6953.75 High Oct 30 and bull trigger

- RES 2: 6900.50 High Nov 12

- RES 1: 6779.00 20-day EMA

- PRICE: 6640.50 @ 14:31 GMT Nov 19

- SUP 1: 6594.00 Low Nov 18

- SUP 2: 6571.25 Low Oct 17

- SUP 3: 6540.25 Low Oct 10 and a key support

- SUP 4: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

S&P E-Minis maintain a softer short-term tone. The breach of support at 6655.70, the Nov 7 low cancels recent bullish signals and signals scope for an extension of the current corrective cycle. Note that price has also breached support at the 50-day EMA. An extension would open 6540.25, the Oct 10 low and the next key support. Initial firm resistance to watch is 6779.00, the 20-day EMA.

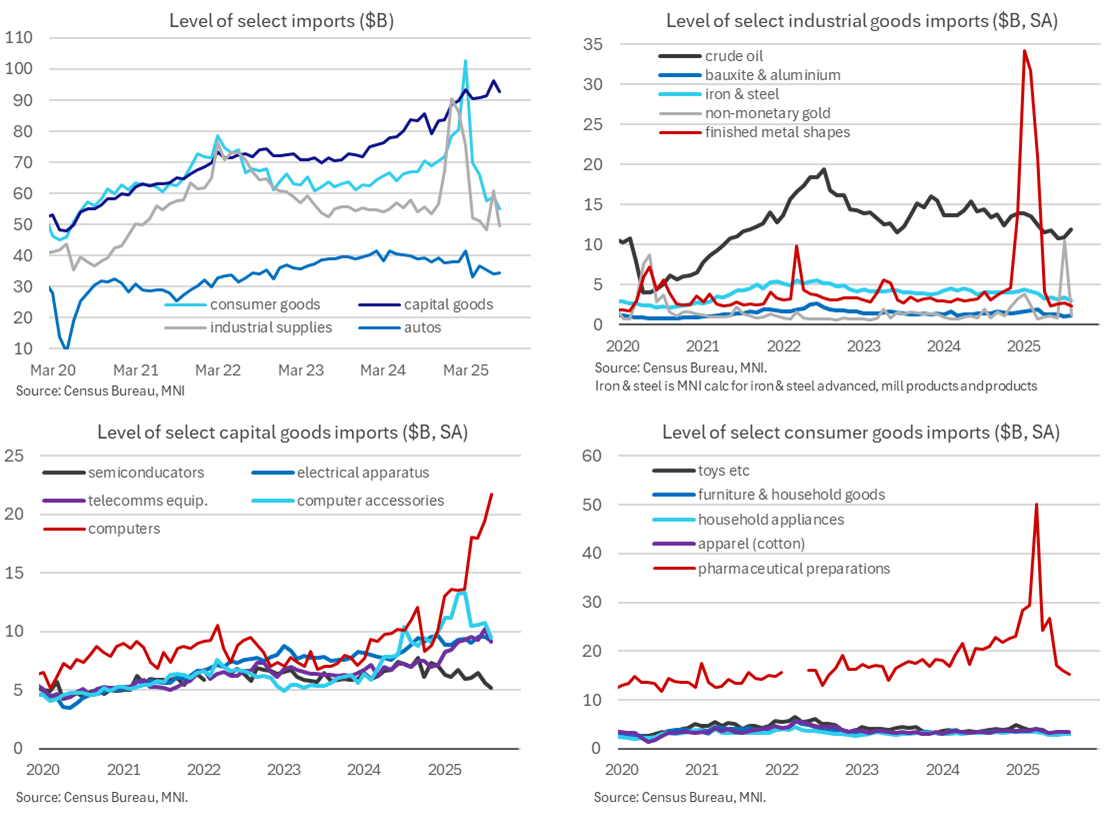

US DATA: Gold Imports Drove Summer Swing, Computer Surge Continued [2/2]

- Today’s details give us a better sense of the drivers behind what we had already known to have been broad-based weakness in imports, with consumer -7.0% M/M after 2.4%, capital -4.4% after 5.1% and industrial supplies -19.6% after 24.3%.

- The swing in industrial supplies was dominated by a pullback in non-monetary gold imports after a surprise jump in July (from $0.9bn in Jun to $10.5bn in Jul and now $1.2bn in Aug).

- This category had picked up earlier this year on tariff front-running with a high of $3.8bn in January but it was tiny compared to the surge in monetary gold which drove the “finished metal shapes” category to $34bn in Jan vs a more typical $3-4bn per month and a latest value of $2.4bn in August. Recall that monetary gold doesn’t feed into GDP calculations (but the non-monetary gold category noted above, does) and now sees the Atlanta Fed’s GDPNow run on an ex-gold basis, for example.

- Capital goods imports fully reversed July’s large increase, falling back from $90.6bn to $86.6bn, despite a further cranking higher in computer imports to $21.7bn (+2.3bn). That’s up from $10bn in December. Nearly all other categories fell on the month, with the largest coming from computer accessories (-1.3bn), telecommunications equipment (-1.1bn), medical equipment (-0.4bn) and semiconductors (-0.4bn).

- Consumer goods imports meanwhile continued their downtrend into August compared to some particularly elevated readings earlier this year on Irish pharmaceutical front-running. Latest Eurozone trade data for September suggests this reversed with a sharp increase. For now, the $55bn in August was the lowest nominal level of consumer goods since mid-2020. This category saw $72bn of imports in Dec 2024 before surging to a peak of $103bn in March ahead of telegraphed reciprocal tariff announcements in early April.